Predictability Over Possibility:

The Power of Volatility Control

In today’s email:

- Does your average rate of return matter?

- If Sarah and David both get the same return and spend the same, why is David broke?

- Markets had a good week across the board, but there has been a shift.

- What will the Fed do next?

The Scoop

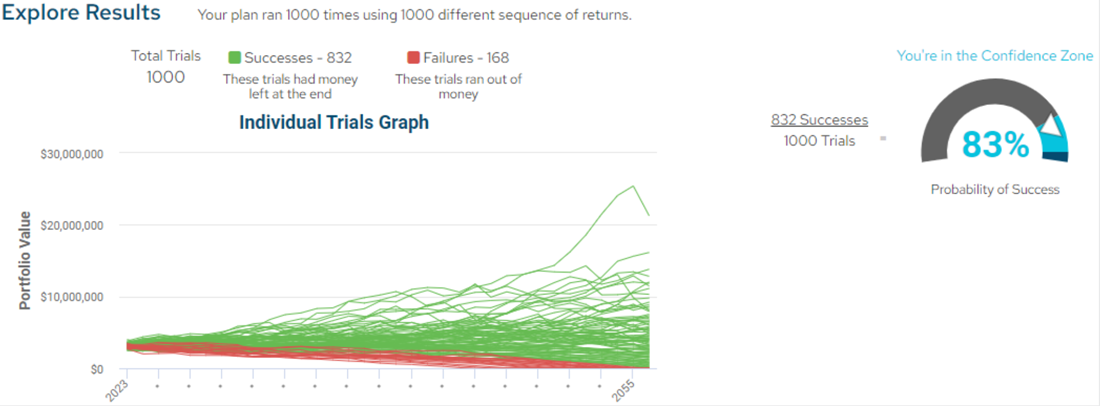

Most retirement plans don’t fail because people don’t earn enough—they fail because the returns come at the wrong time. At Cherry Hill, one of the most important tools we use to prevent that outcome is Monte Carlo analysis. It’s not about guessing the future—it’s about understanding how different sequences of returns and risk levels play out over time.

So what happens when we reduce the volatility in a plan—even just a little?

Let’s look at two simple, but very real, case studies. Ready to get a bit nerdy?

Case Study 1: Same Returns, Different Outcomes

Meet Sarah and David. Both retire with $1,000,000 and plan to withdraw $50,000 per year, adjusted for inflation. They both expect an average return of 6% per year over 30 years.

But here’s the catch:

- Sarah’s Portfolio: Her first year return is +10%, followed by a mixed but steady path that averages 6%.

- David’s Portfolio: His first year return is –10%, also followed by the same average 6%.

Result:

Sarah’s portfolio lasts comfortably into her 90s.

David’s runs out by age 82.

This is the sequence of returns risk in action. Even though both averaged the same return, the early losses combined with withdrawals made David’s portfolio bleed faster.

Case Study 2: Smoother Ride, Better Outcome

Now let’s compare Emily and James. They also both retire with $1,000,000 and withdraw $50,000 per year. But:

- Emily’s Portfolio: Average return of 6%, with high volatility (standard deviation of 12%).

- James’s Portfolio: Same 6% average return, but with lower volatility (standard deviation of 6%).

Result (based on Monte Carlo simulation):

Emily has about a 65% chance of making it through retirement without running out of money.

James? He’s sitting at 90%+.

Same average returns, dramatically different confidence. That’s what managing volatility does.

Why We Build Like a Pension (And You Should Too)

At Cherry Hill, we don’t invest like a traditional retail advisor. We invest like a pension fund—and there’s a good reason for that.

Pensions, endowments, and the largest family offices in the world all share one thing in common: they care deeply about downside protection.

Why?

Because it’s not about hitting home runs—it’s about not striking out.

These institutional investors know that avoiding big losses is the key to long-term success, especially when they have ongoing liabilities (like paying retirees… or funding your retirement lifestyle).

