Is the AI Boom a Bubble —

or Just Getting Started?

In today’s email:

- Cherry Hill is on the move!

- Are we living through an AI boom — or the early signs of a bubble?

- Why regulators and big pension funds are starting to raise caution flags.

- What a cooling AI market could mean for your portfolio (and who gets hurt most).

- Markets rebound as investors eye potential rate cuts and year-end trends.

- A timeless investing reminder from Howard Marks: preparation over prediction.

Beyond the Portfolio

Our team is very excited to announce the official opening of our new Burlington office. It took some time for it to be built out, but we’re now all moved in.

We are located at:

1001 Champlain Ave, Suite 108

Burlington, ON

L7L5Z4

We hope to welcome you in person soon!

The Scoop

Why the biggest market theme of the decade may be entering a new phase.

Artificial intelligence has dominated every financial headline this year, and for good reason: the technology is extraordinary, the pace of adoption is staggering, and for many companies, AI has transformed from a competitive advantage to the cost of entry. But when one theme drives such a large portion of market returns — and when expectations rise far faster than revenues — it’s natural to ask whether enthusiasm is turning into something more speculative.

Over the past few weeks, that question has taken on new urgency. Regulators, institutional investors, and even some of the companies at the centre of the boom have started signalling that valuations may be running too hot, too quickly. That doesn’t mean AI is going away. Far from it. But it does mean this is a good moment to step back and look carefully at what’s unfolding — and what it could mean for your portfolio.

A Growing Debate: Is AI Entering Bubble Territory?

Bubbles are never obvious until after they burst, but you can usually see the signs forming. Rapid capital inflows, soaring valuations, and a widespread belief that “this time is different” tend to appear right before things get uncomfortable. And we’re seeing early hints of that today.

In its most recent Financial Stability Report, the Bank of England flagged the rapid rise in AI-linked equities — combined with a surge in leverage across corporate credit markets — as a potential risk to financial stability. It’s unusual for regulators to single out a specific technology trend, and it reflects how quickly expectations have grown. At the same time, several major UK pension funds — managing hundreds of billions of dollars — have begun trimming U.S. tech exposure specifically because they view the space as over-concentrated and priced for perfection. When the most conservative, long-horizon investors start reducing their allocation to a sector, it’s worth paying attention.

Even the market’s current darlings aren’t immune. Nvidia, despite delivering standout results, has faced bouts of volatility as investors weigh lofty expectations against rising competition and the hard reality that no company can grow exponentially forever. It’s a reminder that when a theme becomes crowded, even good news can fail to lift a stock.

What Happens if AI Expectations Cool?

If we do see an AI bubble form — and eventually deflate — the companies most exposed will be the ones whose valuations expanded the fastest and furthest. Chipmakers, cloud infrastructure providers, and second-tier AI software firms have seen extraordinary inflows, often ahead of revenue. These were the market’s big winners on the way up, and history suggests they would feel the most pressure on the way down.

A useful comparison is the dot-com era. The internet didn’t fail — it changed the world — but many of the companies built around it didn’t survive the transition from excitement to earnings. The same could unfold here: AI will continue to advance, but not every company associated with the theme will grow into its stock price.

A Helpful Lens: The “Winner-Takes-Most” Outcome

To put this in perspective, I often look at commentary from Scott Galloway, a marketing professor at NYU and a long-time analyst of technology trends. He recently summed up the dynamic by saying, “AI doesn’t end in failure — it ends in consolidation.” His view is that the sector is unlikely to crash in the traditional sense. Instead, a handful of companies may end up capturing an overwhelming share of the economic value while dozens — maybe hundreds — of competitors fall behind.

We’ve seen this play out before: smartphones, cloud computing, social media. In each case, the technology succeeded beyond anyone’s expectations — but the returns flowed to only a very small group of firms.

If AI follows that path, the question becomes less about whether AI is the future (it likely is) and more about which players have the scale, capital, and infrastructure to remain dominant. Betting broadly on “AI everywhere” may not work. Being selective — and staying diversified — matters more.

How to Invest When Hype Runs Ahead of Reality

The good news is that you don’t need to predict which company will win the AI race to build a resilient portfolio. In periods where markets become overly concentrated in a single theme, well-diversified portfolios tend to hold up better — and sometimes significantly outperform when the air comes out of the balloon.

Private credit, private real estate, and infrastructure have continued to attract institutional capital precisely because they aren’t driven by daily market sentiment. They offer income, stability, and low correlation at a time when public markets are increasingly tied to a small number of tech giants.

Bonds also come back into focus in this environment. If we see volatility pick up or growth expectations cool, yields may stabilize or fall, creating a supportive backdrop for fixed income.

