The 60/40 Portfolio is Dying:

And That’s a Good Thing

In today’s email:

- BlackRock says the 60/40 portfolio is dead — here’s why that’s nothing new to us.

- What other big firms are doing to catch up with modern portfolio design.

- Markets rose modestly after surprise rate cuts in both the U.S. and Canada.

- Energy stocks take the lead as oil hits new 2025 highs.

- Quote of the Week: David Kelly on timing the next rate cut.

The Scoop

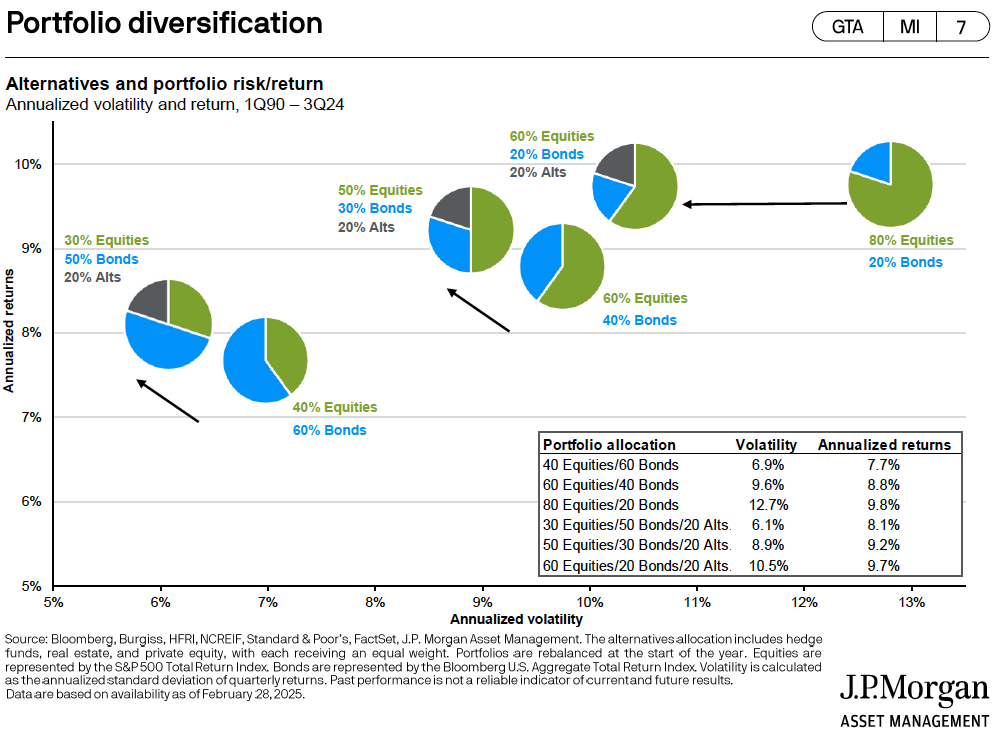

For decades, the 60/40 portfolio — that classic mix of 60% stocks and 40% bonds — was the industry’s go-to playbook. It was simple, easy to communicate, and for a long time, it worked. But markets have changed. The world has changed. And now even some of the biggest players on Wall Street are starting to say what we’ve known for years: the traditional 60/40 model no longer cuts it.

Larry Fink, CEO of BlackRock, made headlines this week when he told CNBC, “I don’t think 60/40 works.” He went on to highlight the growing need for alternative assets, citing their rising importance in building more resilient portfolios.

“Clients are looking for more and more alternatives.”

— Larry Fink, BlackRock

What’s interesting here isn’t the statement itself — it’s who’s saying it. BlackRock is the largest asset manager in the world. If they’re publicly walking away from 60/40, that’s a big deal. But more importantly, it’s confirmation that the approach we’ve taken for years is the right one.

The Industry is Catching Up

BlackRock isn’t alone. JPMorgan Asset Management recently published research questioning the long-term effectiveness of traditional portfolios in a high-volatility, lower-return world. Vanguard — historically a defender of low-cost, balanced portfolios — has also acknowledged that investors need to “prepare for lower returns” and may need to diversify more creatively.

Meanwhile, private equity, private credit, infrastructure, and other alternatives have been increasingly adopted by institutional investors, endowments, and pension funds.

“The 60/40 portfolio may be facing its toughest challenge in decades.”

— Goldman Sachs Asset Management

Sound familiar?

For years now, we’ve been building portfolios that go beyond the textbook 60/40 split. Our approach borrows heavily from how large endowments and pension funds invest — emphasizing alternative assets, downside protection, and lower volatility.

