The Real Question:

How Much Income Do You Need?

In today’s email:

- Is $1.3 million what you should target for retirement?

- How should you set a target for your retirement?

- Not all income is taxed equally.

- Unemployment data, tariffs, and an unhappy market.

The Scoop

You’ve probably seen the headlines: “You need $1.3 million to retire.” It’s a nice, round number—and it feels like a good goal to chase. But here’s the problem: focusing solely on a big retirement number is like planning a road trip by picking a distance without ever checking the map.

At Cherry Hill, we flip that thinking around.

We don’t start with a savings target—we start with a lifestyle target.

How Much Income Do You Actually Need?

Instead of aiming for a magic lump sum, we work with clients to figure out how much income they’ll need each year to support the life they want:

- What are your monthly living costs?

- Will you travel? Maintain a cottage? Support kids or grandkids?

- What happens if your health changes? Or if you want to retire earlier than expected?

That income number becomes the real foundation of your retirement plan—not the size of your portfolio.

And once we’ve landed on that lifestyle-driven income goal, then we reverse-engineer the savings, investment mix, and drawdown strategy to support it.

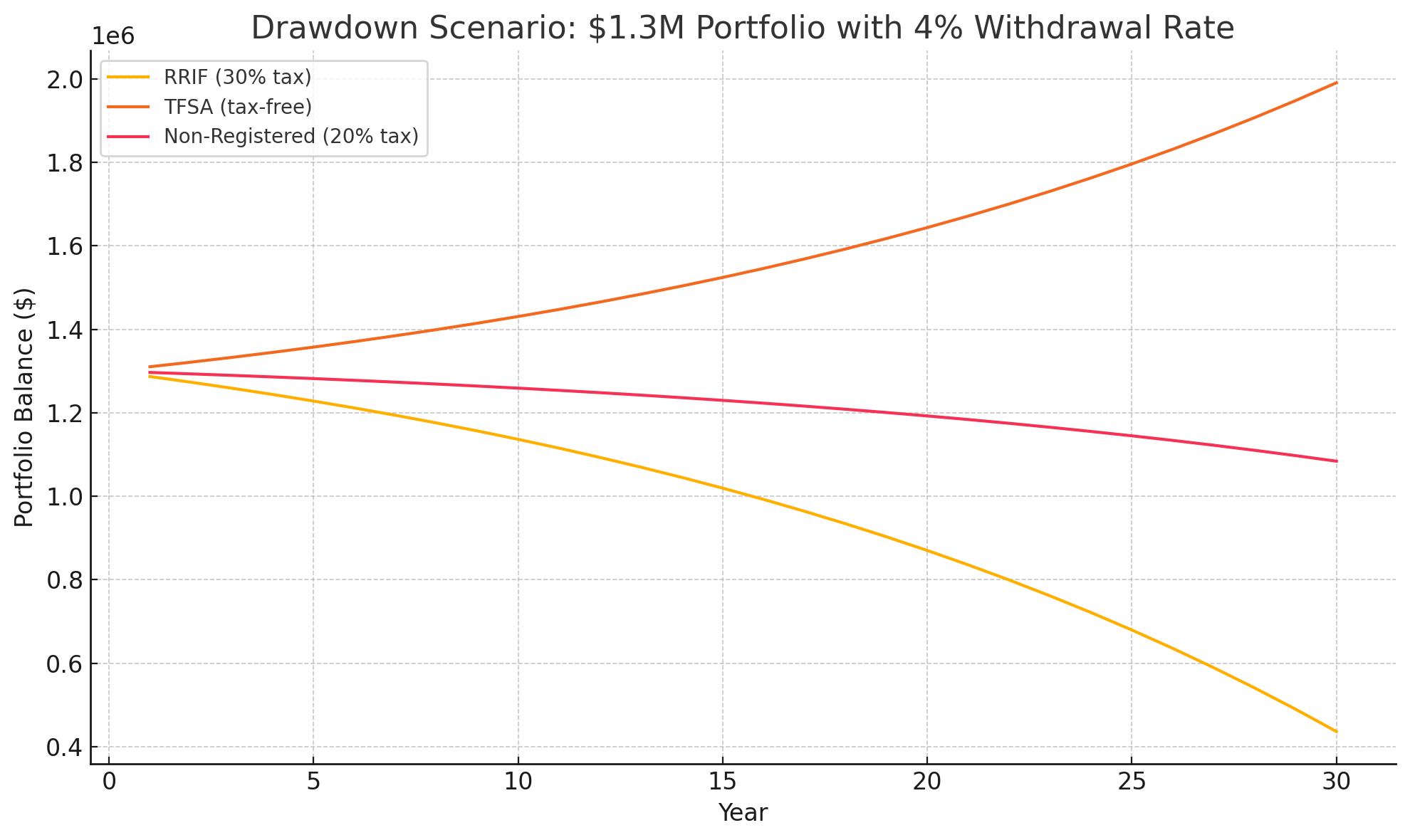

What Does $1.3 Million Really Get You?

If you were to follow the traditional 4% rule on a $1.3 million nest egg, you’d generate roughly $52,000 per year before taxes. That might sound reasonable, but taxes and inflation quickly shrink that number.

More importantly: where your income comes from matters just as much as how much you have.

Here’s why:

- RRSPs/RRIFs: Fully taxable. Every withdrawal is treated like salary.

- TFSAs: Withdrawals are completely tax-free—great for managing cash flow and avoiding OAS clawbacks.

- Non-registered accounts: Tax depends on the type of investment income.

- CPP/OAS/Pensions: Indexed and predictable, but taxable, and they may not fully cover your needs.

A well-balanced retirement income plan uses all of these tools together—efficiently and strategically.

Stress-Testing the Plan

A good plan isn’t just about averages—it’s about resilience. At Cherry Hill, we “crash test” retirement plans to ensure they can stand up to:

- A major market correction early in retirement

- A health event or long-term care need

- Inflation that stays higher than expected

- Unexpected expenses like home repairs or family support

These aren’t just hypotheticals—they’re real-life risks we plan for in advance.

The Bottom Line: Focus on Income, Not a Magic Number

Retirement isn’t about hitting $1 million, $1.3 million, or any other arbitrary goal. It’s about knowing what kind of life you want—and building a plan that gives you the confidence to live it.

If you’re wondering whether your current plan is on track—or how much income your savings could actually support—we’re here to help make sense of it.

Market Minute

Markets moved sharply lower this past week as investor sentiment turned more cautious. Concerns over slowing global growth, disappointing earnings in some sectors, and lingering uncertainty around the pace of rate cuts weighed on major indexes.

Canadian Markets:

The TSX dropped 1.7%, with losses across energy, materials, and financials. Commodity prices softened, dragging down resource-heavy names, while Canadian banks faced pressure amid narrowing margins and ongoing credit concerns. Defensive sectors offered little refuge as broad market sentiment declined.

U.S. Markets:

The S&P 500 saw its worst weekly performance in several months, falling 2.4%. Tech, which had been a key driver earlier in the year, took a breather, while consumer and healthcare sectors underperformed following weaker earnings. Mixed economic data and a slight uptick in unemployment claims added to investor jitters.

Global Markets:

The MSCI EAFE Index, which tracks developed markets outside North America, declined 3.1%. European markets retreated as manufacturing data disappointed, and Asian equities slumped amid ongoing concerns over China’s property sector and export demand. Global investor sentiment remained fragile as hopes for synchronized growth faded.

Sector Spotlight:

Technology stocks, which had been a source of strength for most of 2025, led the pullback this week as investors locked in gains. Energy and materials also struggled amid weaker commodity prices. Conversely, utilities and telecom fared slightly better, reflecting a minor rotation into defensive positions.

Quote of the Week:

“Markets can handle bad news or good news—but uncertainty is what really rattles investors.”