That’s why our portfolios are built with alternative investments that reduce volatility, such as:

- Private credit and private real estate

- Infrastructure assets

- Hedged equity strategies

- Structured notes and downside buffers

These aren’t always available at the bank or through mutual funds, but they are available to you through our platform. The result? A more predictable retirement income, with a higher chance of success—even if markets stay rocky.

Predictability Is the New Growth

Chasing returns is exciting in your 30s and 40s. But in retirement, predictability is what really matters. Monte Carlo analysis shows us clearly: reducing volatility can be even more powerful than increasing return.

If you want to see what this could look like for your own plan—or stress test your current setup—let’s talk. We can show you exactly how a smoother ride can lead to a stronger retirement.

Market Minute

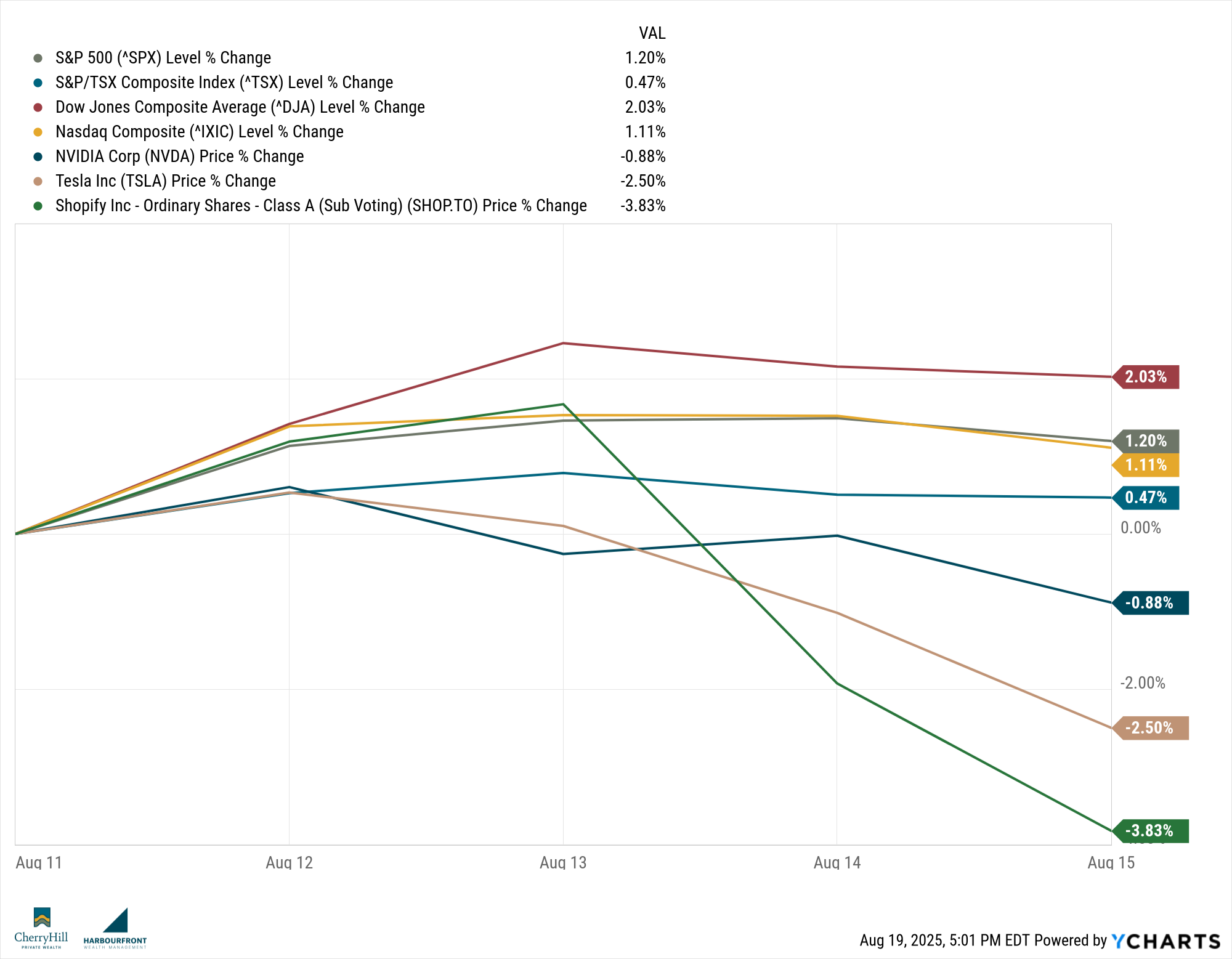

This past week, markets posted broad gains across North America and overseas, as investors welcomed signs of economic stability and growing expectations for interest rate cuts. Momentum returned to small- and mid-cap names, signaling expanding breadth in the equity rally, while Canadian equities continued to show resilience amid improving sentiment around trade and monetary policy.

Canadian Markets:

The TSX Composite Index advanced by approximately 0.5% for the week, marking another step forward in a generally positive third quarter. Strength in financials and industrials helped offset weakness in energy, while Canadian investors tracked global sentiment closely ahead of upcoming inflation readings. A recent Reuters poll suggests the TSX could rise another 2.3% before year-end, supported by easing rate pressures and greater trade certainty. While the Trump–Putin meeting dominated political headlines, markets remained largely unaffected, instead focusing on domestic data and upcoming Bank of Canada commentary.

U.S. Markets:

