Rent vs. Buying:

A New Take on an Old Debate

In today’s email:

- What happens when you apply the same leverage used in home buying to investing instead—and how the results compare over a decade..

- Canadian markets inch higher, U.S. investors brace for a potential shutdown, and global sentiment holds steady despite rising oil prices.

- Tech remains dominant as AI-related fund inflows continue to support growth names.

- Quote of the Week: “The market is learning that resilience in the economy doesn’t guarantee calm in the markets.”

The Scoop

Quick Disclaimer: Today’s newsletter explores the concept of leveraged investing. This strategy involves significant risk and is not suitable for everyone. The goal is to illustrate an alternative approach that may work in specific situations for certain individuals. Many of the ideas and thoughts expressed in this newsletter are designed to illustrate that there are other ways of creating and protecting wealth.As always, speak with your advisor before considering any strategy like this.

On to the newsletter…

We’ve all heard the saying: “Renting is just throwing money away.” But is that still true?

A recent National Post article (here) highlighted something worth paying attention to: in many Canadian cities, the math no longer clearly favours homeownership. In Mississauga, a two-bedroom rental saves you about $13,000 over 10 years; in Abbotsford, the savings top $118,000.

The takeaway? Renting might not be “throwing money away” after all—especially if you invest the difference. And that got me thinking…

If buying a home is really a leveraged investment—you put down 20% but earn gains on 100%—what happens if you applied that same strategy to investing instead?

Let’s walk through it.

Scenario A: The Traditional Homeowner

You buy a home for $750,000. You put down $150,000, plus $20,000 in closing costs—so $170,000 total upfront.

Your monthly costs (mortgage, taxes, insurance, maintenance) come to around $4,400. Over 10 years, your home appreciates 3% annually, and you pay down some of the mortgage.

After a decade, you’ve likely built up around $550,000 in equity (between home price growth and mortgage principal payments).

Solid, steady, and relatively low risk.

Scenario B: The Renter-Investor (With Leverage)

Instead of buying, you rent a similar home for $3,000/month and hold onto your $170,000.

But here’s the twist:

You borrow $300,000 through a structured investment loan and invest the full $470,000 (your equity + borrowed funds) into an S&P 500 ETF. Historically, the S&P 500 has returned around 13.6% annually over the past 10 years, but to stay conservative, let’s assume 8% annual returns.

Rather than investing extra money, you use the $1,400/month cash flow savings (renting vs owning) to pay down the investment loan over time.

What happens?

After 10 years:

- Your investment portfolio grows to ≈ $1,014,695

- You’ve paid off the $300,000 loan (including ~$99,674 in interest)

- Your net portfolio value is also ≈ $1,014,695

That’s a meaningful gap—nearly double the homeowner’s equity.

What If You Didn’t Use Leverage?

Let’s say leverage makes you uneasy. What if you just invested the $170,000 (instead of buying a house) and also invested the $1,400/month saved by renting?

With the same 8% return assumption:

- Your portfolio could grow to ~$535,000 after 10 years.

That puts you within reach of the homeowner’s $550,000 equity, without the risks of borrowing or owning a single large asset like a house.

It’s not a flashy return—but it’s flexible, liquid, and diversified.

A Few Important Caveats

This isn’t financial advice, and it’s definitely not a recommendation to use leverage lightly.

Leveraged investing comes with real risks:

- If the market drops early, you still owe the loan

- If your investment underperforms, debt magnifies your losses

- There’s emotional discipline required—especially during market turbulence

The same is true on the homeownership side:

- If home values fall or stagnate, you could lose equity

- Big repairs, rising property taxes, or forced moves can eat away at returns

- Real estate is not liquid—you can’t sell a wall to cover an unexpected expense

The Takeaway

Owning a home is still a great way to build wealth—but it’s not the only way.

Homeownership is a leveraged investment. And under the right conditions, renting + investing—either with or without leverage—can go toe-to-toe with buying, especially if you’re disciplined and take a long-term approach.

The key is knowing which path fits your lifestyle, risk tolerance, and long-term goals. And that’s where we come in.

Let’s run the numbers together—and help you choose the path that gets you where you want to go.

