A World in Transition

In today’s email:

- The end of the old global playbook — and Canada’s uncomfortable position

- What Davos really signalled (hint: it wasn’t optimism)

- Why markets shrugged off geopolitical noise (and what they didn’t miss)

- How markets finished the week — and why leadership is quietly shifting

- Why “ignore the headlines” might be the most underrated strategy for 2026

Beyond the Portfolio

A quick housekeeping note as tax season gets underway — especially helpful if you like to stay ahead of deadlines (or if you’ve ever filed too early and regretted it).

A few key dates and reminders to keep in mind:

- RRSP contribution deadline: March 3, 2026 (for the 2025 tax year)

- Tax slips arrive in waves: most between February and late March

- Non-registered and private investment slips can arrive later, and amended slips are not uncommon

- TFSA planning: contribution limits typically finalize later in Q1, which is often the best time to confirm next steps

One practical tip: if you hold non-registered investments — particularly private or partnership-style holdings — filing too early can create extra work if revised slips show up. When in doubt, waiting until late March or early April (or following your accountant’s guidance) can save headaches.

For clients, we’re rolling out a shared tax folder option this year so slips can be uploaded once and securely accessed by both you and your accountant. It’s designed to reduce back-and-forth and eliminate the need for you to play “middleman” during tax season. We’ll be sending more details in our upcoming tax-season emails.

For non-clients, consider this a simple reminder: giving yourself time — and a system — makes tax season far less stressful.

The Scoop

For most of the last 30 years, the global economic backdrop was relatively simple.

Trade expanded. Defence budgets shrank. Supply chains stretched across continents in the name of efficiency. And countries like Canada benefited enormously by sitting comfortably inside a rules-based system largely anchored by the U.S. and its allies.

That era is ending (has ended?).

At Davos, Prime Minister Mark Carney put words to something many governments and investors have been sensing for a while: the global order is shifting from cooperation to competition, from efficiency to resilience, and from clear rules to constantly changing probabilities.

This isn’t about panic — but it is about adjustment.

From Efficiency to Resilience

For decades, economic policy was built around one dominant idea: optimize for lowest cost.

That meant just-in-time supply chains, concentrated manufacturing hubs, and deep reliance on a small number of trading partners. It worked — until it didn’t.

Pandemics, wars, sanctions, tariffs, and political realignment have exposed just how fragile that system can be. Today, governments are far more focused on questions like:

- What happens if this supply chain breaks?

- What if this ally changes direction?

- What if access isn’t guaranteed anymore?

The answer hasn’t been globalization’s full reversal — but it has been a clear shift toward friend-shoring, domestic capacity, and redundancy. These choices are more expensive, but they reduce catastrophic risk.

Markets are already adapting to this reality, even if headlines lag behind.

Canada’s Trade Reality Check

Canada sits in an unusual position.

On one hand, we are deeply integrated with the U.S. economy — more than even most people realize. On the other, that reliance is now being viewed as a vulnerability rather than a strength.

The conversation in Ottawa has clearly changed. Diversifying trade relationships is no longer a talking point — it’s becoming policy. That includes:

- Deeper ties with Europe and the UK

- Expanding relationships in the Indo-Pacific

- Strategic partnerships tied to energy, critical minerals, and infrastructure

This doesn’t mean Canada is “moving away” from the U.S. But it does mean we’re no longer assuming the relationship will always be frictionless.

For businesses and investors, this introduces both opportunity and uncertainty — often at the same time.