All three major U.S. indices ended the week in positive territory. The Dow Jones Industrial Average gained 2.03%, supported by strong performance in healthcare, especially UnitedHealth, which surged following news of a large Berkshire Hathaway stake. The S&P 500 climbed 1.2%, while the Nasdaq Composite added 1.1%, despite some softness in the semiconductor space. Notably, the rally extended beyond the usual tech leaders, as small-cap and value stocks outperformed—offering investors a sign that the recovery is broadening. The Russell 2000 index rose over 3% for the week, suggesting improving economic confidence at the grassroots level. A stable inflation environment and hopes for a September rate cut by the Federal Reserve helped keep investor sentiment upbeat throughout the week.

Global Markets:

International stocks joined in the rally, with the MSCI EAFE Index rising 2.4%. European shares responded positively to encouraging economic data out of Germany and easing political tension across the eurozone. In Asia, markets remained steady despite ongoing concerns around China’s property sector. Japanese equities edged higher, aided by the Bank of Japan’s reaffirmed stance to maintain accommodative policy. The combination of global central bank dovishness and a lack of major geopolitical flare-ups contributed to the optimistic tone across global indices.

Sector Spotlight:

Small-cap and value stocks stole the spotlight this week, outperforming their large-cap and growth counterparts by a notable margin. Investors appear to be repositioning portfolios to take advantage of more economically sensitive areas of the market. This shift comes amid growing belief that the U.S. economy may achieve a soft landing, allowing sectors that had lagged during the mega-cap tech run-up to finally catch a bid. The Russell 2000’s 3.1% gain is a strong indication of this rotation. Leadership in sectors like industrials, financials, and select consumer names reinforced this broadening of the bull market.

Quote of the Week:

“Tactical pullbacks should be viewed as opportunities to add exposure, as the bull market appears well supported by underlying fundamentals.

