The Real Story Behind Rising Gas Prices

In today’s email:

- Gas prices are climbing — but it’s not just oil that’s to blame.

- The TSX took the lead last week — can energy keep driving it higher?

- U.S. markets are leaning on tech again while consumers tighten their belts.

- Europe and Japan are stealing the spotlight with standout returns.

- Inflation and housing data this week could shake up the rate outlook.

The Scoop

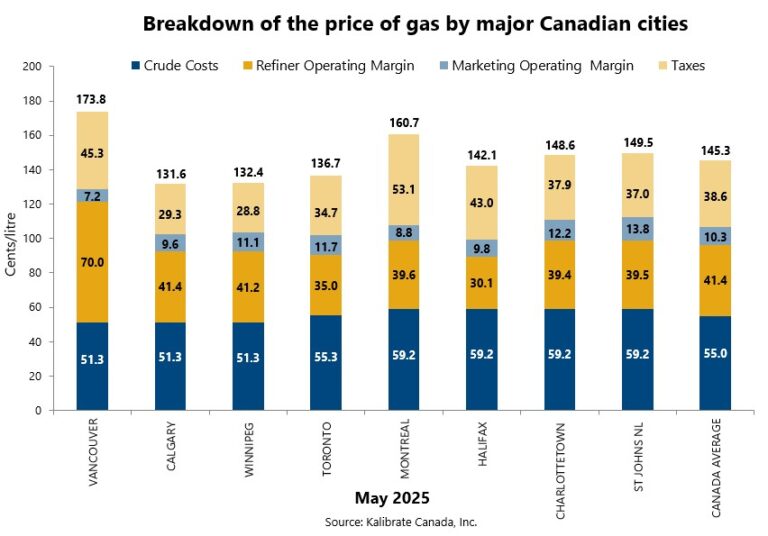

Pull up to the pump and see prices suddenly 10¢ higher, and the first thought is usually: “Oil must be up.” It makes sense—crude oil is the raw material for gasoline. But the truth is, what you’re paying for at the pump is only partly tied to the price of a barrel. Crude makes up roughly half the cost. The rest comes from refining, transportation, distribution, and retail markups. Then taxes pile on top—federal excise taxes, provincial fuel levies, carbon taxes, and even GST/HST.

That means a big chunk of what you see on the sign outside the gas station has nothing to do with global oil prices. In fact, two drivers filling up on the same day—one in Alberta and one in Vancouver—can pay 30¢ per litre different purely because of taxes and local supply chains.

Why the Recent Jump Happened

So why did prices jump this time? It’s a perfect storm of factors. Seasonal demand is one—summer road trips and holiday weekends see fuel consumption spike. Refineries also use summer to perform maintenance, which cuts supply right when drivers are using more. Add to that regional quirks—BC often faces some of the highest prices in North America due to limited refining capacity and pipeline access.

For Ontario drivers, there’s an added wrinkle: most of the province relies on supply coming from U.S. Midwest refineries. Any hiccup—whether it’s maintenance, outages, or strong American demand—can spill over quickly into prices at the pumps.

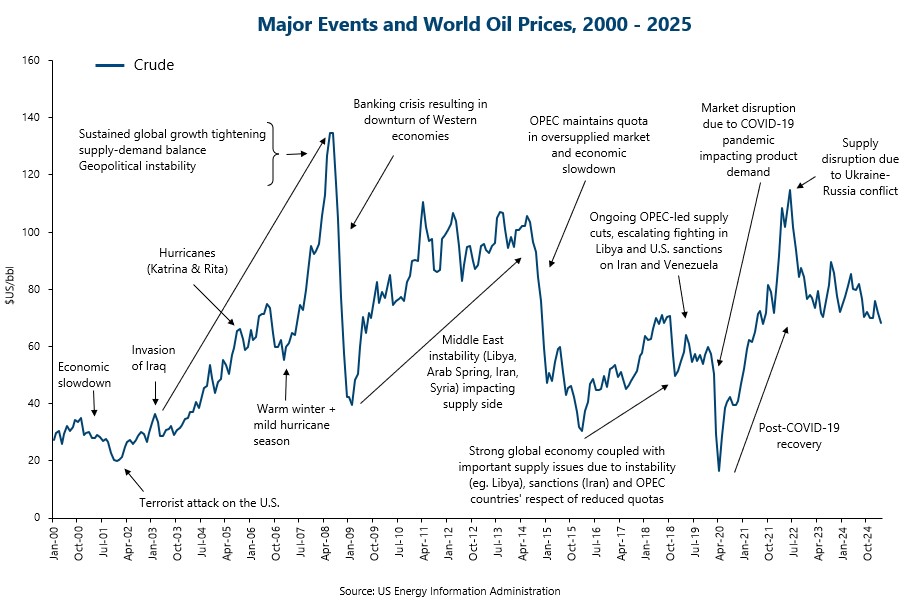

And here’s the kicker: oil is priced in U.S. dollars. When the Canadian dollar weakens against the greenback, it magnifies the cost of every barrel we import. Even if oil itself only nudges higher, a weaker loonie can make it feel like a big jump at the pump for Canadian drivers.