Gold and real assets remain helpful diversifiers when uncertainty rises. They aren’t meant to replace equity exposure — they’re meant to balance it.

And holding measured exposure to the strongest AI leaders is still sensible. If consolidation happens, the winners could generate meaningful long-term returns. The key is ensuring AI excitement doesn’t overwhelm the rest of your financial plan.

Why This Matters Now

AI is likely to be the defining technology of the next decade. But even the right technology can be the wrong investment at the wrong price. When valuations start leaning more on hope than on earnings, it’s important to keep a level head and remember that investing is ultimately about durability, not headlines.

A portfolio built with balance — blending public markets with private assets, growth with stability, and innovation with real cash flow — puts you in a position to benefit regardless of whether AI continues to soar, cools off, or goes through a period of consolidation.

We don’t need to fear an AI bubble. We just need to be prepared for whatever shape it takes.

Market Minute

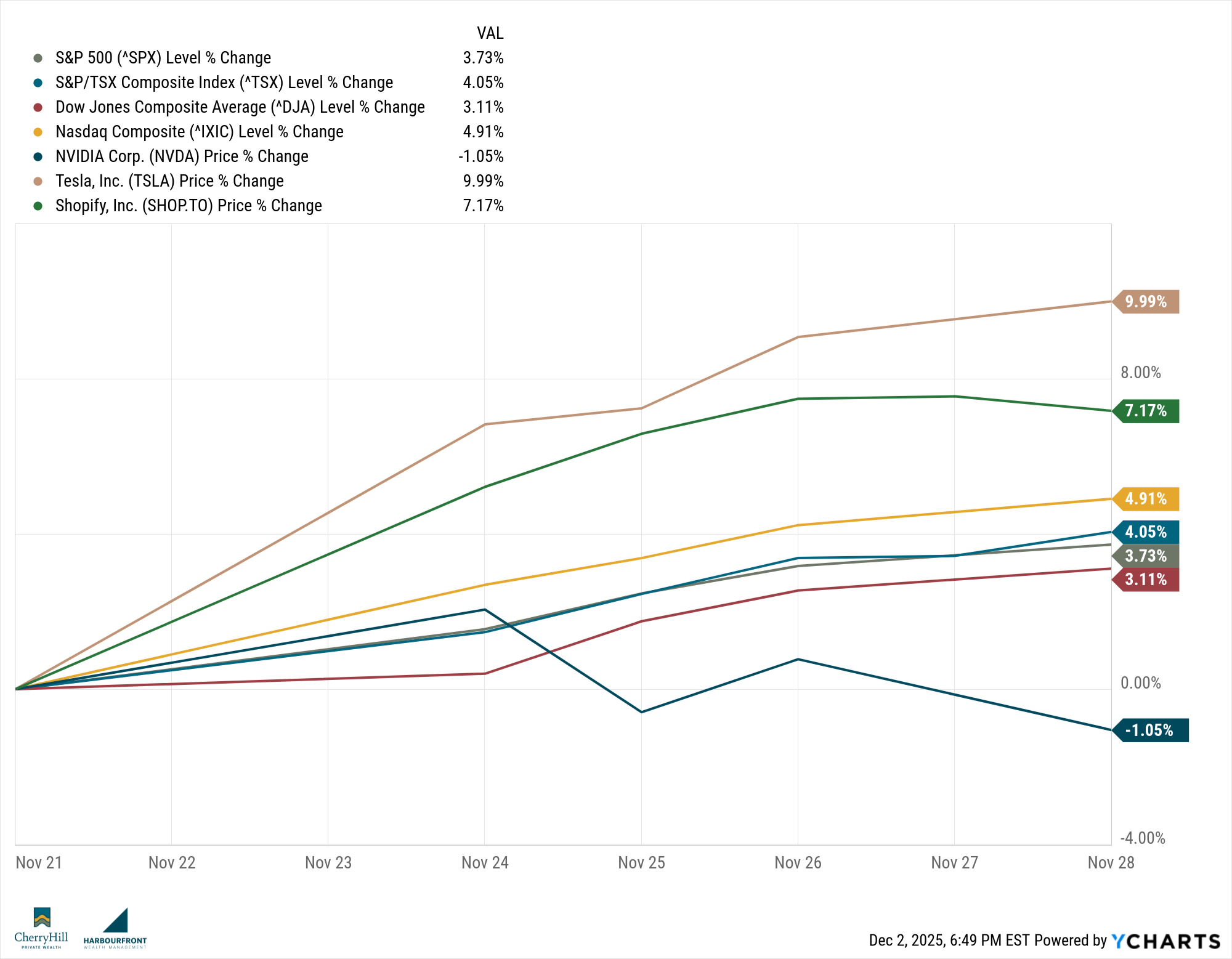

This past week, markets enjoyed a generally positive tone as investors seemed encouraged by soft economic data and growing expectations the Federal Reserve may cut rates in December — a dynamic that’s helped stabilize equities. While volatility remains under the surface, the rebound from recent turbulence suggests investors remain open to selective risk-taking going into year-end.