— Angelo Kourkafas, Senior Global Investment Strategist, Edward Jones

Trends to Watch This Week:

Here’s what were watching this week:

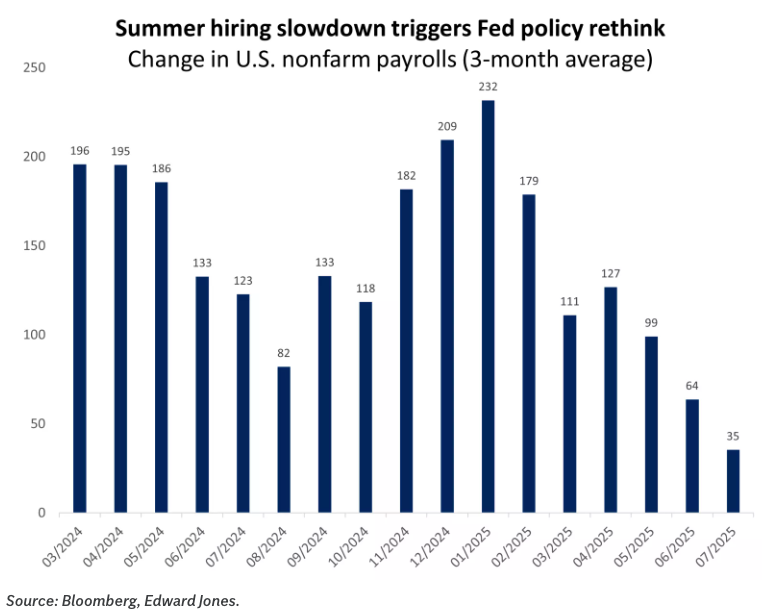

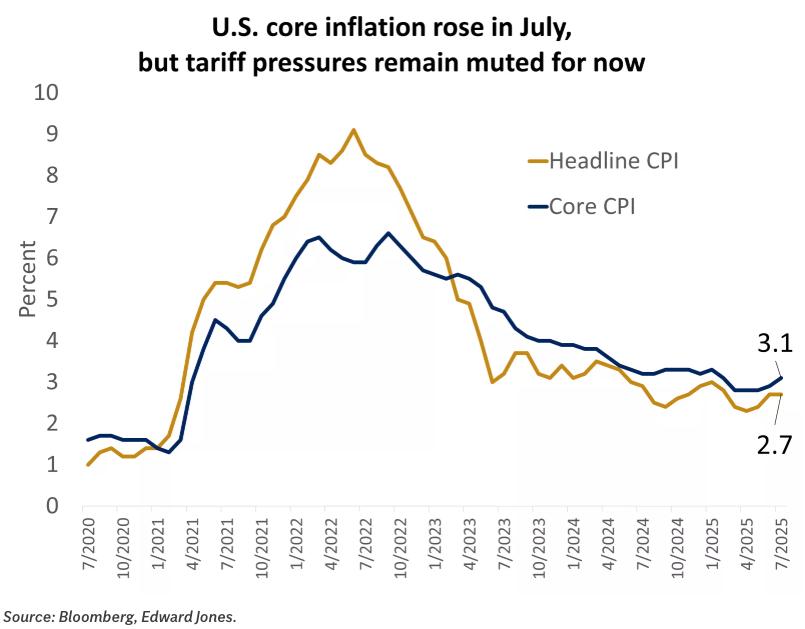

- U.S. inflation and retail sales data could influence the Fed’s next move.

- Jackson Hole Economic Symposium begins Thursday, with markets watching for clues on interest rates.

- Canadian manufacturing and wholesale trade numbers are due, helping shape expectations for the next Bank of Canada meeting.

Summary:

Equities gained ground globally last week, led by U.S. small caps and a rebound in international markets. Lower volatility, steady inflation, and the growing likelihood of a Fed rate cut contributed to improved investor sentiment. As markets digest this momentum, all eyes now turn to key inflation figures and the Federal Reserve’s message from Jackson Hole—two potential catalysts that could define the tone heading into September.

Final Thought

For those of you already working with us, you know that having a strong portfolio is just one part of a great financial strategy. True success comes from combining intentional investment approaches with the full range of available tools—and regularly stress-testing your plan. Monte Carlo analysis is just one of the many ways we help ensure that you and your family not only achieve financial freedom, but maintain it with confidence.

Until next time, stay informed and strategically invested!

Trevor