$1,000 a Week for Life… or $1 Million Today?

In today’s email:

- A lottery headline that turns into a real-world retirement planning lesson

- $1,000 a week for life vs. $1 million today — what the napkin math actually says

- Why income, compounding, and estate planning are deeply connected decisions

- How markets finished the week — and why broader leadership matters more than short-term moves

- A team update and an expanded focus on executor and estate planning

Beyond the Portfolio

Welcome to the Team, Adam

We’re excited to share that Adam Duggan has officially joined the Cherry Hill team.

Adam brings a strong operations background and a proven focus on client excellence. His role is centred on elevating the client experience — making sure systems, processes, and follow-through work smoothly behind the scenes so that your interactions with our team feel seamless, responsive, and well-coordinated.

A big part of Adam’s work will be helping us implement and improve internal systems, allowing the team to spend more time where it matters most: with clients. As we continue to grow, this kind of operational support is essential to maintaining the level of service you expect from us.

We’re thrilled to have Adam on board and confident his impact will be felt quickly — even if much of his work happens quietly in the background.

A New Focus on Estate & Executor Planning

I’m also pleased to share that I’ve recently completed my Certified Executor Advisor (CEA) designation.

This specialization is focused on one of the most overlooked — and often most stressful — parts of financial planning: what actually happens when someone passes away.

The CEA designation goes beyond investments and tax planning. It focuses on the real-world responsibilities executors face, including coordinating legal, tax, financial, and family matters — often during an emotionally difficult time.

For clients, this means more structured guidance around:

- choosing the right executor,

- understanding executor responsibilities and risks,

- planning for estate complexity before it becomes a problem, and

- supporting executors and families through the process when the time comes.

Estate planning isn’t just about having a will. It’s about making sure the people you care about aren’t left with confusion, conflict, or unnecessary stress. This designation strengthens our ability to support that part of the planning conversation in a more practical, hands-on way.

If executor or estate planning has been on your mind — or if you’re currently acting as an executor for someone else — this is a conversation we’re happy to have.

The Scoop

A recent Canadian lottery winner made headlines for turning down a $1 million lump sum in favour of $1,000 a week for life.

At first glance, this feels like a simple math problem. Take the money now, invest it, and you’re better off… right?

But once you scratch the surface, it becomes a much more interesting planning question.

$1,000 a week works out to $52,000 per year. In very simple terms, you’d receive $1 million after just over 19 years. Live longer than that, and the weekly payments start to look pretty appealing. Live a shorter life, and the lump sum likely wins.

But of course, inflation matters. Taxes matter. Behaviour matters. And so does what you’d actually do with the money.

This is where the spreadsheet crowd and real life tend to part ways.

The Napkin Math (No Spreadsheets Required)

Let’s keep this simple.

If you took the $1 million lump sum and invested it, how much would you need to earn to replicate that $52,000 per year?

- At 5%, $1 million generates about $50,000 per year

- At 4%, it’s $40,000 per year

- At 6%, it’s $60,000 per year

So roughly speaking, you’d need to earn just over 5% annually, consistently, to “beat” the weekly payment — and that’s before taxes, before volatility, and before human behaviour enters the picture.

And unlike the lottery payment, markets don’t send you a cheque every Friday, guaranteed, for the rest of your life.

This is why the decision isn’t just about returns. It’s about certainty versus flexibility.

Why Some People Will Always Choose the Weekly Cheque

The appeal of $1,000 a week isn’t that it maximizes wealth. It’s that it removes decision-making risk.

There’s:

- no temptation to overspend early,

- no pressure from family or friends,

- no panic during market downturns,

- and no worry about running out of money later in life.

Whether intentionally or not, the winner chose guardrails.

And this thinking shows up everywhere in financial planning.

This Is the Same Question We Ask with CPP and Annuities

This exact trade-off comes up when people decide when to take CPP.

Take it early and receive smaller payments for longer — or delay it and lock in a higher, guaranteed income later in life.

It also shows up in conversations around annuities. Many people dismiss annuities outright because “I can earn more investing.” Sometimes that’s true. But annuities aren’t designed to win a rate-of-return contest. They’re designed to eliminate longevity risk — the risk of living longer than your money.

For many retirees, the most effective plans blend both:

- guaranteed income to cover essentials, and

- growth assets to maintain purchasing power and flexibility.

The lottery choice is simply an exaggerated version of the same planning decision most people face — just with bigger numbers and better headlines.

