Confidence Beats a Crystal Ball

In today’s email:

- 76% of Canadians are worried they won’t have enough in retirement — but worry doesn’t equal reality

- The confidence gap: what having a plan actually does (and doesn’t) fix’

- Why inflation concerns keep growing even when inflation itself has cooled

- How markets finished the week — and what’s actually driving returns

- The real antidote to retirement anxiety (spoiler: it’s not just more money)

The Scoop

Here’s a headline you’ve probably seen in some form recently: 76% of Canadians are worried they won’t have enough money in retirement because of rising prices.

That stat comes from BMO’s latest retirement survey, and honestly, it’s not surprising. Inflation dominated the conversation for two years. Prices on everything from groceries to gas jumped. And even though inflation has cooled significantly, the feeling hasn’t fully caught up yet.

But here’s the thing — worry and reality aren’t always the same thing.

The Worry is Real (But So Is the Context)

Let’s start with what people are actually saying.

According to recent surveys from BMO, CIBC, and CPP Investments, Canadians are:

- Increasing their estimate of how much they’ll need to retire — from $1.67 million to $1.54 million on average (though even this is still down slightly from last year)

- Cutting spending in other areas to maintain retirement savings

- Planning to work longer or into retirement just to stay on track

- Feeling more anxious about outliving their savings — especially women and younger Canadians

The surveys also show that 63% of Canadians say inflation has impacted their ability to save for retirement over the past year. For many, it’s forced hard choices: reduce contributions, delay retirement, or abandon saving altogether for now.

This isn’t trivial. Real people are making real trade-offs.

But here’s where the nuance matters.

Feeling Behind Doesn’t Mean You Are

One of the more interesting findings in the data is this: people without a plan feel significantly more anxious than people with one — even when their actual financial situation isn’t that different.

In other words, the confidence gap often comes down to clarity, not just capital.

TD found that 90% of Canadians with a personalized financial plan believe it’s helping them reach their goals. Meanwhile, 54% of Canadians don’t have a plan at all — and among that group, nearly four in ten say they’d feel more confident if they had one.

Think about that for a second. The antidote to a lot of this anxiety isn’t necessarily earning more or saving more (though that helps). It’s having a roadmap that accounts for the variables you can’t control — like inflation, market returns, and how long you’ll live.

Why Inflation Still Looms Large (Even as It Cools)

Inflation has dropped. We all know this. Headline CPI in Canada is well off its highs. Central banks have started cutting rates. And yet, people are more worried about inflation now than they were a year ago.

Why?

Because inflation is cumulative. Prices didn’t go back down — they just stopped rising as fast. That means the sticker shock from 2022 and 2023 is still here. Your grocery bill didn’t reset. Your property taxes didn’t reverse. And if you’re on a fixed income or close to retirement, you’re acutely aware that your purchasing power took a hit — and it’s not coming back.

This is why retirees (and near-retirees) are especially sensitive to inflation. They’re not getting raises. They’re not seeing their paycheques grow with wage inflation. They’re living on savings, pensions, and government benefits — most of which are indexed to inflation, but often with a lag.

The good news? CPP and OAS are indexed. RRIFs and other investment income can grow if structured properly. But the psychological weight of watching prices climb doesn’t just disappear when inflation cools. It lingers.

What Actually Helps

So what’s the fix?

It’s not about predicting inflation. It’s not about timing the market. And it’s definitely not about having a million-dollar lump sum sitting in cash (which, by the way, is a guarantee that inflation will erode your purchasing power).

The fix is threefold:

1. A plan that accounts for longevity and inflation

You need to plan for living longer than you expect — not dying young. That means building income streams that last, whether through CPP, annuities, or portfolio withdrawals designed to keep pace with rising costs.

A 65-year-old Canadian woman can expect to live to 87 on average. But there’s an 11% chance she lives to 100. Planning for “average” isn’t enough.

2. Diversified income sources — and real downside protection

The smartest retirement plans don’t rely on one thing going perfectly. They blend:

- Guaranteed income (CPP, OAS, maybe a pension or annuity) to cover essentials

- Growth assets to maintain purchasing power over time

- Alternatives like private credit, private equity, and private real estate to reduce volatility and generate income in ways public markets can’t

- Flexibility to adjust when life throws curveballs

This is where a lot of traditional portfolios fall short. They’re built entirely around public market risk — stocks and bonds — which means when markets get choppy, everything moves together. And if you’re in or near retirement, that kind of volatility isn’t just uncomfortable. It can derail your entire plan.

