Sentiment ≠ Reality:

Why You Might Be Feeling the Wrong Thing

In today’s email:

- Markets are rising — even as consumer sentiment sinks

- What ClearBridge’s recession dashboard says about what’s next

- Why feelings ≠ facts when it comes to the economy

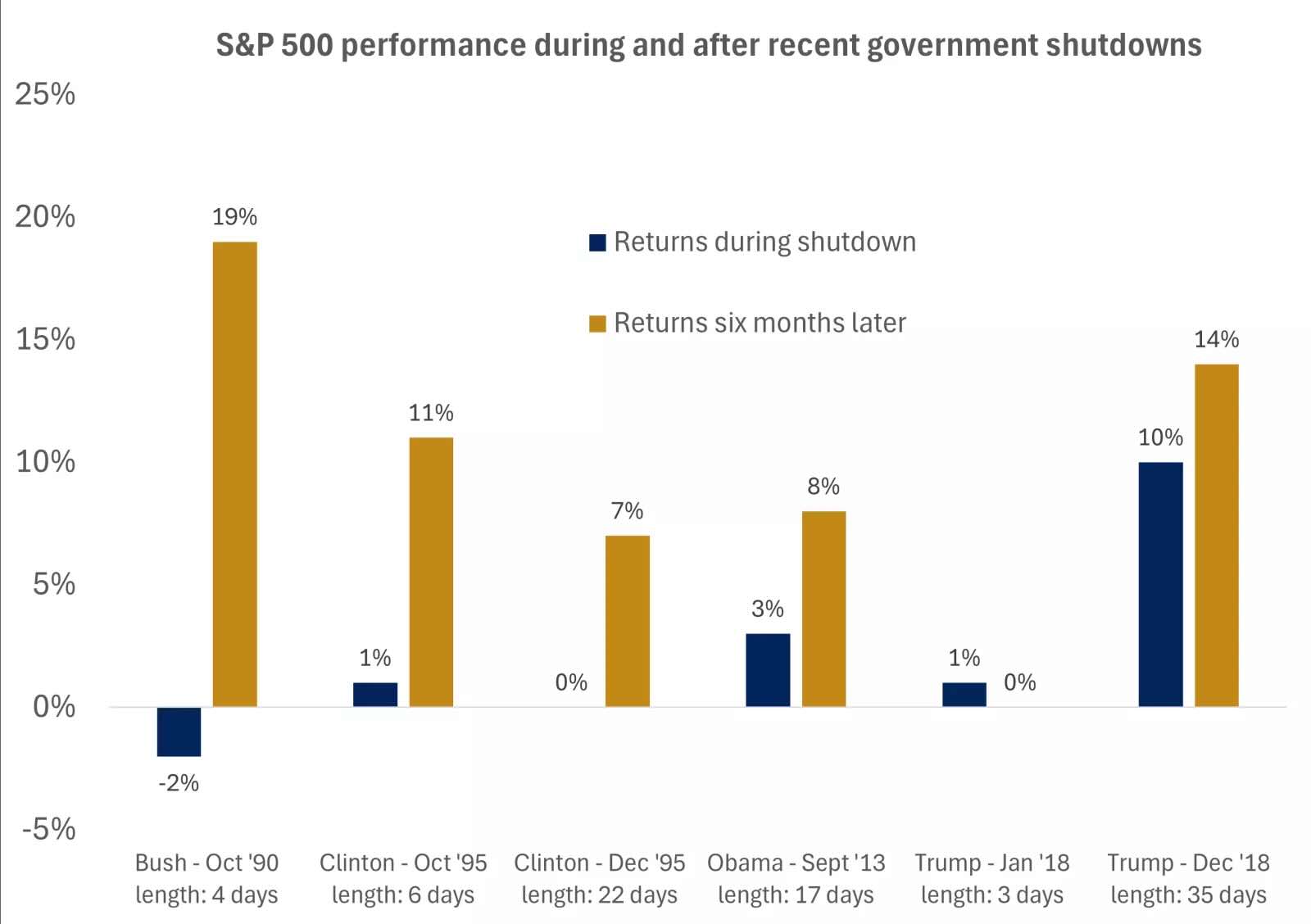

- The U.S. government might be shutdown, but the markets aren’t

Beyond the Portfolio

This week, the Cherry Hill team is out of the office attending our annual Harbourfront conference — a gathering of some of the top minds in the financial industry. It’s an opportunity for us to sharpen our skills, hear from industry leaders, and stay ahead of the curve so we can continue delivering the kind of advice and planning that helps you reach your goals.

