THE VANTAGE

Issue 131 | April 20, 2026

About those private credit headlines…

The headlines are loud right now. Here’s what’s actually going on, and what it means for how we’re positioned

In today’s email:

- The word “private credit” is doing a lot of work in the news right now — and most of it doesn’t apply to you

- Why a “gate” isn’t the same as a problem

- From panic to record highs in four weeks — what just happened

- A quiet note on where the calm comes from

Beyond the Portfolio

Nine days until April 30

Quick one.

The deadline to file your personal tax return is Thursday, April 30. That’s nine days away.

If you haven’t gathered your slips, sent them to your accountant, or booked the time to file — this is the reminder. The CRA has been especially active this year, particularly on anything involving real estate, rental income, and crypto. (We wrote about this in our first issue.)

If your situation has any complexity to it — a business, investment accounts, multiple income sources, a property sale — don’t leave it to the last weekend. File an extension if you need to. Just don’t ignore it.

If you’re not sure whether your accountant has everything they need from us, reply to this email and we’ll double-check.

The Scoop

What the headlines won’t tell you about private credit

If you’ve been paying attention to the financial news lately, you’ve probably seen the headlines. CNN ran a feature last week on how private credit is “worrying Wall Street.” Bloomberg has been running stories on default warnings piling up. Jamie Dimon wrote about it in his annual shareholder letter. BlackRock made news for limiting withdrawals from one of its private credit funds.

Clients have been reaching out. So let’s walk through it.

Here’s the thing about the phrase “private credit”: it’s doing a lot of work in the headlines right now and most of what it’s describing isn’t the private credit you actually own.

Let’s take it apart.

One. The publicly-traded credit funds (called BDCs) have been volatile. These funds trade on the stock exchange like any other stock, which means they get whipped around by market sentiment, not by what’s happening inside the loans themselves. When you read that a BDC is “down 12% this year,” that’s a pricing reaction to broader market mood — not a sign that the underlying loans are going bad. We don’t own BDCs. The private credit we hold is not traded on exchanges and is priced based on what the loans are actually worth.

Two. Some retail-focused private credit funds have hit redemption limits. When you hear that a fund is “gating” investors or “freezing” redemptions, it sounds alarming. But those limits are built into the structure of the fund from day one — you agree to them when you invest. They exist to protect everyone from forced fire-sales during moments of panic. It’s the fund working as designed, not a sign of distress. The media loves the word “gate.” It’s doing a lot of work in those headlines.

Three. There’s growing concern about loans to software companies, especially with AI reshaping the landscape. This one is legitimate to watch. Some of the large direct lenders have heavy exposure to sponsor-backed software companies, and if AI meaningfully disrupts those business models, some of those loans will come under pressure. Most of these loans are senior-secured at conservative loan-to-value ratios, which means a company’s value would need to drop significantly before lenders take a real loss. But it’s a story worth tracking.