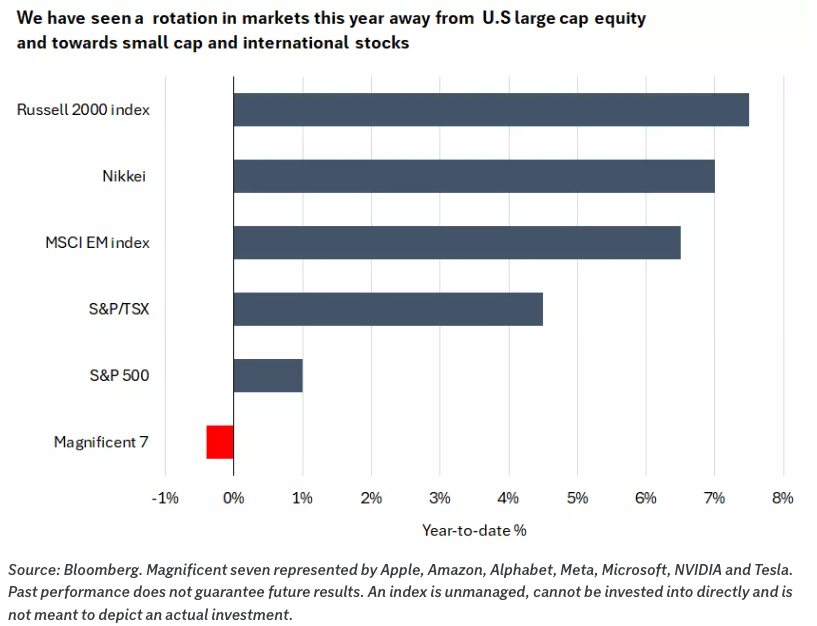

The UK and the Rise of “Middle Powers”

One of the more interesting undercurrents at Davos was the renewed visibility of countries that don’t dominate headlines — but still matter enormously.

The UK, Canada, Australia, and parts of Europe are increasingly positioning themselves as stable, investable alternatives in a more fragmented world. These “middle powers” are trying to remain open, predictable, and rules-based — even as the global system becomes less so.

For investors, this creates a different landscape:

- More dispersion between winners and losers

- More emphasis on domestic strength and pricing power

- Less tolerance for fragile business models

It also means global capital won’t flow as freely or evenly as it once did.

What This Means for Investors

When geopolitics shifts, the instinct is often to react emotionally — or worse, to trade the headlines.

Historically, that’s been a costly mistake.

A more durable approach is to recognize how these changes tend to show up in portfolios:

- Greater volatility as markets reprice probabilities

- Longer-term themes that unfold unevenly

- Periods where fundamentals matter more than narratives

This is why diversification, downside protection, and disciplined portfolio construction matter most during transitions — not after they’re complete.

The goal isn’t to predict every outcome. It’s to remain positioned so that no single assumption has to be “right” for your plan to work.

The Takeaway

The world isn’t falling apart — but it is being reorganized.

Trade relationships are evolving. Security has a price again. And countries like Canada are being forced to rethink long-standing assumptions about who they rely on and how exposed they really are.

Markets will continue to adapt, but they won’t wait for certainty. They’ll move as probabilities shift — quietly at first, then all at once.

That’s why this environment rewards patience, preparation, and portfolios designed to absorb change rather than react to it.