Alternatives aren’t about chasing higher returns (though they can help with that too). They’re about creating a smoother ride. Private credit can generate consistent income without the day-to-day price swings of bonds. Private real estate offers inflation protection and diversification away from stock market gyrations. And private equity gives you access to growth that’s less correlated to what’s happening on the TSX or S&P 500.

The goal isn’t complexity for its own sake. It’s about building a portfolio that doesn’t require every assumption to be right in order to work.

3. Confidence through preparation

Here’s the part that doesn’t get talked about enough: confidence matters.

Not blind optimism. Not ignoring risk. But the kind of confidence that comes from knowing you’ve thought through the scenarios, built in redundancy and downside protection, and have a plan that doesn’t require everything to go perfectly.

The data backs this up. People with plans feel better. They sleep better. They make better decisions. And they’re far less likely to panic when markets get choppy or headlines get scary.

And when your portfolio is designed to actually absorb volatility rather than just ride it out white-knuckled? That confidence becomes a lot easier to maintain.

The Takeaway

Worry is understandable. But it’s not a strategy.

Canadians are right to think about inflation. They’re right to question whether they’ve saved enough. And they’re right to want certainty in an uncertain world.

But the real antidote to retirement anxiety isn’t just more money. It’s a plan that’s designed to absorb change rather than rely on perfect conditions.

Markets will fluctuate. Inflation will come and go. Life will be unpredictable. That’s always been true.

What matters is that your plan is built to handle it — not because you can predict the future, but because you don’t have to.