While we’re away, Christine is holding down the fort. If anything urgent comes up, she’s available and happy to assist.

We’ll be back soon with fresh ideas, new insights, and even more tools to support your financial journey.

The Scoop

I recently sat down with Dave Wahl from ClearBridge for a wide-ranging webinar that will be released publicly in the coming days. We unpacked what the data says about the economy, how emotions are driving the narrative, and how investors can make sense of it all.

The timing couldn’t be better. Both in Canada and the U.S., we’re seeing a strange divergence: people feel like things are bad — but the data says otherwise.

Take this recent CNN article for example. It highlights a growing disconnect: consumer sentiment remains near recessionary levels, even while spending, travel, and job growth continue at a healthy pace. A similar story is playing out in Canada, as shown in a Wealth Professional piece that found more than half of Canadians think we’re already in a recession.

So what gives?

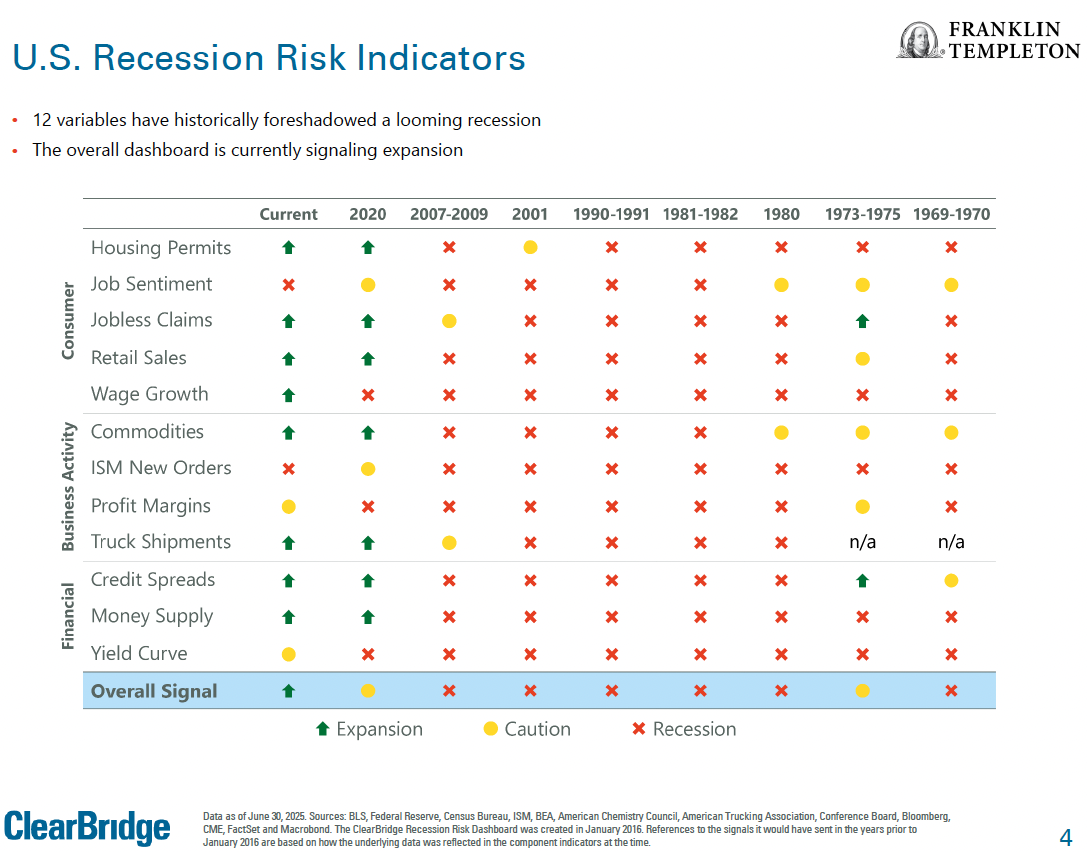

What Dave’s Dashboard Says

Dave shared the ClearBridge “Recession Risk Dashboard,” a tool that tracks 12 key economic indicators — things like jobless claims, retail sales, credit spreads, and the yield curve. As of June 30, the dashboard shows 7 of the 12 indicators as green — signaling economic expansion rather than contraction .

Here are a few key highlights from the discussion and the report:

- Jobless claims remain low, despite seasonal “speed bumps” over the summer.

- Core GDP is still growing, albeit more slowly — but that’s common in a maturing economic cycle.