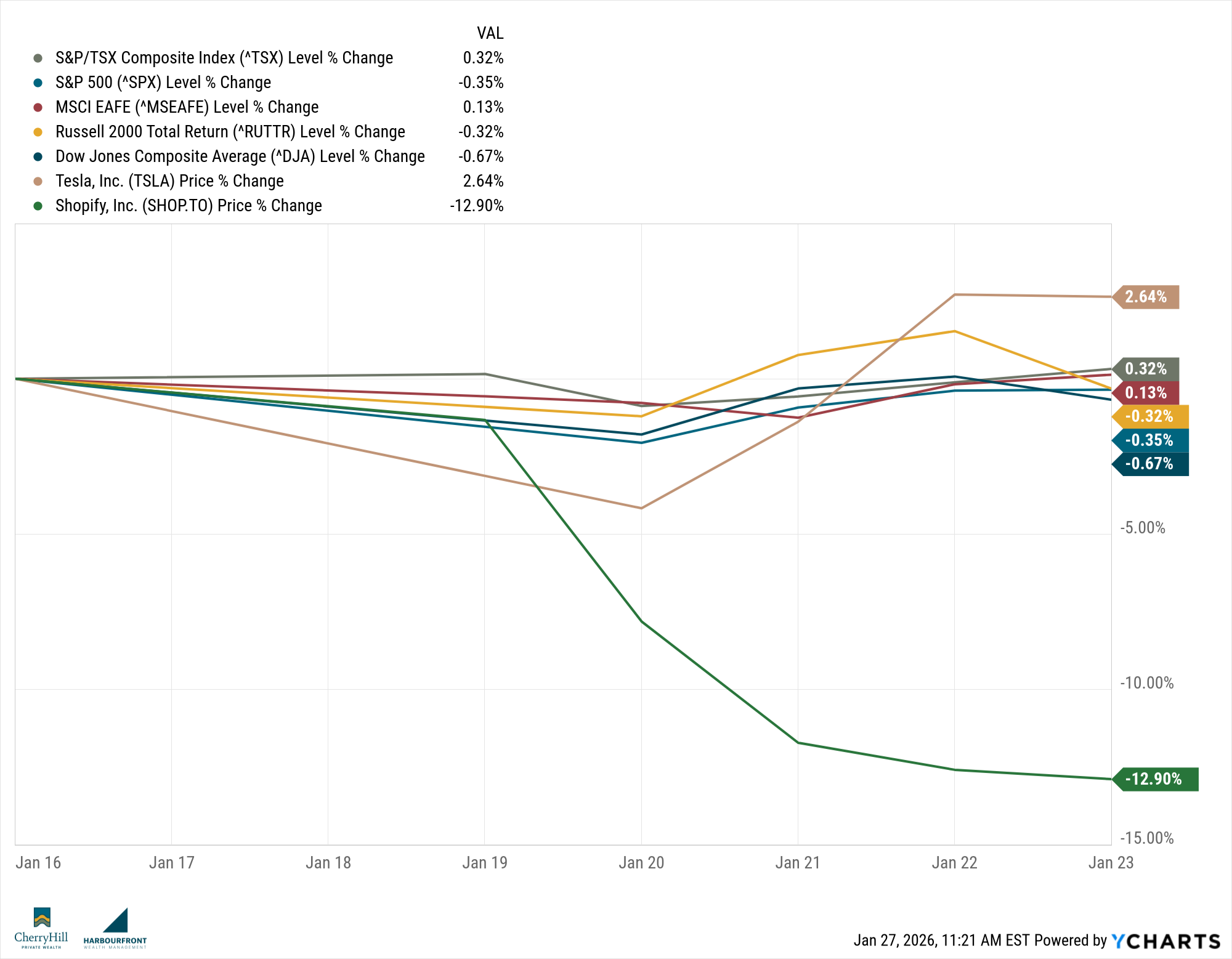

Market Minute

Week Ending January 23, 2026

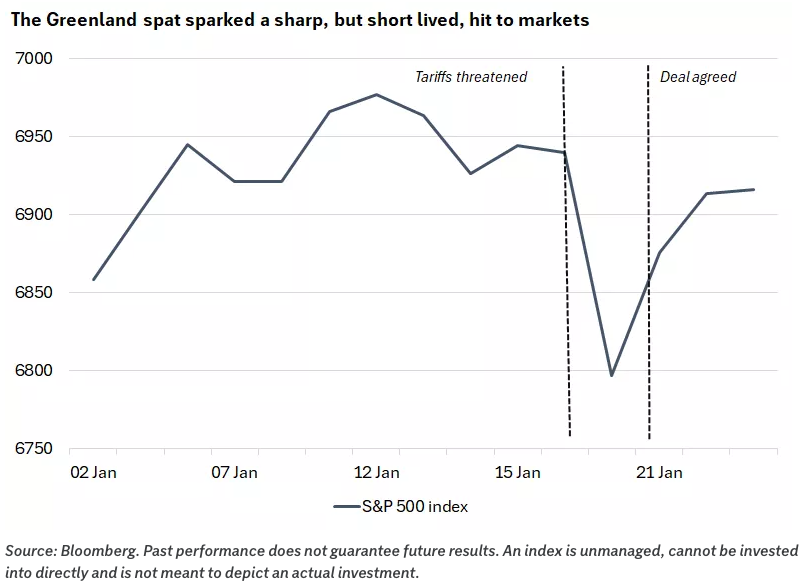

Last week was a perfect example of the market’s attention span: a scary headline hits, prices wobble, and then everyone goes right back to what actually drives returns—rates, earnings, and economic momentum. The “Greenland + tariffs” flare-up created a quick risk-off move… and then faded almost as quickly once it looked like the worst-case outcome wasn’t happening.