How Barrel Prices and Pump Prices Are Linked

There is a connection between oil and gasoline, but it’s not neat and tidy. Think of crude oil as the dough, and gasoline as the bread—it has to be processed before it’s ready. Crude typically makes up 50–60% of pump prices, so big moves in oil eventually filter down, but not always immediately or equally.

The wild card is what’s known as the “crack spread”—the profit margin refiners earn for turning oil into gasoline. If refineries are running at full tilt and margins are tight, prices at the pump might not move much even when oil rises. But when supply is constrained and demand is hot, those margins widen. That’s when you see gasoline jump faster than oil, and it feels like drivers are paying more than their fair share. And when oil prices fall? Well, retailers and refiners don’t always rush to pass those savings on—meaning pump prices can stay stubbornly high.

The Broader Economic Impact

Gasoline isn’t just another household expense—it’s a price we see flashing on every street corner. Unlike groceries or utilities, you can’t avoid noticing it. When drivers pull up and see $1.90 or $2.00 per litre on the sign, it doesn’t just strain the wallet—it sends a signal about the economy, often dampening consumer confidence. High gas prices act like a stealth tax, draining disposable income that could have gone to dinners out, new clothes, or family vacations.

For businesses, the pinch is just as real. Trucking companies, airlines, and shipping firms all see costs rise, and those costs often filter through to grocery store shelves and online orders. It’s one reason central banks watch fuel prices closely: sticky gasoline costs can make inflation harder to bring down, forcing them to hold interest rates higher for longer. In short, what you pay to fill your car can ripple all the way through to mortgage rates and stock markets.

What It Means for Investors

For investors, gasoline prices highlight the push and pull across sectors. Oil producers and refiners benefit when crude prices are strong and margins wide—something shareholders in energy companies have enjoyed recently. On the flip side, airlines, consumer discretionary businesses, and transportation companies feel the squeeze when fuel costs eat into profits.

This is also a good reminder that “macro” news has very real effects on portfolios. What we see at the pump isn’t just a household nuisance—it’s a signal of broader economic conditions. Rising pump prices can foreshadow inflation pressures, shifts in consumer spending, and eventually changes in central bank policy, all of which shape investment opportunities.

