Venezuela, Oil Markets, and Why Headlines Don’t Equal Barrels

In today’s email:

- Venezuela makes headlines — but markets focus on expectations, not politics

- Why this story is about probabilities, not barrels of oil

- Early warning signs Canadian investors should be watching closely

- Winners, losers, and why time horizon matters more than the news cycle

- How markets wrapped up the first trading week of 2026

Beyond the Portfolio

Happy New Year from all of us at Cherry Hill and Harbourfront!

2025 was a year defined by the word “unprecedented,” and if the first few days of 2026 are any indication, this year may bring more of the same. Our role at Cherry Hill, alongside the team at Harbourfront, remains unchanged: to help you cut through the headline noise, protect your investments, and ensure your plan stays well positioned for the future.

We’re excited about what’s ahead in 2026 as we continue to evolve and refine both our investment process and the services we offer. Our focus remains on delivering a thoughtful, comprehensive wealth management experience — one that adapts as your needs and priorities change.

If there are services or solutions you’d like to see integrated into your relationship with us, please let us know. We’re always looking for ways to improve and expand what we offer, and the best way to do that is by hearing directly from you.

The Scoop

As we kick off the first newsletter of the year, the biggest global headline isn’t an interest rate decision or an earnings surprise — it’s Venezuela.

Over the weekend, news broke that Nicolás Maduro had been removed from leadership, setting off a wave of speculation around geopolitics, oil prices, and what this could mean for energy markets. As usual, the headlines moved faster than the facts.

Rather than viewing this through a political lens, I want to focus on what actually matters to investors: how markets price change, risk, and expectations — and where that shows up in portfolios.

This Isn’t an “Oil Shock” — It’s an Expectations Story

The first reaction many people had was simple:

“Does this mean more oil and lower prices?”

In reality, very little changes overnight.

Venezuela may hold some of the largest oil reserves in the world, but production capacity is a completely different story. Years of underinvestment, sanctions, infrastructure decay, and capital flight don’t reverse themselves because of a single event. Even under optimistic assumptions, it would take years and hundreds of billions of dollars to return production anywhere near historical peaks.

So if supply doesn’t change meaningfully in the near term, why did markets care?

Because markets don’t just price today’s reality — they price future probabilities.

Where the Market Reaction Shows Up First

Instead of watching headline oil prices, the more useful indicators are the secondary pricing signals, especially for Canadian investors.

1. Heavy Crude Differentials

One of the earliest reactions has been movement in heavy crude pricing, particularly Western Canada Select (WCS). Traders are starting to factor in the possibility — not the certainty — that Venezuelan heavy crude could eventually compete for U.S. Gulf Coast refinery demand.

That matters because:

- Gulf Coast refineries are optimized for heavy, sour crude

- Venezuelan grades are cheaper to ship than Canadian barrels

- Markets can widen differentials years before barrels ever arrive

This doesn’t hurt production tomorrow — but it can influence valuations and sentiment today.

2. The Canadian Dollar

We’ve also seen pressure on the Canadian dollar, reflecting concern that Canada’s terms of trade could weaken if future heavy crude competition increases. Currency moves are often one of the earliest signals that global investors are reassessing a country’s commodity advantage.

Again, this is about expectations, not immediate flows.

Winners and Losers — With the Right Time Horizon

This story only makes sense if we separate short-term reality from long-term positioning.

Potential Beneficiaries

- **U.S. Gulf Coast refiners: **These refineries were upgraded decades ago to handle heavy Latin American crude. If Venezuelan supply ever becomes reliable, they’re structurally positioned to benefit.

- **Integrated oil majors: **Only the largest global producers have the balance sheets, expertise, and political leverage required to invest meaningfully in Venezuela. This isn’t a space for smaller producers.

Potential Pressure Points

- **Canadian heavy oil producers: **Not because production is at risk, but because future competition can widen discounts, affecting cash flows and valuations.

- **Canadian energy-linked equities and CAD exposure: **Markets don’t wait for certainty — they adjust when probabilities change.

The Bigger Picture: Why This Matters Beyond Oil

One of the most overlooked aspects of this story is that it reinforces a broader trend we’ve been discussing for some time: energy infrastructure is increasingly treated as a strategic asset, not just a commodity business.

That has implications for:

- Capital allocation

- Sanctions policy

- Defence and national security spending

- Who global investors are willing to trust with long-term capital

This is where the second-order effects often create both risk and opportunity — long before they show up in headline data.