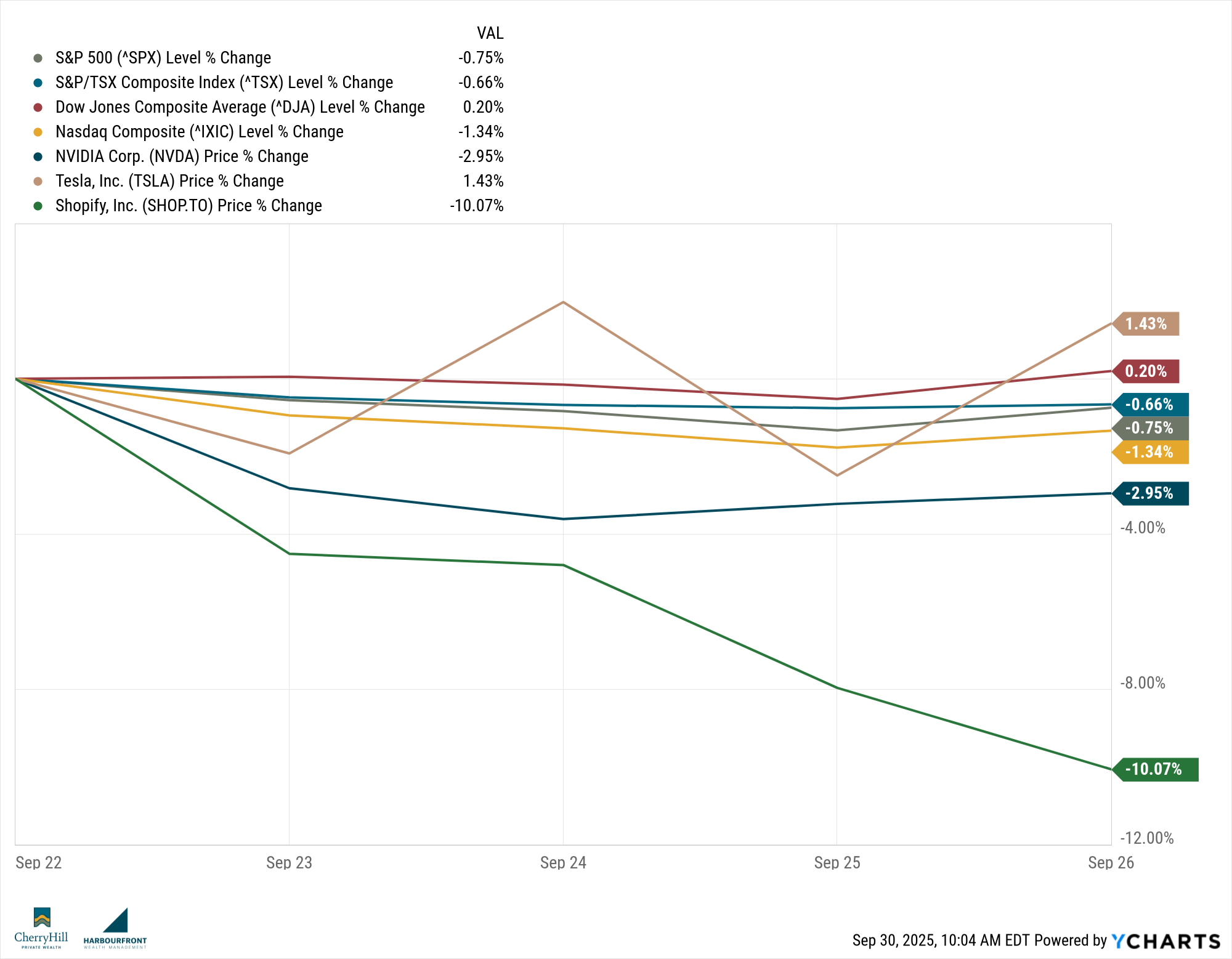

Market Minute

Markets were mixed this past week as investors balanced strong economic data against rising concerns over a potential U.S. government shutdown. While corporate and consumer fundamentals remain solid, headlines out of Washington and persistent inflation uncertainty kept investor sentiment in check.

Canadian Markets:

The TSX edged slightly higher (+0.3%) on the week, buoyed by strength in energy and materials. Energy stocks benefited from a rebound in oil prices, while base metal producers gained on improving global demand signals.

Economic data continues to show stability: GDP expectations were revised slightly upward, and August’s jobs data hinted at resilience in full-time employment. Financials were flat as bond market volatility left rate-sensitive names in a holding pattern.