— Anonymous trader insight from the floor

Trends to Watch This Week:

Here’s what were watching this week:

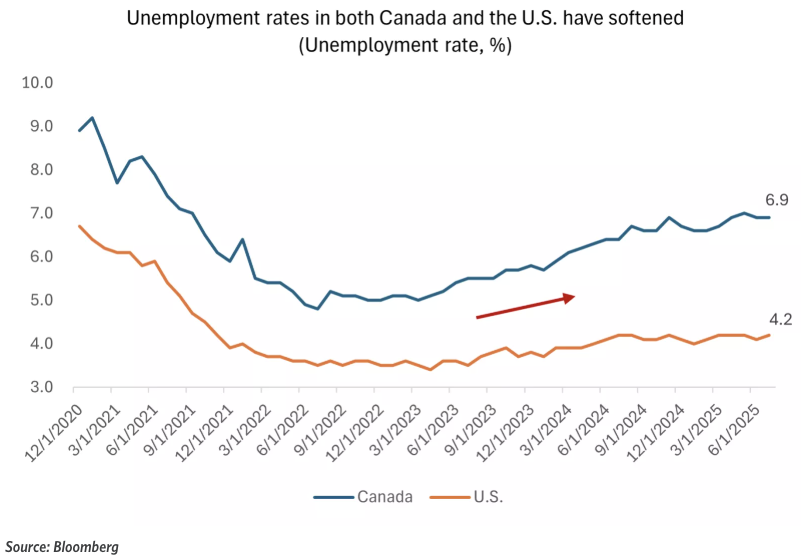

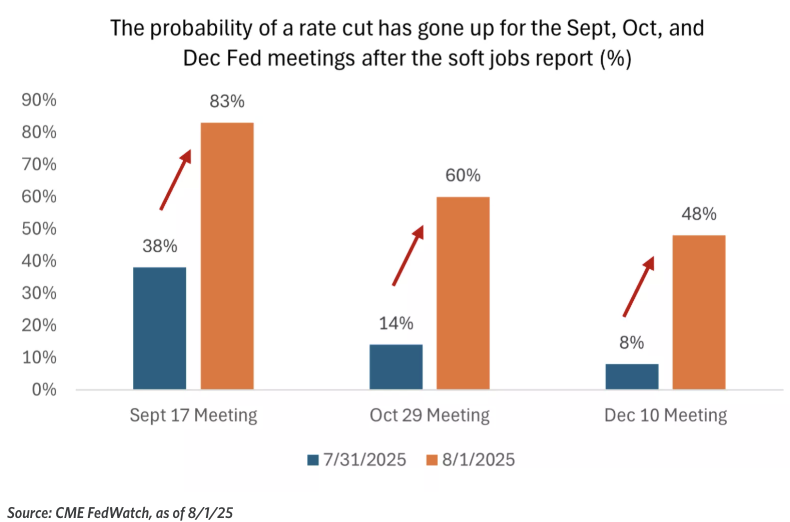

- U.S. Jobs Report Reaction: Investors will watch closely to see whether employment softness continues and how that might influence the Fed’s next move.

- Canadian Economic Data: CPI and housing data will help gauge how the Bank of Canada may proceed with rate adjustments.

- Earnings Season Wrap-Up: Final reports from smaller firms may reveal more about consumer trends and sector resilience heading into Q4.

Summary:

After months of relative strength, global equity markets saw a notable pullback as growth concerns and mixed data triggered a wave of risk-off sentiment. Investors are now looking ahead to inflation and employment figures for clarity on central bank policy and the broader economic path.

Final Thought

We continue to see volatility in the markets, but overall, it’s been a pretty good year for equities. Minimizing these downward swings, while continuing to take advantage of the climbs remains our primary focus. Building a plan for retirement that crash tests various scenarios can be the difference between living the retirement lifestyle that you’ve dreamt about vs. living tighter than you’d like.

Until next time, stay informed and strategically invested!

Trevor