Canadian Markets:

TSX: 33,145 (+0.3% on the week, +4.5% YTD)

Canada quietly did what Canada often does in choppy global weeks: held up better than expected.

A big part of that resilience is what Canada owns: resources and financials—and right now, anything tied to gold has been a tailwind. Meanwhile, the inflation story at home is getting more interesting: headline CPI bumped up, but core measures appear to be cooling, which keeps the “rate cuts later, not panic now” narrative alive.

U.S. Markets:

S&P 500: 6,916 (-0.4% on the week, +1.0% YTD)

The U.S. market started the week with a punch in the mouth and finished looking… mostly fine.

What stood out to me wasn’t the weekly decline—it was how quickly the market reframed the story from “geopolitical shock” back to “okay, what are earnings doing and what are central banks doing?” That’s the tone heading into a big week: Fed meeting, heavy earnings, and a lot of “are we really seeing leadership broaden out beyond the usual names?” debate.

Global Markets:

MSCI EAFE: 2,995.99 (+0.1% on the week, +3.6% YTD)

International developed markets are starting 2026 with a bit more confidence than last year. Part of this is valuation, part is positioning, and part is simply investors being reminded that diversification isn’t a slogan—it’s a strategy that actually shows up when headlines get messy.

Sector Spotlight: Gold & “Uncertainty Hedges”

Gold remains one of the clearest tells in the market right now. It’s up ~15% year-to-date already, after a monster 2025.

That doesn’t mean you chase it—moves like that can also mean the easy money has been made near-term—but it does reinforce why small, thoughtful diversifiers can matter when investors start questioning the stability of the global backdrop.

Quote of the Week:

“It seems that every day we’re reminded… the rules-based order is fading… And faced with this logic, there is a strong tendency for countries to go along to get a long… Well, it won’t.”

— Mark Carney, Davos

Trends to Watch This Week:

Here’s what we’re keeping an eye on this week.

- Fed + Bank of Canada (both expected to hold): It’s not the decision—it’s the tone. Markets will be listening for how confident they are that inflation is cooling without growth rolling over.

- Mega-cap earnings: Apple, Microsoft, Meta, Tesla—this is a major “AI profitability” checkpoint and a test of whether earnings strength is spreading to a broader group of companies.

- Canada GDP (November): Quietly important, because it shapes how much patience the BoC has if growth stays soft but inflation keeps behaving.

The Bigger Picture

The market did what it usually does: it reacted to the headline, then zoomed out and went back to fundamentals.

Canada finished the week positive, the U.S. slipped modestly, and international markets continued their steady start to the year. Meanwhile, the real “tell” was in the supporting cast: oil up (+3.3%), CAD up (+1.5%), and Canada investment-grade bonds slightly down (-0.1%)—a mixed but very “macro-aware” tape.

If 2026 is going to be a year of shifting alliances and shifting assumptions, the playbook stays the same: stay diversified, don’t overtrade headlines, and make sure your portfolio doesn’t rely on one perfect outcome.

Final Thought

We’re not even a month into 2026, and I’m already pretty confident that this year’s theme is going to be “Ignore the Headlines.”

The year ahead feels like it could look a lot like 2025 — plenty of headline-driven volatility, with cooler heads ultimately being rewarded. That doesn’t mean there aren’t real risks out there. There are still several important factors that could influence both markets and individual portfolios in very different ways as the year unfolds.

Our job isn’t to react to every news cycle. It’s to continually assess those risks, make thoughtful adjustments where needed, and ensure portfolios are built to hold up across a range of outcomes. That means staying diversified and using all the tools available to us — including private markets and other alternatives — to help reduce risk and create a smoother investment experience over time.

Until next time, stay informed and strategically invested!

Trevor