- Consumer confidence, while low, has historically acted as a contrarian indicator. As noted in the report, past troughs in sentiment have often been followed by strong 12-month equity returns, averaging 25%.

In short: feelings ≠ facts.

Why We’re Feeling Recessionary (Even If We Aren’t)

It’s not hard to understand why people feel pessimistic. Prices are higher, mortgage payments have jumped, and headlines keep reminding us of geopolitical turmoil. Emotional fatigue is real.

But as investors, we need to be data-driven.

One particularly telling insight: while Canadians report feeling worse about their financial situation, consumer spending hasn’t collapsed. In the U.S., travel is booming, and retail sales are healthy. This divergence between sentiment and spending is one of the key reasons why traditional recession warning signs aren’t flashing red.

What to Do About It

This is where financial planning earns its stripes. In environments like this:

- Stay invested, but be selective — many of the largest U.S. stocks are trading at extremes, while international and value stocks are showing signs of leadership again.

- Use sentiment as a signal, not a guide — remember, the best buying opportunities often come when people feel the worst.

- Diversify — we continue to focus on private alternatives, income-generating strategies, and downside protection. If you’re relying solely on headlines to manage your money, you’re flying blind.

The Takeaway

It’s easy to feel like a recession is just around the corner, but the data — and the experts — are telling a different story. Our job is to keep our heads clear and portfolios aligned to the facts, not the fear. The biggest risk right now might not be an economic crash — it’s making decisions based on emotion, not evidence.

If you’d like to chat more about how we’re positioning for the months ahead — or want access to the webinar before it goes public — just reply to this email. Happy to share.