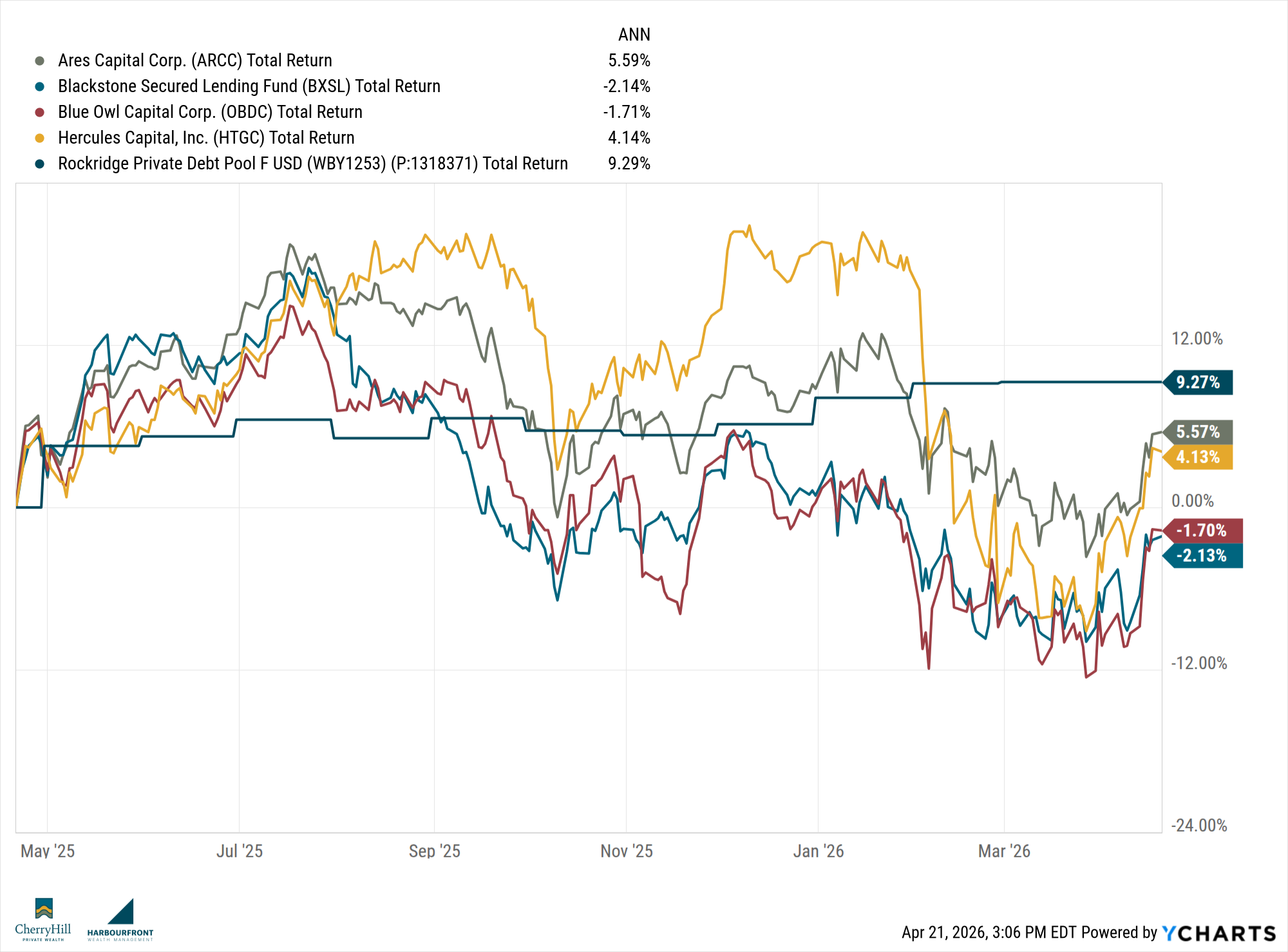

Below are some of the top BDC funds on the market. I have included our Private Credit (Debt) offering in here for comparison, which is the Rockridge Private Debt Pool.

Now — here’s the part that matters for you.

Our private credit exposure isn’t concentrated in any of the areas getting the most attention. We’re not heavily allocated to the large, sponsor-backed corporate lending that dominates the headlines. Our allocation is diversified across asset-backed lending, residential and commercial mortgages, and specialty finance. Different risk drivers. Different loan structures. Different borrowers. Different everything.

The managers we use have been lending through multiple credit cycles. They underwrite conservatively. They hold loans they’re comfortable holding. One of our largest holdings is a Canadian mortgage book that has been operating for over four decades.

Default rates across our managers remain low. Borrower earnings are holding up. And none of them have flagged systemic concerns.

Could the credit cycle turn? Yes. It always does, eventually. And when it does, we’ll probably see a few of the more aggressive lenders get hit. That’s normal. That’s how cycles work. What matters is that the portfolios we’ve built weren’t designed to win when everything is going up — they were designed to hold up when it isn’t.

The headlines are loud right now. The portfolio is built quiet.