Market Minute

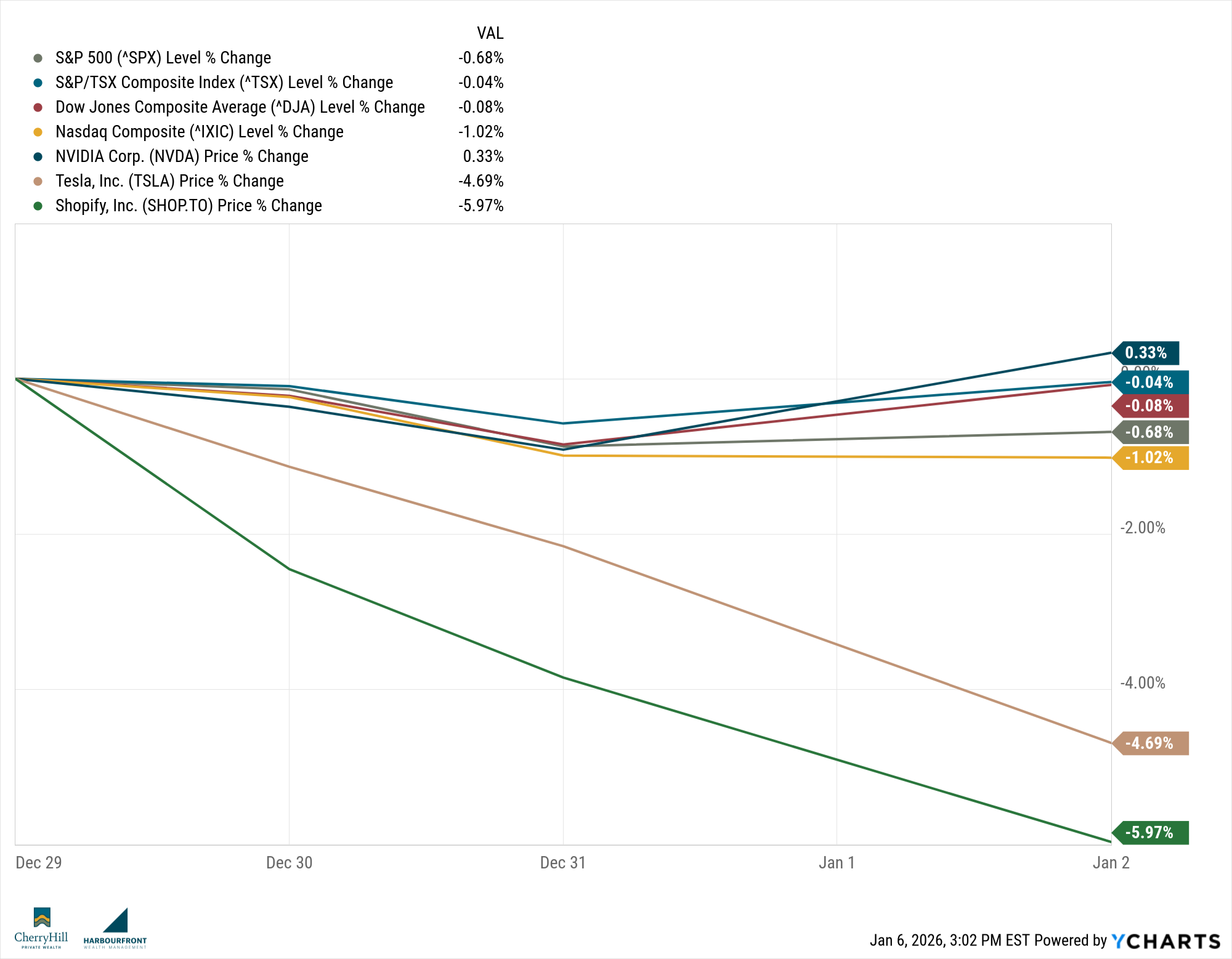

Week Ending January 2, 2026

Markets closed out the first trading week of the year on a cautious but steady note, with lighter holiday volumes giving way to early positioning for 2026. Investors began the year balancing optimism around potential rate cuts later in the year with lingering uncertainty tied to inflation, energy markets, and global geopolitical developments.

Canadian Markets:

Canadian equities finished the week modestly lower. The TSX was pressured by weakness in the energy sector as heavy crude differentials widened, while materials also weighed on returns. Financials were mixed, as investors continued to debate the timing and pace of interest rate cuts from the Bank of Canada. The Canadian dollar weakened against the U.S. dollar, reflecting softness in commodity prices and global risk sentiment.

U.S. Markets:

U.S. markets were mixed to slightly higher. The S&P 500 and Nasdaq ended the week relatively resilient, supported by strength in large-cap technology and growth-oriented stocks. In contrast, the Dow Jones Industrial Average lagged, weighed down by industrials and energy-related names. Investors continued to favor companies with strong balance sheets, consistent cash flows, and pricing power.

Global Markets:

International markets showed mixed performance. European equities were relatively stable as investors digested slowing economic data alongside expectations that central banks may begin easing policy later this year. Asian markets were mixed, with ongoing concerns around China’s economic recovery offset by modest gains in Japan, supported by currency dynamics and export-oriented sectors.

Sector Spotlight: Energy

Energy stocks underperformed this week, particularly in Canada, as markets reacted to shifting expectations around heavy crude supply dynamics following developments in Venezuela. While there is unlikely to be any meaningful change in near-term oil supply, markets began pricing in potential long-term competition for heavy crude demand, contributing to wider WCS differentials. This serves as a reminder that energy markets often react to future probabilities well before fundamentals actually change.

Quote of the Week:

“The biggest investing errors come not from not from factors that are informational or analytical, but from those are psychological.”

— Howard Marks, co-founder of Oaktree Capital Management

Trends to Watch This Week:

Here’s what were watching this week:

- Heavy crude pricing: Movements in WCS vs. WTI as markets reassess longer-term supply expectations

- Currency markets: Canadian dollar reaction to energy and commodity trends

- Interest rate expectations: Any shifts in economic data that could influence central bank policy outlooks

Summary

The first week of the year set a familiar tone: markets remain cautious, selective, and forward-looking. While headlines may drive short-term volatility, investors continue to focus on fundamentals, expectations for monetary policy, and how global developments translate into pricing signals across sectors.

Final Thought

When uncertainty rises, the most important thing investors can do is take a step back and trust the process. Our investment philosophy remains anchored in protecting on the downside, while staying positioned to participate when markets move higher.

If 2025 taught us anything, it’s that headlines and market movements often don’t move in logical or linear ways. Markets reacted to narratives, emotions, and shifting expectations far more than to fundamentals. That disconnect is exactly why a disciplined, diversified approach matters — especially during periods of elevated uncertainty.

Until next time, stay informed and strategically invested!

Trevor