Why This Matters for You

Here’s the truth: markets have become more complex. We’ve seen periods where both stocks and bonds fall at the same time — something the 60/40 model simply wasn’t built to handle. Inflation, rising interest rates, and geopolitical uncertainty have exposed the vulnerabilities in that old framework.

So while others are just now pivoting, we’ve long believed in building smarter portfolios using tools like:

- Private credit and private real estate for steady, income-generating assets

- Infrastructure and private equity for long-term growth with different risk/return profiles

- Hedged equity to smooth the ride during turbulent markets

- Risk-managed strategies that aim to protect capital, not just chase returns

The goal isn’t to be flashy — it’s to be smart. To build something that lasts.

The Takeaway

If you’re working with us already, you know this is nothing new. We’ve been intentional about building portfolios that are forward-looking, not backward-glancing. The fact that big firms are finally coming around to this mindset? That’s just more validation that we’re on the right path.

Most investors out there — especially those not working with a firm like ours — simply don’t have access to this kind of investing. Their portfolios are still stuck in the old 60/40 model, and they don’t even realize there’s a better way.

If you know someone who could benefit from a more modern, institutional-style investment approach — someone who’s frustrated with traditional strategies or unsure about what’s next — let’s connect. Introductions are always appreciated, and we’re happy to start with a simple conversation to see if we can help.

Market Minute

Markets were relatively flat this past week as investors digested mixed inflation data and awaited more clarity from central banks. The narrative continues to revolve around interest rate trajectories, with core inflation slowing but still hovering above central bank targets.

Canadian Markets:

The TSX finished the week modestly higher (+0.3%), supported by strength in energy and materials as oil prices climbed. Financials remained range-bound as investors weighed the timing and depth of future rate cuts. Brookfield (+2.2%) was among the notable gainers, lifted by optimism in infrastructure investment.

U.S. Markets:

U.S. equities posted small weekly gains, with the S&P 500 up +0.2% and the Nasdaq slightly higher at +0.3%. The Dow ended the week flat. Markets reacted cautiously to the latest U.S. CPI report, which showed headline inflation ticking higher due to rising energy costs, while core inflation continued its downward trend. Tech remained a relative out-performer, with Adobe (+4.8%) jumping after strong earnings and forward guidance tied to AI-related demand.

Global Markets:

International markets were mixed. The MSCI EAFE index ended the week up (+0.6%) as investors responded positively to data suggesting moderating inflation in Europe. The ECB held rates steady, citing improving inflation expectations. Asian markets remained subdued, with ongoing weakness in Chinese economic indicators weighing on sentiment.

Sector Spotlight:

Energy stood out last week, with WTI crude climbing above $91 per barrel — its highest level since mid-2022. This supported gains in both Canadian and U.S. energy stocks, and renewed conversations around energy security and global supply constraints.

Quote of the Week:

“It’s not about timing the next rate cut. It’s about building portfolios that can thrive regardless of the outcome.”

— David Kelly, J.P. Morgan Weekly Market Recap

Trends to Watch This Week:

Here’s what were watching this week:

- U.S. Fed Meeting: All eyes are on the upcoming FOMC decision and commentary. Markets expect a pause, but guidance will be key for future rate expectations.

- Canadian CPI Release: Inflation data in Canada will help shape the Bank of Canada’s tone heading into October.

- Global Manufacturing Data: Updates from Europe and China may offer insight into global growth trends and commodity demand.

Summary:

Markets are searching for direction as inflation trends slow but remain sticky. Central banks appear to be at or near the end of their rate-hiking cycles, and investor focus is now shifting toward the timing of future cuts. In the meantime, sector leadership is rotating, with energy and infrastructure gaining momentum in a more uncertain macro backdrop.

Final Thought

Everyone on the Cherry Hill team took a massive leap of faith when we left the institutions we’d been with for years. We believed in a better process — one that gave clients access to the kinds of portfolios typically reserved for endowments, pension funds, and the Ultra Wealthy. You took that leap with us, and we’re incredibly grateful.

Being a trendsetter is never easy. But as we watch major U.S. firms pivot away from traditional 60/40 portfolios and finally acknowledge the limitations of that outdated model, we feel a strong sense of validation (Canada, as usual, is still playing catch-up).

You’ve had a front-row seat to how private asset investing can reshape what a portfolio can do. Thank you for trusting us to guide you through this more modern — and frankly, smarter — way to invest. You can proudly tell your friends and family that you were among the first in Canada to embrace private asset funds for your portfolio. And if someone you care about is still stuck in the past, we’d be happy to have a conversation.

Until next time, stay informed and strategically invested!

Trevor