Market Minute

Since We Last Spoke

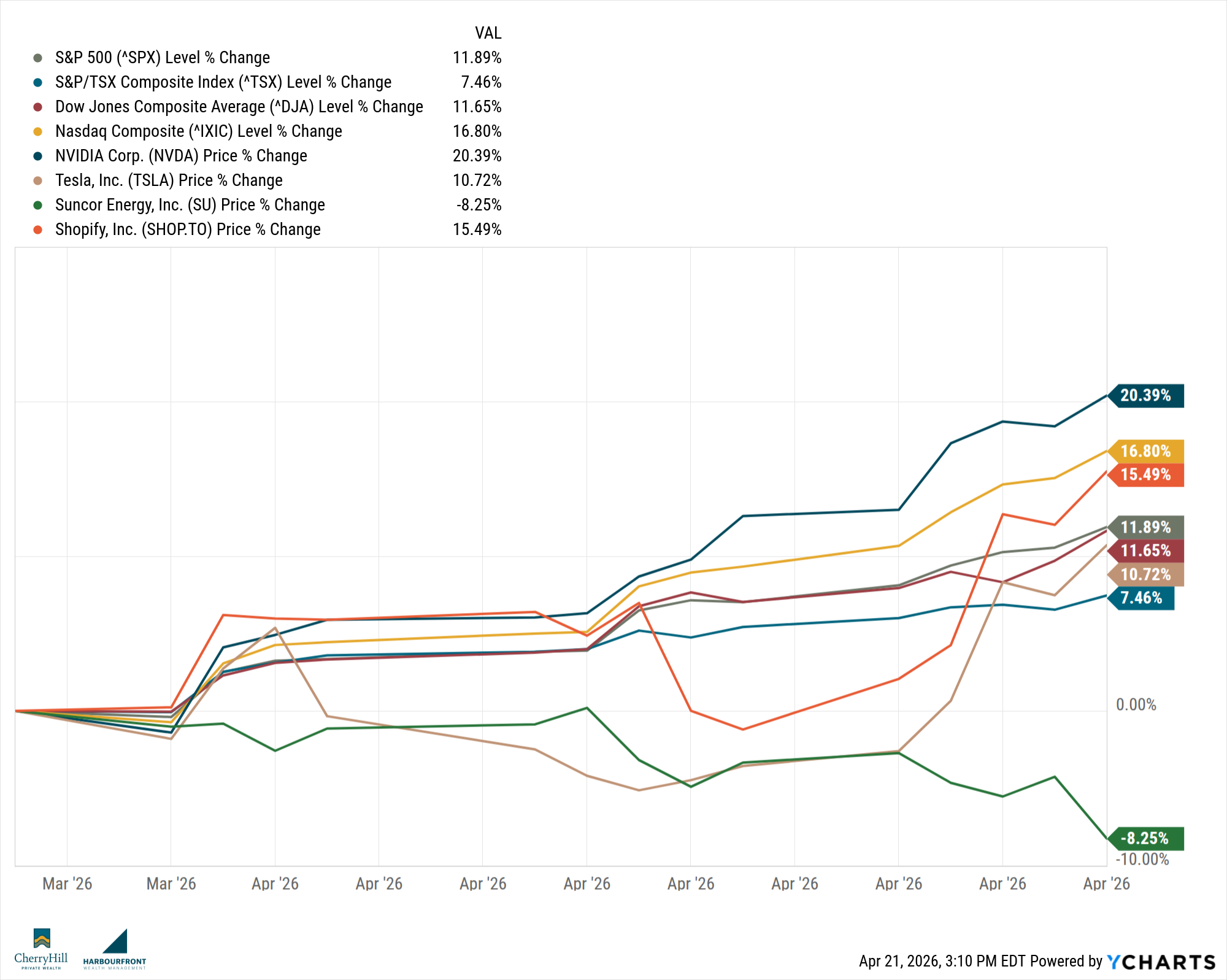

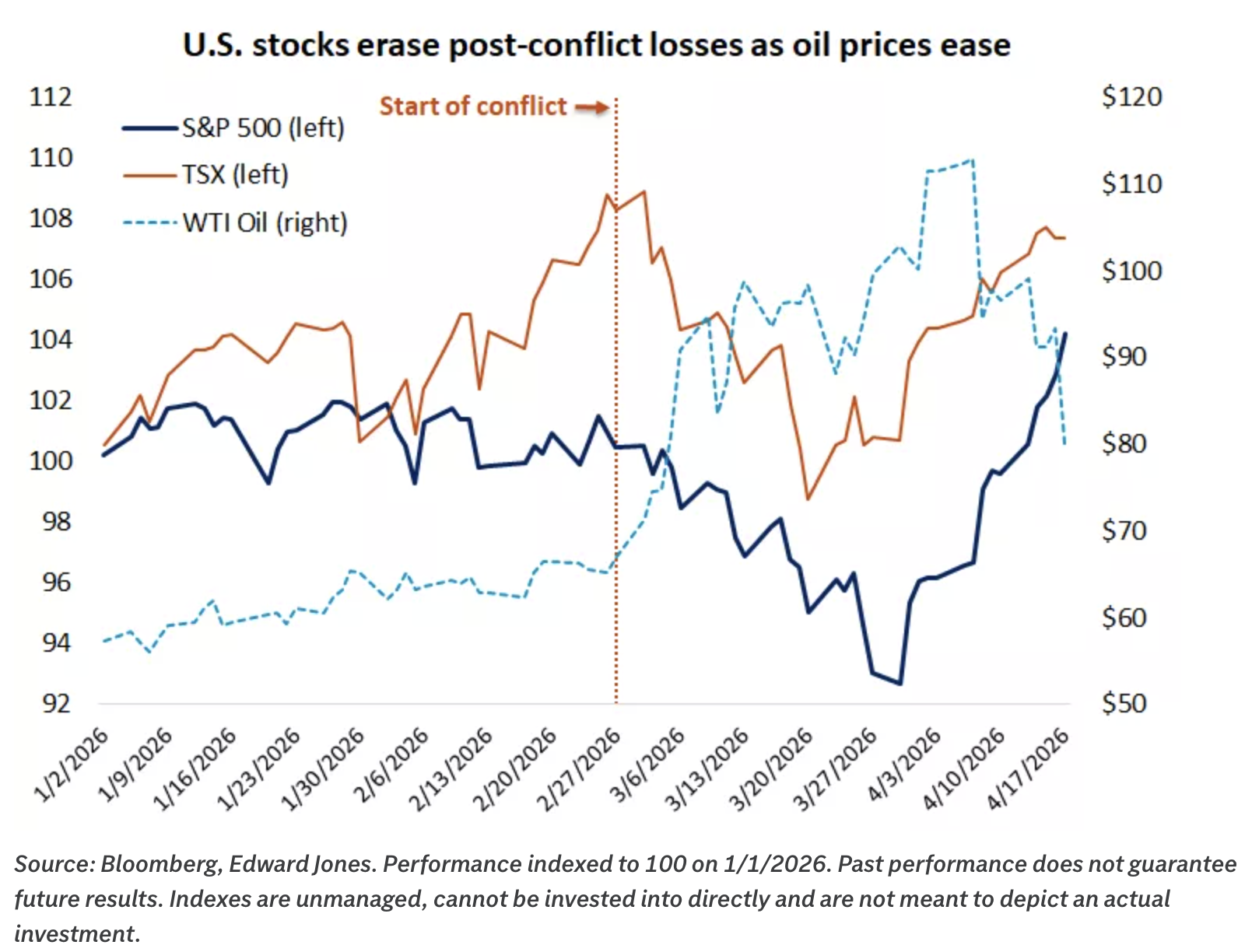

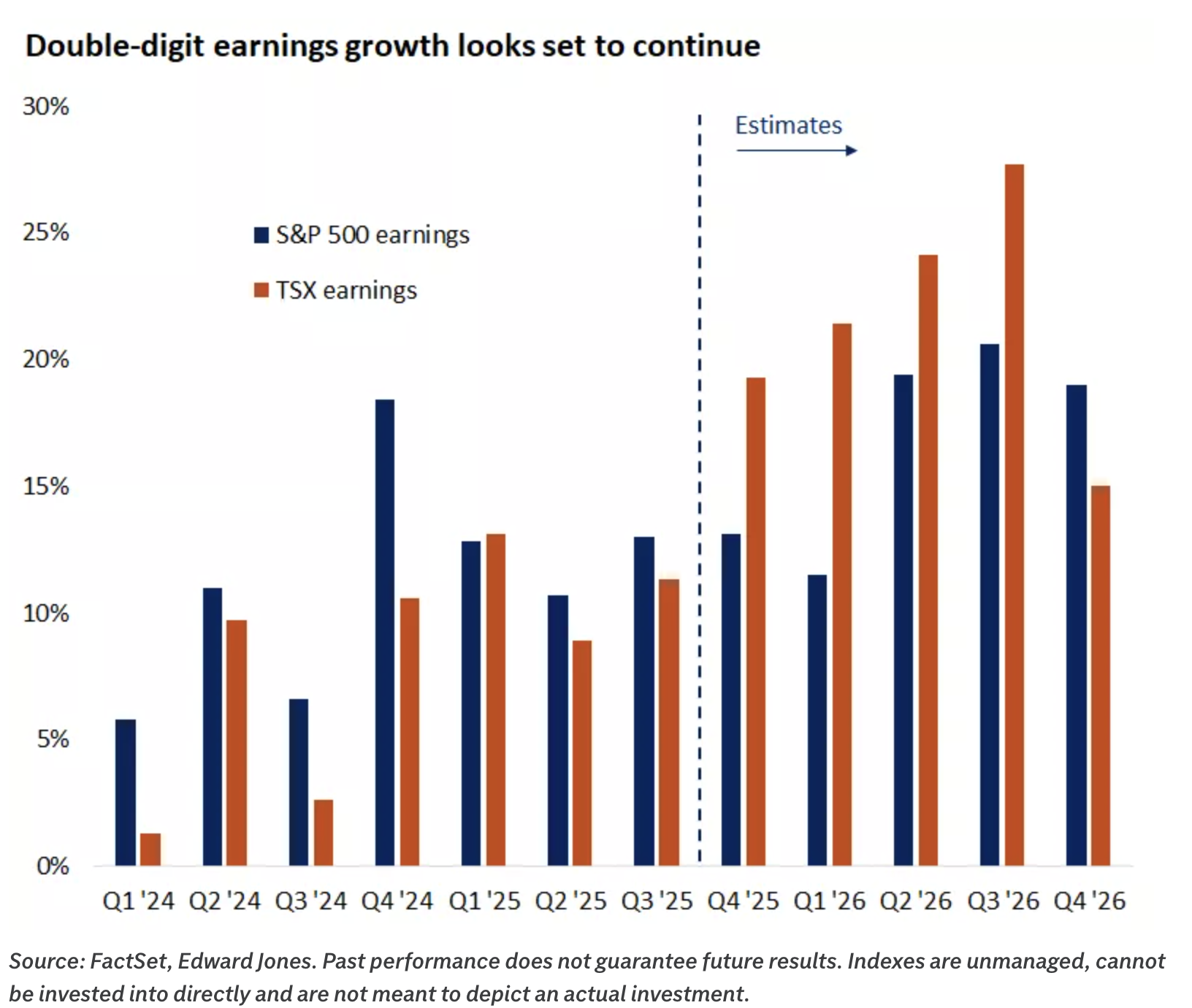

Four weeks ago, we were writing to you about oil above $100, a war in the Middle East, and markets down sharply from their January highs. This morning, it would be hard to tell any of that happened.

The S&P 500 hit a fresh record high last week. The Nasdaq is on its longest winning streak since 1992. The Dow has recouped all of its losses since the Iran conflict began. Oil is back below $100 and falling. And the TSX is trading just under 34,100 — within striking distance of its February record.

The pivot came when a ceasefire between Israel and Lebanon was announced on April 17, followed by Iran declaring the Strait of Hormuz open with full commercial shipping access for the duration of the ceasefire. Markets treated it as resolution. That’s probably a touch optimistic — geopolitical situations rarely stay tidy — but the direction of travel is clearly de-escalation.