Market Minute

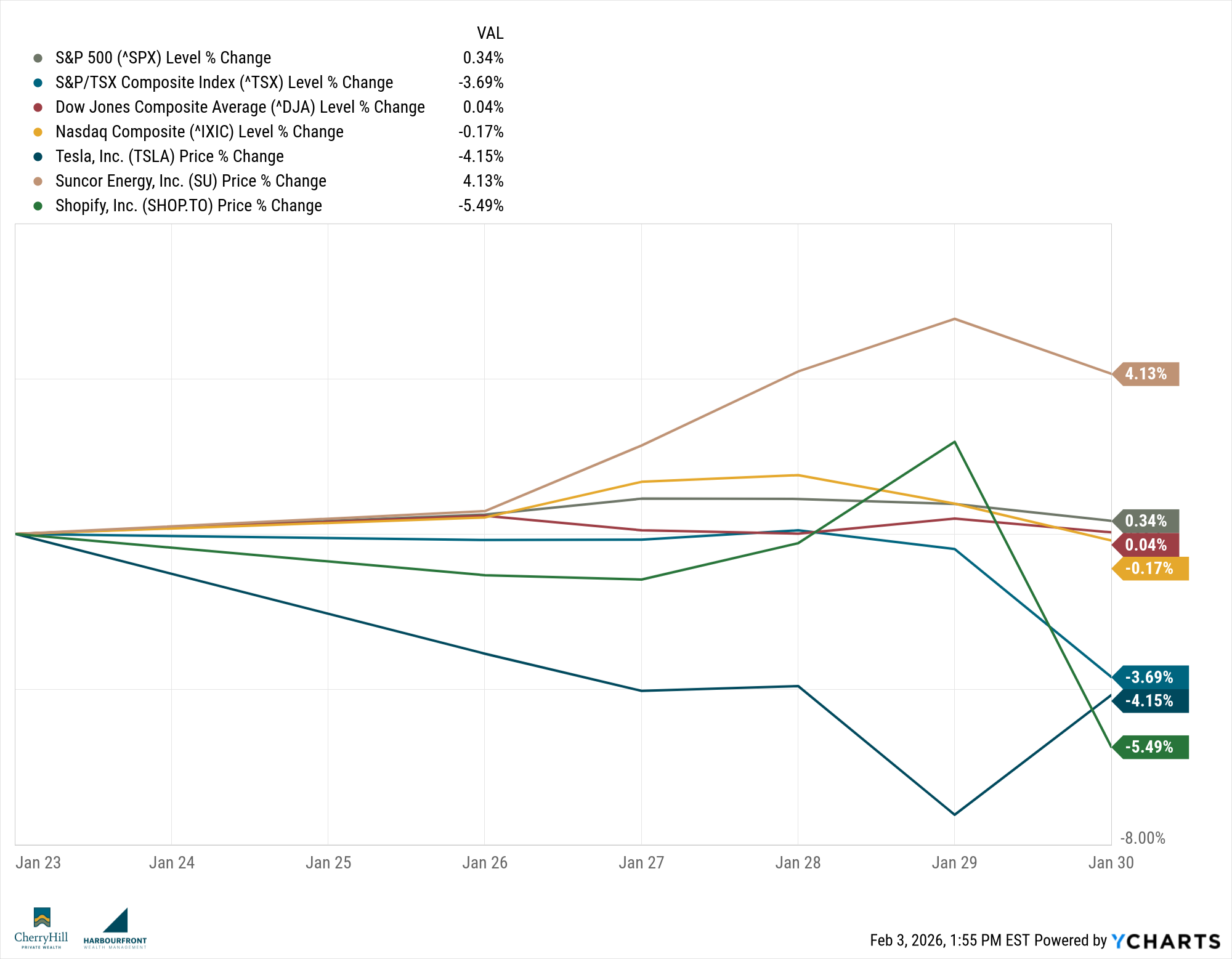

Week Ending January 2303, 2026

Last week was one of those weeks where the final score doesn’t tell the full story.

The TSX dropped -3.7% on the week — its worst showing in months — finishing at 31,924. Meanwhile, the S&P 500 gained a modest +0.3%, closing at 6,939. But if you were watching the tape, you know it felt a lot choppier than that small gain suggests.

Canadian Markets:

The TSX had a rough week, down nearly 4%, with most of the pain concentrated in energy and materials. Oil jumped +7.7% on the week (closing at $65.77), but that recovery came late and wasn’t enough to offset earlier weakness in the sector. Gold miners stabilized after a volatile stretch, but the broader resource-heavy index couldn’t find its footing.

Financials provided some support — Canada’s big banks held up reasonably well, benefiting from resilient earnings expectations and solid dividend yields. But overall, the TSX spent the week giving back some of its strong YTD gains. It’s still up +0.7% year-to-date, which is respectable, but the momentum from early January has clearly cooled.

U.S. Markets:

The U.S. painted a more constructive picture on the surface, but beneath that, there was plenty of intra-week volatility.

The S&P 500 rallied early in the week, sold off mid-week following some disappointing tech earnings reactions (Microsoft, in particular), and then steadied into Friday. The VIX — the market’s fear gauge — spiked nearly to 20 at one point, a reminder that calm markets and calm investors aren’t always the same thing.

Earnings have been solid so far. About a third of the way through Q4 earnings season, companies are beating estimates at a decent clip. The blended earnings growth rate for the S&P 500 now sits at 11.9%, up from 8.2% just a week ago. Industrials, tech, and communication services have been the main contributors.

That said, the market’s reaction to earnings has been uneven. Beat-and-raise isn’t enough anymore — investors want to see proof that AI spending is translating into actual profits, and they’re pushing back on anything that feels like over-investment or slowing momentum.

Global Markets:

International developed markets (MSCI EAFE) gained +1.6% on the week, continuing their steady start to 2026. Europe and Japan both posted gains, benefiting from more attractive valuations and some rotation out of expensive U.S. mega-caps.

This is the kind of environment where diversification quietly does its job. U.S. markets get the headlines, but international exposure has been pulling its weight so far this year.