Market Minute

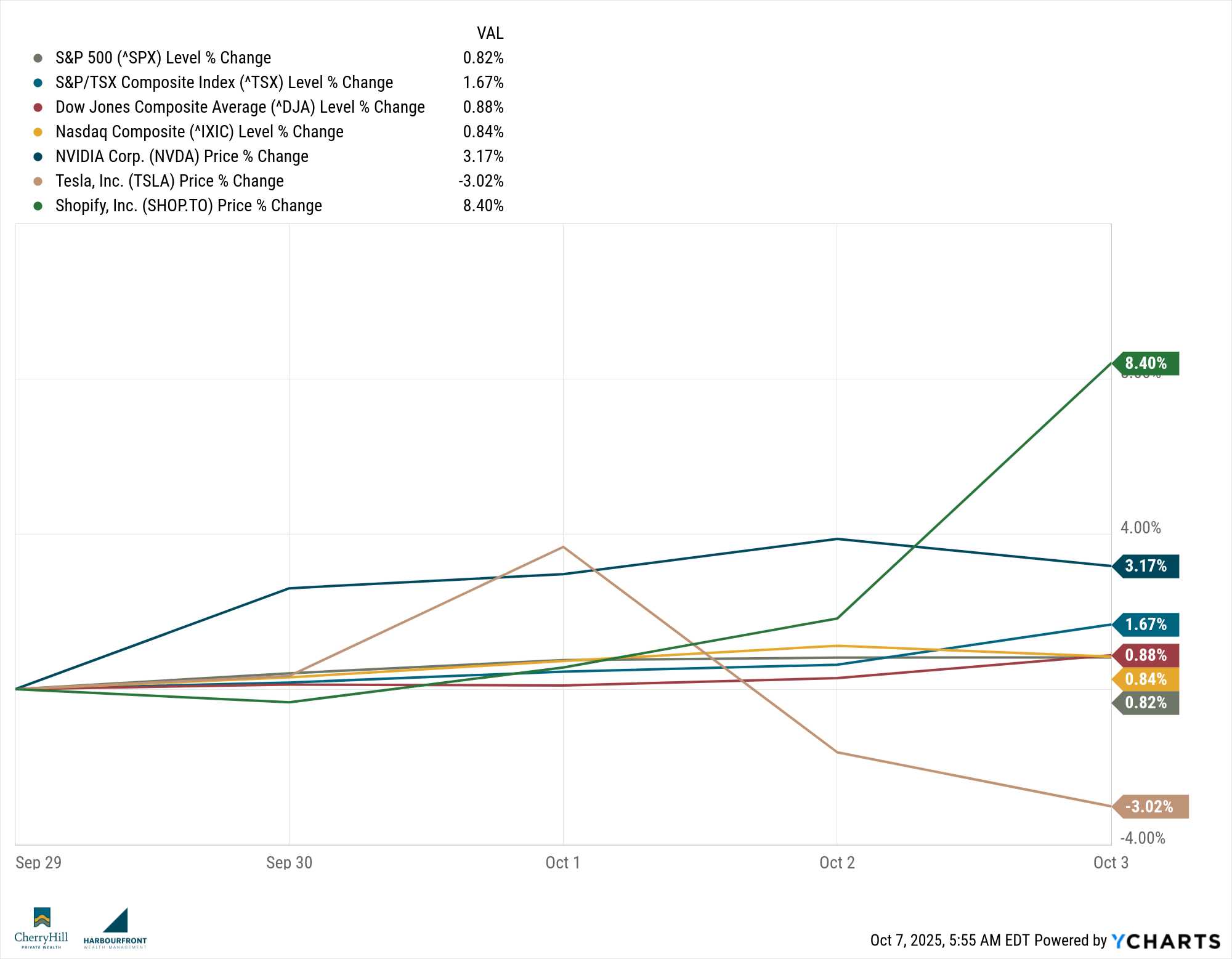

Markets rallied last week despite political noise and a partial U.S. government shutdown. Investor sentiment remains cautiously optimistic as strong economic indicators and ongoing tech strength helped push indices higher. With the official jobs report delayed due to the shutdown, markets leaned on alternative data sources, which suggested a gradually cooling—but still resilient—economy.

Canadian Markets:

The TSX rose approximately 2.4% last week, lifted by strength in rate-sensitive sectors and cyclicals. Canadian equities were also supported by improving global sentiment, particularly in the tech and industrial sectors. While commodity prices softened slightly, especially in oil, the broader market remained resilient. Year-to-date, the TSX has gained over 23%, reflecting stronger investor appetite for equities amid easing inflation pressures and expectations of lower interest rates.

U.S. Markets:

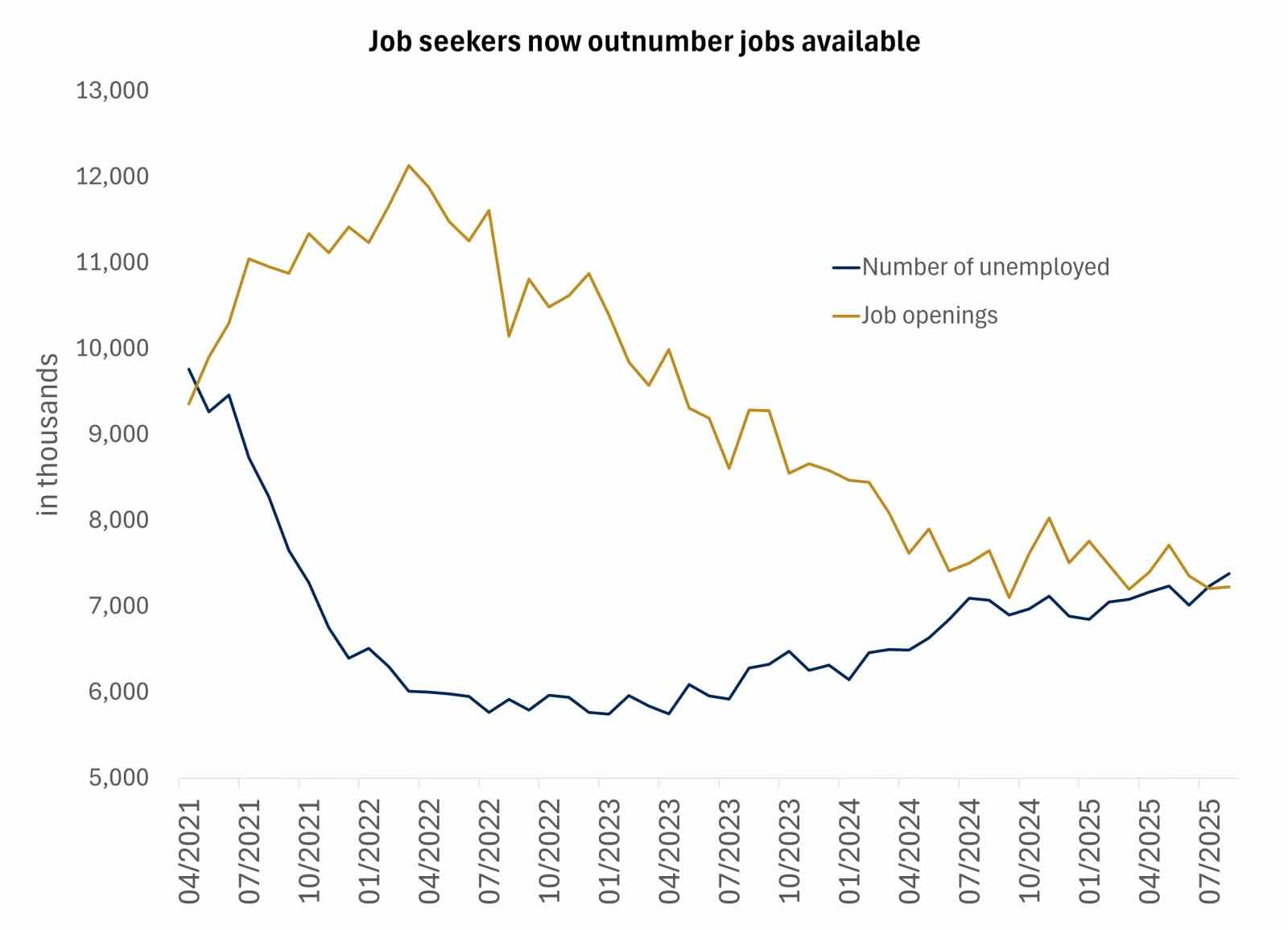

U.S. indices were also positive, with the S&P 500 advancing 1.1% for the week, bringing its year-to-date return to 14.2%. The Nasdaq once again led the way, buoyed by large-cap tech strength and ongoing enthusiasm for AI-related investments. Despite the lack of official labor market data due to the government shutdown, markets remained steady, with private data showing mixed signals. ADP private payrolls showed a modest decline, and job openings have started to dip below the number of unemployed—potential signs of a softening labor market. Even so, the broader narrative remains constructive: consumer spending is strong, GDP forecasts are being revised higher, and many investors see a Federal Reserve pivot on the horizon. Small- and mid-cap stocks also posted solid gains, with the Russell 2000 index up nearly 12% in Q3, as investors look beyond the mega-cap names.

Global Markets:

Global equities followed suit, with the MSCI EAFE index (representing developed markets outside North America) up 2.5% for the week. Optimism around a weaker U.S. dollar and improving European economic data helped drive performance. Canadian bonds also gained slightly, with investment-grade fixed income up 0.3%, while the Canadian 10-year yield dipped to around 3.15%. The energy sector saw some weakness as oil prices dropped 7.7%, but this helped ease inflation expectations, a net positive for rate-sensitive sectors. The Canadian dollar was flat to slightly lower against the U.S. dollar, reflecting a mixed commodity outlook.

Sector Spotlight:

Tech continues to be the market’s primary engine, but the broadening of leadership is worth noting. Investors are increasingly rotating into mid-cap names, industrials, and dividend payers—signaling a market that’s becoming less concentrated and more balanced. Energy gave back some recent gains, but real estate and consumer discretionary sectors showed signs of strength.

Quote of the Week:

“Consumer sentiment has historically been a contra-indicator for equity investors when hitting extreme levels.”

— David Wahl, ClearBridge Investments, Anatomy of a Recession, Q3 2025

Trends to Watch This Week:

Here’s what were watching this week:

- Canadian employment report — critical for gauging whether the labour market remains resilient.

- U.S. consumer credit & wholesale inventories — these could offer early clues in the absence of official data.

- Michigan sentiment index — to see whether consumer mood shifts further, or shows signs of stabilization.

- Earnings season kickoff — Profit reports will give further confirmation (or challenge) assumptions around margins and growth.

Summary:

Despite consumer pessimism and political uncertainty, the data continues to support a cautiously optimistic outlook. The U.S. shutdown has temporarily limited the flow of economic data, but investors seem comfortable looking through the noise. As we discussed recently with Dave Wahl, markets and sentiment don’t always move in sync—especially in a late-cycle environment. For now, equity markets remain firm, and any pullbacks may present an opportunity rather than a red flag.

Final Thought

As we head into Thanksgiving, it’s a natural time to reflect — not just on gratitude, but on what really matters. The markets will always have noise, the headlines will always shift, and there will always be debates about what’s next. But what doesn’t change is our commitment to helping you build a plan that’s grounded, intentional, and designed to weather all seasons.

From all of us at Cherry Hill, thank you for trusting us with such an important part of your life. We’re grateful for the opportunity — and excited for what’s ahead.

Until next time, stay informed and strategically invested!

Trevor