Market Minute

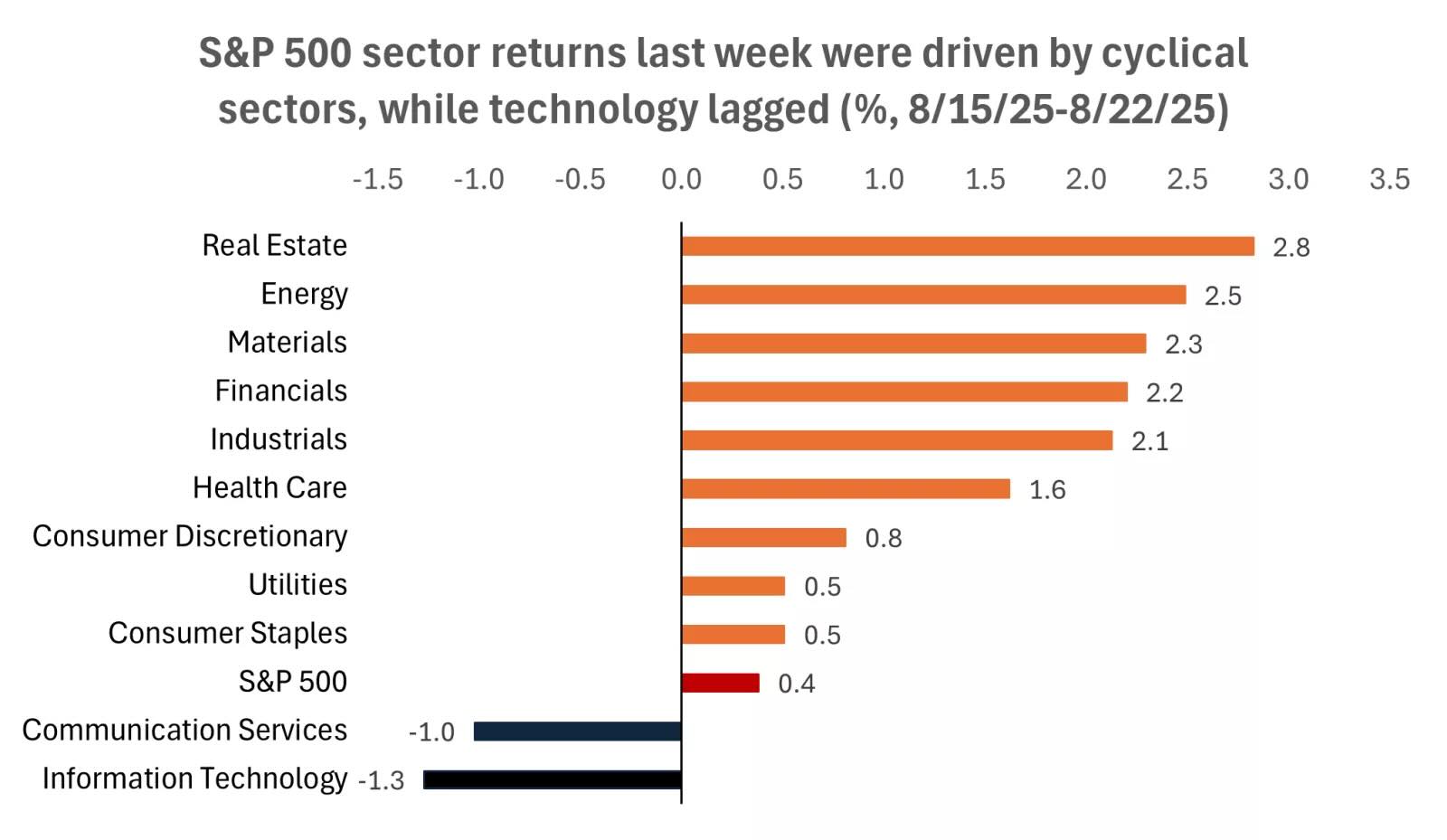

Markets ended last week on firmer footing, with investors continuing to balance optimism around corporate earnings and stable bond yields against lingering concerns about consumer demand and global growth. Canadian equities led the way thanks to energy strength, U.S. markets eked out modest gains, and international stocks remained the standout for 2025 with another strong weekly performance.

Canadian Markets:

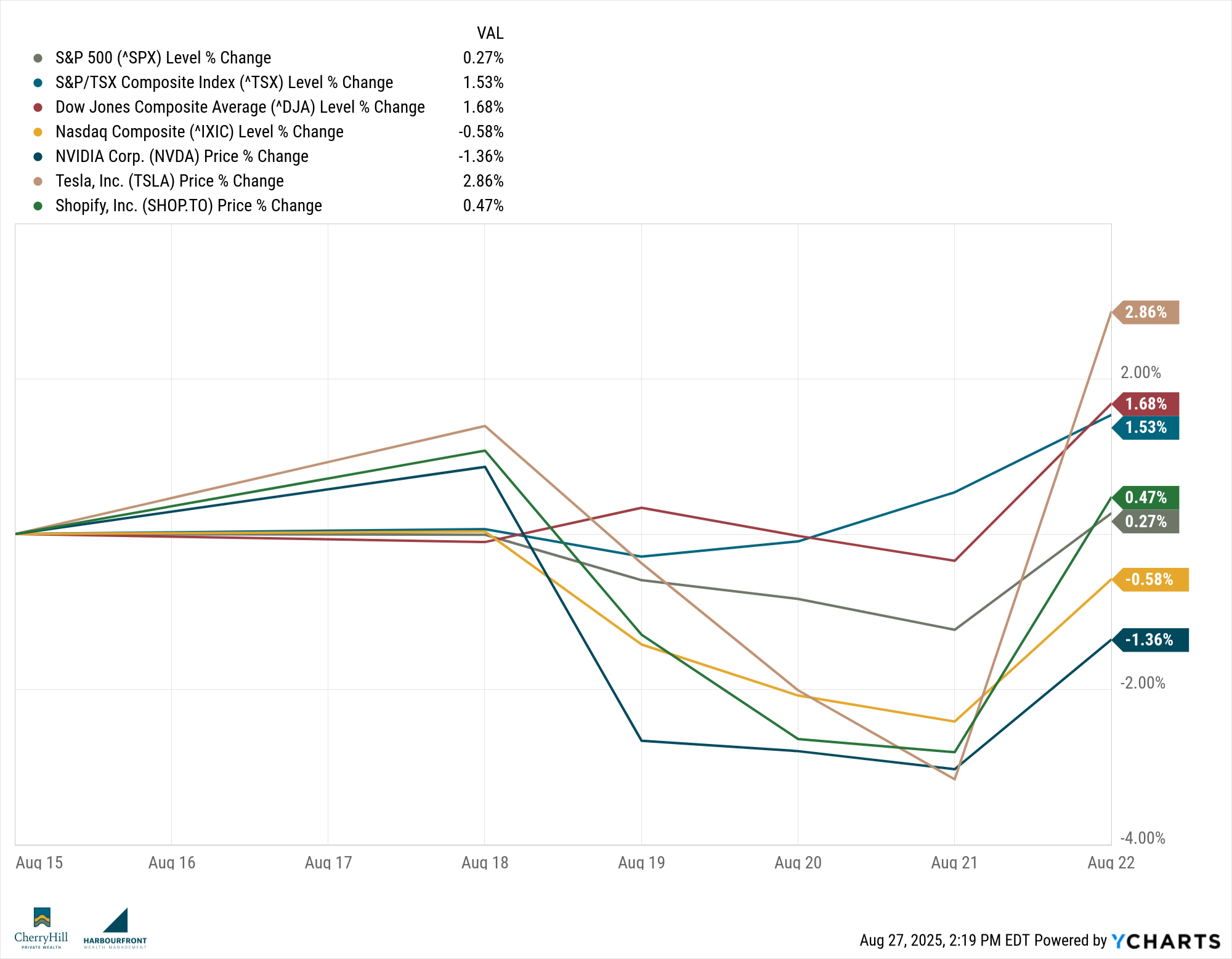

The TSX advanced 1.5% on the week, outperforming U.S. benchmarks as energy stocks benefitted from a rebound in oil. Crude rose 1.6% to $63.81 per barrel, reversing part of its year-to-date decline and helping lift Canadian producers. Financials were steady, reflecting stability in rates with the 10-year Government of Canada bond yield flat at 3.40%. The Canadian dollar slipped 0.2% against the U.S. dollar, ending at $0.72, which adds a headwind for import costs but provides some support for exporters. Year-to-date, the TSX is now up 14.6%, a strong showing relative to its U.S. counterpart.

U.S. Markets:

South of the border, the S&P 500 gained 0.3%, as strength in technology once again offset weakness in consumer-facing sectors. Investors leaned into large-cap names that continue to drive market performance, though concerns around consumer spending remain a drag on sentiment. Inflation continues to be the key watchpoint for the Federal Reserve, and with bond yields holding steady, the market is cautiously optimistic about rate stability. Year-to-date, the S&P 500 is up 10%, but leadership remains narrow, with tech carrying much of the load.

Global Markets:

International equities remain the global leaders this year, with the MSCI EAFE index up another 0.8% last week, and now an impressive 22.2% year-to-date. European markets saw renewed strength on the back of better-than-expected German industrial production data, while Japan benefitted from continued optimism that monetary policy will remain accommodative. The weaker yen has provided an additional tailwind to Japanese exporters. Global investors are increasingly looking outside of North America for diversification, and 2025 has so far rewarded that move.

Sector Spotlight:

Energy was the week’s bright spot, with oil prices ticking higher and boosting Canadian producers in particular. After months of pressure from oversupply concerns, the recent rebound suggests stabilizing demand. Refinery margins also improved, adding to sector strength. Investors will continue to watch for signals from OPEC+ on supply adjustments, as production policy has the potential to swing sentiment quickly in either direction.

Quote of the Week:

“Uncertainty is the new normal, but resilience is what carries economies through.”