What We’re Watching

- Whether the ceasefire holds. Everything above is contingent on the Strait staying open and the conflict staying contained. If either changes, the last three weeks of gains are the first thing the market will give back.

- The Bank of Canada. Rate path is genuinely unclear. With oil falling and the inflation pressure easing, the conversation about rate cuts is back on the table. We’ll know more over the next few weeks.

- Earnings season. Big companies start reporting this week. With markets at record highs, expectations are running hot. Any sign of weakness in corporate results could take the wind out of this rally quickly.

Final Thought

One of the things that gets lost when markets swing the way they have is the role of portfolio design.

The last four weeks are exactly what our portfolios are built for. Not because we predicted the war, or the ceasefire, or the rebound. We didn’t. Nobody did. But uncertainty itself is predictable — and a portfolio that relies on the headlines being good, or calm, or quiet, isn’t much of a portfolio.

Private credit, private equity, real estate, infrastructure, absolute return strategies — these aren’t exotic additions to a stock-and-bond portfolio. They’re the structural foundation that lets a portfolio absorb shocks without abandoning the plan. That’s why you don’t hear from us in a panic when markets move. And it’s why, when the headlines get noisy, we can tell you honestly what applies to you and what doesn’t.

If any of this has been on your mind — the private credit headlines, the war, the rally, what any of it means for your plan — reply to this email. That’s what we’re here for.

As always, if anything in this email sparked a question or you want to talk through how any of this applies to your situation, just reply. We read every one.

Until next time, stay informed and strategically invested!

Trevor