Canadian Markets:

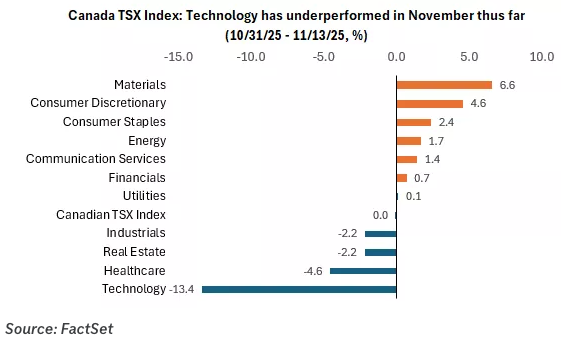

The S&P/TSX Composite Index (TSX) remains on pace for one of its strongest calendar-year performances since 2009. The Canadian market continues to benefit from broad leadership across sectors, with materials, energy, and industrials among the stronger performers — helping offset softness in other areas.

U.S. Markets:

U.S. equities rebounded this week. The S&P 500 snapped back from a recent dip, on track for a roughly +3.75% weekly gain as it closed out the week. Market leadership has broadened: energy and consumer discretionary helped carry gains, while healthcare — which lagged — remains relatively more attractive on a sector-rotation basis.

Global Markets:

International equities also held up well. Many developed-market and emerging-market indexes outperformed U.S. equities this week — a trend supported by stronger relative economic activity abroad and modest currency shifts. That said, fixed income remains under pressure, with bond yields ticking up modestly — a reminder that global markets remain sensitive to rate and policy shifts.

Sector Spotlight: Rotation Into Value & Income Traits

What stands out this week is a subtle but meaningful shift: investors seem to be repositioning away from purely high-growth or speculative sectors, in favour of companies and sectors with stronger cash flows, earnings stability, and value traits. On the S&P 500, energy and consumer discretionary led the rebound, while sectors like healthcare and industrials look increasingly attractive compared with stretched tech valuations.

In Canada, materials and industrials remain among the standouts, riding strength in commodities and resilient domestic demand. This rotation suggests many investors are quietly tilting toward what they see as “safer growth” — not because they’re abandoning growth altogether, but because they’re becoming more selective about where they place their bets.

Quote of the Week:

“You can’t predict, but you can prepare.”

— Howard Marks, co-founder of Oaktree Capital Management

Trends to Watch This Week:

Here’s what were watching this week:

- Interest-rate expectations — Markets remain focused on signals from the Fed and global central banks; any shift could ripple widely through stocks, bonds, and currencies.

- Earnings season (especially banks and cyclicals) — With macroeconomic data soft and volatility high, earnings from financials, energy, and materials firms will be scrutinized as potential bellwethers for broader risk appetite.

- Year-end positioning / flow into income and value — With many funds and institutions rebalancing, there could be more rotation toward dividend-paying or undervalued names — especially if risk sentiment stays cautious.

- Global growth signals — especially outside the U.S. — Strength or weakness in Europe, Asia, or emerging markets could influence whether international equities continue to outperform.

Summary

After a turbulent 2025, markets ended this week with a firmer footing. Optimism around potential rate cuts, sector rotation toward value and earnings-rich names, and improving sentiment have helped send both Canadian and U.S. markets higher. That said, risks remain — valuations remain elevated for many growth-oriented names, and global uncertainty still looms.

For investors — especially those like us focused on alternative assets, downside protection, and long-term cash flow — this environment underlines the value of diversification. If the year-end rally holds, all the better. But if markets stumble again, having exposure beyond hyper speculative tech could make the difference between a rough patch and a real setback.

Final Thought

We’re officially in the final month of the year, and what a year it’s been. As we rip off the last page in our 2025 calendar, I can’t help but look back on the road that got us here. Over the next few weeks, I’m planning to take a bit of time to reflect before shifting my focus fully to 2026 and beyond. It’s been a year of ups and downs and plenty of uncertainty, but we’ve managed to navigate it together.

I hope you’re also able to find a little time during the holiday season to pause, take stock of the past year, and enjoy a few quiet moments with friends and family. There’s still more to come before we officially close out 2025, but this feels like the right moment to take a breath before the final stretch.

Until next time, stay informed and strategically invested!

Trevor