— Christine Lagarde, ECB President

Trends to Watch This Week:

Here’s what were watching this week:

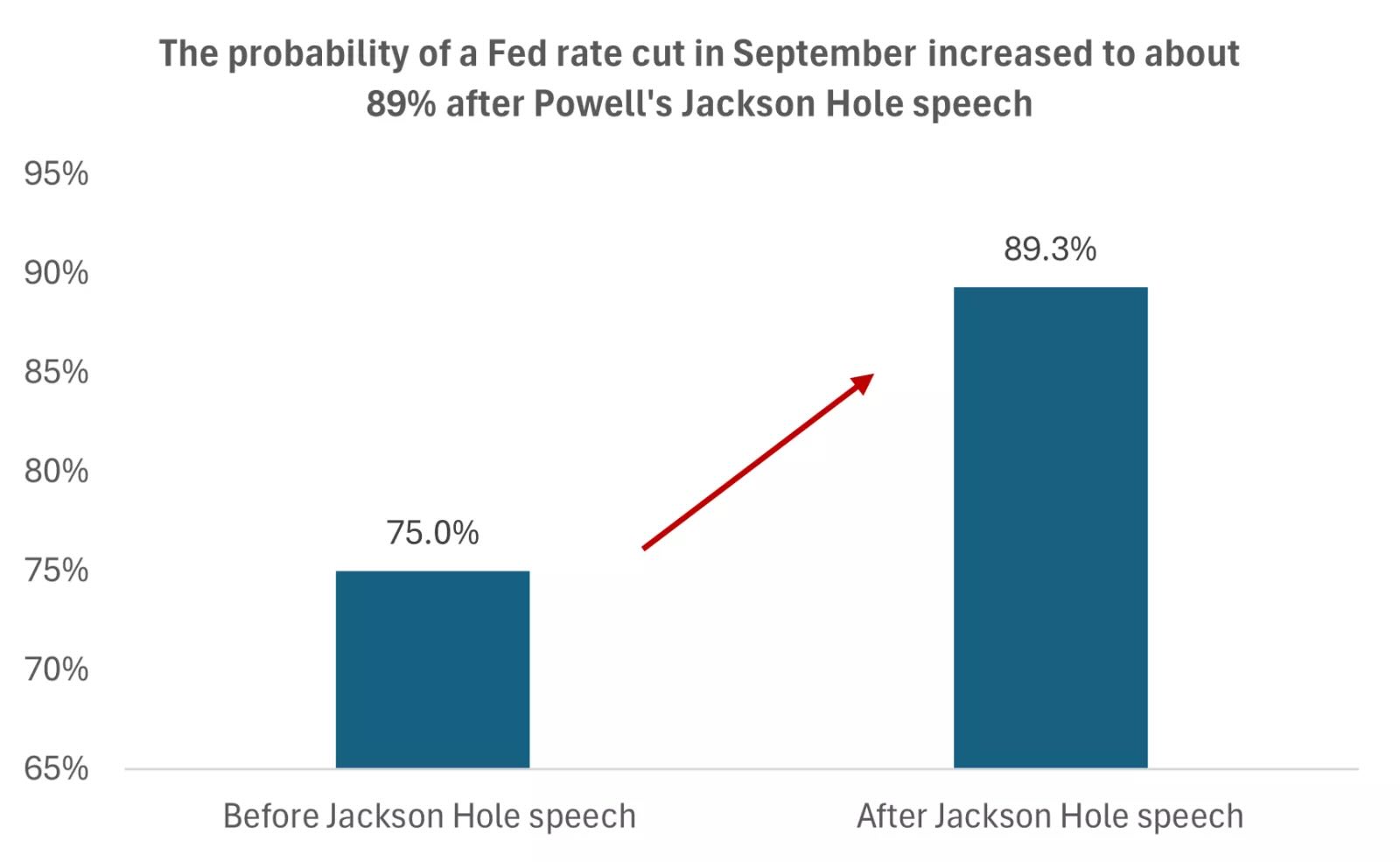

- U.S. Inflation Data: Investors will closely watch this week’s release for signals on the Federal Reserve’s next steps.

- Canadian Housing Data: Price trends and sales activity will shed light on consumer confidence and the impact of higher rates.

- Oil Market Developments: Any new commentary from OPEC+ could influence energy sector momentum.

Summary:

Markets closed last week on firmer footing, with Canadian equities leading the way and international stocks maintaining strong year-to-date performance. With inflation and housing data due this week, investors will be focused on whether the balance between economic resilience and inflationary pressures can sustain market momentum into the fall.

Final Thought

For most of us with young kids, this marks the final week of summer vacation. Fall is usually a great time for us to get together to do some financial planning and ensure that we are set up for a great year end and strong start to the new year and we’d be happy to book a time to work on planning with you.

That being said - this is the final long weekend of the summer, so get outside and do something that brings you joy! Our office is closed on Monday, so have a great long weekend!

Until next time, stay informed and strategically invested!

Trevor