Sector Spotlight: Central Banks on Hold

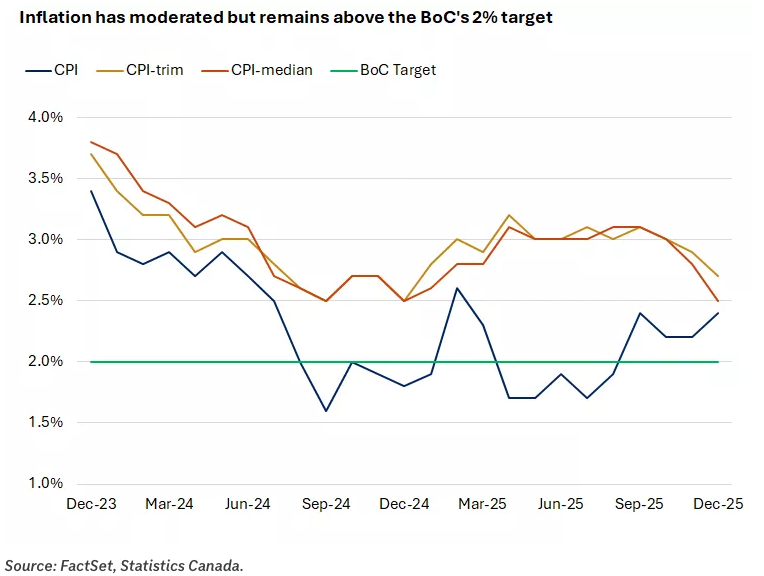

Both the Bank of Canada and the Fed held rates steady last week, as expected.

The BoC kept its policy rate at 2.25% and signaled it’s in no rush to move. Headline CPI ticked up to 2.4% in December (partly due to the GST/HST holiday base effects), and unemployment remains elevated at 6.8%. The bank is essentially saying: “We’ve done a lot of cutting. Now we wait.”

The Fed’s tone was similar. It held the federal funds rate at 3.5%-3.75% and upgraded its assessment of the economy, noting solid growth and a stabilizing labor market. But inflation is still above target, and the Fed made it clear it’s shifting to a more patient stance after three consecutive cuts late last year.

Markets are now pricing in one or two cuts for 2026 — likely starting mid-year, assuming inflation continues to cool. That’s a reasonable base case, but it also means we’re probably done with the “easy cuts” for now.

Quote of the Week:

“Inflation is benign, interest rates are trending lower and earnings are trending higher, and that’s goldilocks for stocks.”— Terry Sandven, Chief Equity Strategist, U.S. Bank Asset Management

Trends to Watch This Week:

Here’s what we’re keeping an eye on this week.

- January employment data (both Canada and the U.S.) — This will shape expectations around how much room central banks have to cut rates if growth softens.

- More mega-cap earnings — We’re still waiting on key reports from the remaining Magnificent 7 names and other bellwethers. The bar is high, and reactions have been volatile.

- Kevin Warsh nomination — Trump’s pick for Fed Chair brings a more dovish stance on rates but also strong views on shrinking the Fed’s balance sheet. The confirmation process could take time, but markets are already pricing in a shift.

The Bigger Picture

Markets are digesting a lot right now: solid earnings, sticky inflation, cautious central banks, and shifting leadership both politically and within equity markets.

The TSX had a tough week, but it’s still positive on the year. The S&P 500 continues grinding higher, though the path is getting bumpier. And international markets are quietly outperforming — a reminder that leadership doesn’t always come from where you expect.

What stood out to me wasn’t the weekly gain or loss — it was how uneven the reactions have been. Some sectors are rallying, others are getting hammered. Some stocks beat earnings and drop anyway. And volatility spiked mid-week even though markets ended relatively flat.

That’s not a sign of panic. It’s a sign of markets repricing assumptions and rotating capital. And in that kind of environment, portfolios built for resilience — not just growth — tend to hold up better.

Final Thought

The retirement surveys all point to the same thing: Canadians are worried.

They’re worried about inflation. They’re worried about running out of money. They’re worried they haven’t saved enough, started early enough, or planned well enough.

And honestly? Some of that worry is justified. Retirement is a big deal. Getting it wrong has consequences.

But here’s what the surveys also show: the people who feel the least anxious aren’t necessarily the ones with the most money. They’re the ones with the most clarity.

They know what they’re working toward. They know what their income will look like. They know their plan accounts for inflation, longevity, and the occasional market downturn. And because of that, they’re not paralyzed by every headline or survey that tells them they should be panicking.

That’s the difference between worry and confidence. And it’s exactly why planning matters.

If you’ve been putting off this conversation — whether with us, with another advisor, or even just with yourself — now’s a good time to start. Not because the world is falling apart. But because having a plan makes everything feel a lot less overwhelming.

Until next time, stay informed and strategically invested!

Trevor