The Estate Question (This Is the Big One)

Here’s where the decision becomes very personal.

The $1,000 per week stops when you stop. There’s no residual value. No inheritance. No transfer to children or charities.

The $1 million lump sum, on the other hand, remains an asset. Whatever isn’t spent can flow through your estate, be invested tax-efficiently, donated, or used intentionally across generations.

For people with strong estate goals, that alone may tip the scale toward the lump sum — even if the math is close.

This mirrors how we think about CPP, pensions, and annuities in real planning conversations. Guaranteed income is fantastic for stability, but it often comes at the cost of legacy.

So… What’s the “Right” Answer?

There isn’t one.

The better question is:

- Do you value certainty or flexibility more?

- Are you more worried about market risk or longevity risk?

- Is your priority maximizing income, or leaving a legacy?

The smartest plans don’t pick one extreme. They balance both.

They create enough guaranteed income to sleep well at night, while keeping enough invested capital to adapt, grow, and pass on what matters most.

This lottery winner didn’t just make a money decision — they made a planning decision. And it’s one most of us will face in quieter, less headline-grabbing ways.

Market Minute

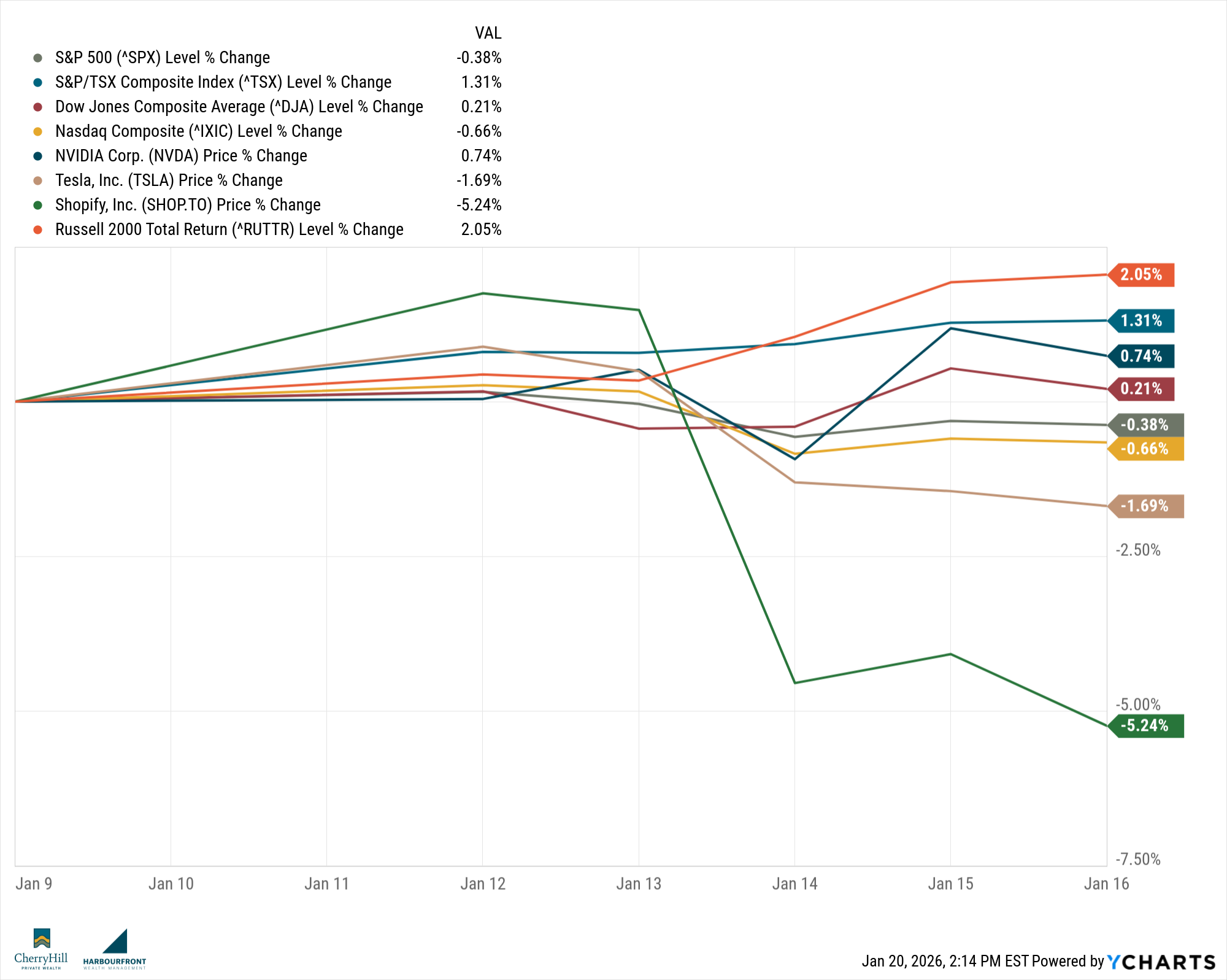

Week Ending January 16, 2026

Markets ended the week on a mixed but constructive note, with investors continuing to look past short-term headlines and focus on the bigger picture. While some of the major U.S. indexes cooled after a strong run, broader participation across regions and market segments remains an encouraging signal. The takeaway isn’t about what led this week — it’s about how diversified portfolios are doing their job as leadership continues to rotate.

Canadian Markets:

Canadian equities finished the week higher, with the TSX gaining just over 1%. Strength was supported by a relatively stable interest-rate backdrop and improving sentiment around economic resilience. While energy prices remain a headwind for certain sectors, they also help keep inflation pressures contained, which matters for both consumers and future rate policy. For Canadian investors, the message is balance: domestic markets may not be flashy, but they continue to provide steady participation alongside global exposure.

U.S. Markets:

In the U.S., markets took a breather. The S&P 500 and Nasdaq finished modestly lower on the week, while the Dow was also slightly down. This wasn’t driven by any single shock, but rather a combination of profit-taking and investor caution ahead of more earnings reports. Importantly, this pullback has been relatively orderly — not the kind of selling that signals stress. Beneath the surface, smaller and mid-sized companies held up better than the largest names, reinforcing the idea that market leadership is slowly broadening. For investors, this is a reminder that markets don’t move in straight lines, and short-term pauses are a normal (and healthy) part of longer-term growth.

Global Markets:

Outside North America, markets were generally stronger. European equities posted gains, and Japan stood out with a particularly strong week as investors responded to improving economic momentum and supportive policy conditions. Parts of Asia remain uneven — China continues to face structural challenges — but select international markets are benefiting from improving earnings expectations and more attractive valuations compared to the U.S. The key takeaway here is diversification: returns are increasingly coming from multiple regions, not just one market or one sector.

Sector Spotlight: Diversification

One of the more important developments recently has been the shift away from narrow leadership. Instead of markets being driven by a small group of mega-cap stocks, returns are spreading more evenly across sectors, company sizes, and geographies. Historically, this kind of environment tends to favour diversified portfolios and disciplined investors, rather than those chasing last year’s winners.

Quote of the Week:

“The biggest mistake investors make is to believe that what happened in the recent past is likely to persist.”

— Ray Dalio

Trends to Watch This Week:

Investors will be watching upcoming inflation data in both Canada and the U.S., along with fresh economic indicators tied to consumer spending and business confidence. These data points will help shape expectations around interest rates, but as always, one week of numbers won’t change the long-term picture on its own.

Summary

Markets may feel choppy at times, but the underlying story remains constructive. Broader participation, steady economic data, and a gradual shift away from narrow leadership are all healthy signs. For long-term investors, this is another reminder that staying diversified and disciplined matters far more than reacting to any single week’s headlines.

Final Thought

Most of us won’t be lucky enough to win the lottery and face a headline-worthy choice between income for life and a lump sum. But in reality, we make versions of this decision throughout our lives — especially as we move closer to retirement.

Whether it’s deciding when to take CPP, how much income your portfolio should generate, how much risk you’re comfortable taking, or how to balance certainty with flexibility, these are the decisions that shape long-term outcomes. They’re rarely just math problems — they involve taxes, longevity, estate goals, and, just as importantly, peace of mind.

This week’s market activity is a reminder that uncertainty is always part of investing. Markets will rotate, headlines will change, and short-term performance will never move in a straight line. That’s why the most important work happens before the decision point — building a plan that can adapt across different market environments and life stages.

And beyond investments, thoughtful planning extends to people and process as well. As our team continues to grow and as we deepen our focus on executor and estate planning, our goal remains the same: to help you navigate complex decisions with clarity, confidence, and support.

When it’s time to make the big decisions — whether expected or unexpected — we’re here to walk through every option with you, so the choice you make is the one that truly fits your life.

Until next time, stay informed and strategically invested!

Trevor