U.S. Markets:

U.S. equity markets finished the week relatively flat, with investors balancing solid economic data against the uncertainty of a looming government shutdown. The S&P 500 slipped by 0.2%, the Dow dipped 0.3%, while the Nasdaq managed a slight gain of 0.1%, supported once again by strength in the tech sector. The August PCE inflation report came in as expected at 2.7% year-over-year, helping calm concerns about persistent inflation and giving markets some breathing room. Meanwhile, investor flows told a more optimistic story—U.S. equity funds saw roughly $12 billion in inflows during the week, driven largely by enthusiasm for AI and large-cap growth. That said, sentiment remained cautious as markets braced for potential disruption in data releases and policy direction should lawmakers fail to avert a shutdown before the October 1 deadline.

Global Markets:

European markets were relatively flat, with the DAX and FTSE 100 both inching higher on economic resilience.

In Asia, Japan’s Nikkei posted a minor loss (-0.4%) as the yen weakened and investors weighed the timing of further stimulus from the Bank of Japan.

Oil prices surged nearly $3/barrel during the week, closing just above $65 (WTI), amid ongoing supply concerns and Middle East tensions—supporting global energy shares.

Sector Spotlight:

Technology continued to lead market momentum. AI-related names attracted fresh capital as investors remain focused on long-term innovation trends. Software, semiconductors, and cloud infrastructure names performed well, with NVIDIA and Microsoft both up modestly on the week.

In Canada, Shopify added 2.3%, as investor sentiment around growth stocks remains cautiously optimistic.

Quote of the Week:

“Markets are beginning to shift focus from recession risks to policy uncertainty—proof that good economic news isn’t always market-friendly.”

— Mona Mahajan, Edward Jones Weekly Market Wrap

Trends to Watch This Week:

Here’s what were watching this week:

- U.S. Government Shutdown Risk: Congress faces a September 30 deadline to avoid a funding lapse. Delays could affect economic data flow, including jobs and inflation reports.

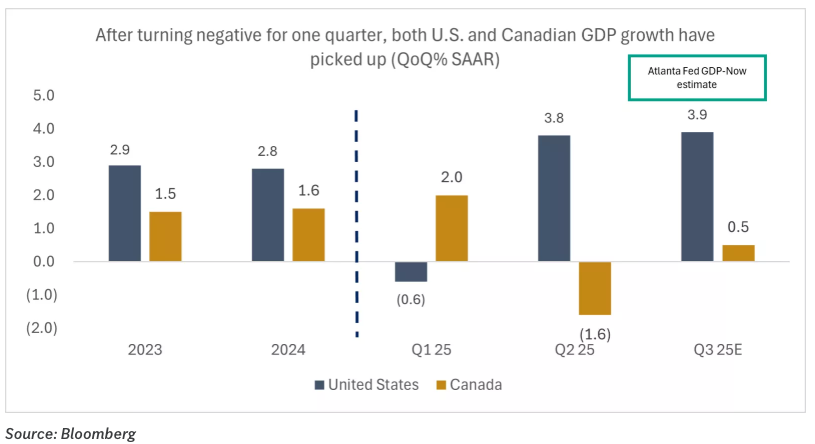

- Canadian GDP Print: Scheduled for release this week, investors will watch closely for signs of economic softening or resilience.

- Equity Fund Flows: Continued inflows into growth and AI-focused funds could keep lifting tech valuations.

- Oil Price Volatility: Supply disruptions may add to inflation uncertainty, especially if prices remain above $65–70.

- Central Bank Commentary: The market will parse speeches from both the Fed and Bank of Canada for clues on future rate moves.

Summary:

Despite economic strength, markets remain cautious. Positive data is now being weighed against potential policy disruptions—particularly in the U.S.—and the implications for rates and liquidity. Investors appear to be reallocating toward growth and tech themes while keeping a close eye on geopolitical risks and fiscal headlines.

With so much in motion, staying diversified and disciplined remains key.

Final Thought

At CHPW, helping you build and protect your wealth isn’t just what we do—it’s what we’re built for. Whether it’s constructing a more resilient portfolio by incorporating alternative asset classes, or exploring advanced strategies like tax planning, legacy building, or (as in today’s case) responsible use of leverage, our goal is to give you every advantage on the path to financial freedom.

We know that real wealth planning goes beyond the basics. That’s why our team includes Certified Financial Planners and specialists who collaborate to uncover opportunities others often miss. We’re committed to looking at the full picture—and never settling for cookie-cutter advice.

We’re still growing our practice and always happy to meet people who need a team that thinks differently, plans deeply, and brings the right tools to the table. If someone you care about could use that kind of support, we’d love an introduction.

Until next time, stay informed and strategically invested!

Trevor