Summer Slump or Seasonal Myth?

In today’s email:

- Sell in May and Go Away, right?

- The January Effect, the Halloween Indicator, and other market myths.

- Markets are hitting new highs, so why are we so worried?

- Inflation is under control… for now.

The Scoop

Every summer, someone inevitably brings up the old investing adage: “Sell in May and go away.” It’s catchy, easy to remember, and it’s been repeated for decades. But like many things in investing, simple doesn’t always mean smart.

So, is the so-called “summer slump” something investors should worry about—or is it just another seasonal myth that’s overstayed its welcome?

Let’s dig in.

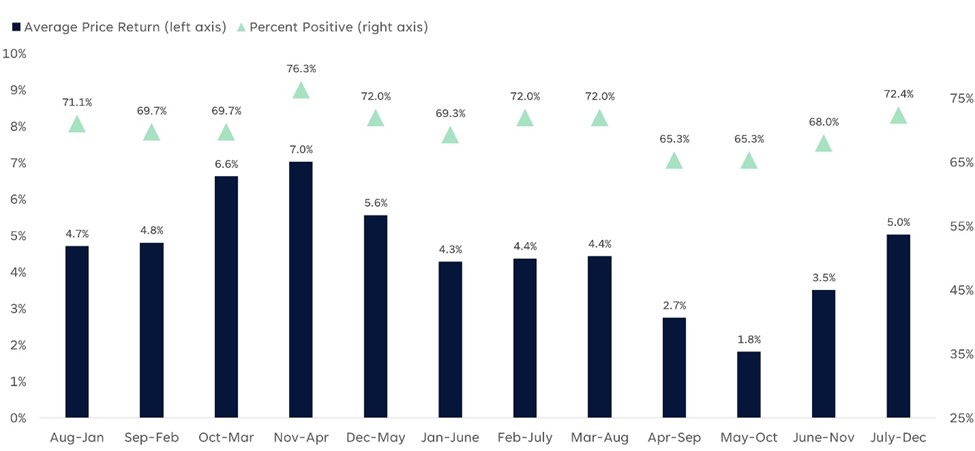

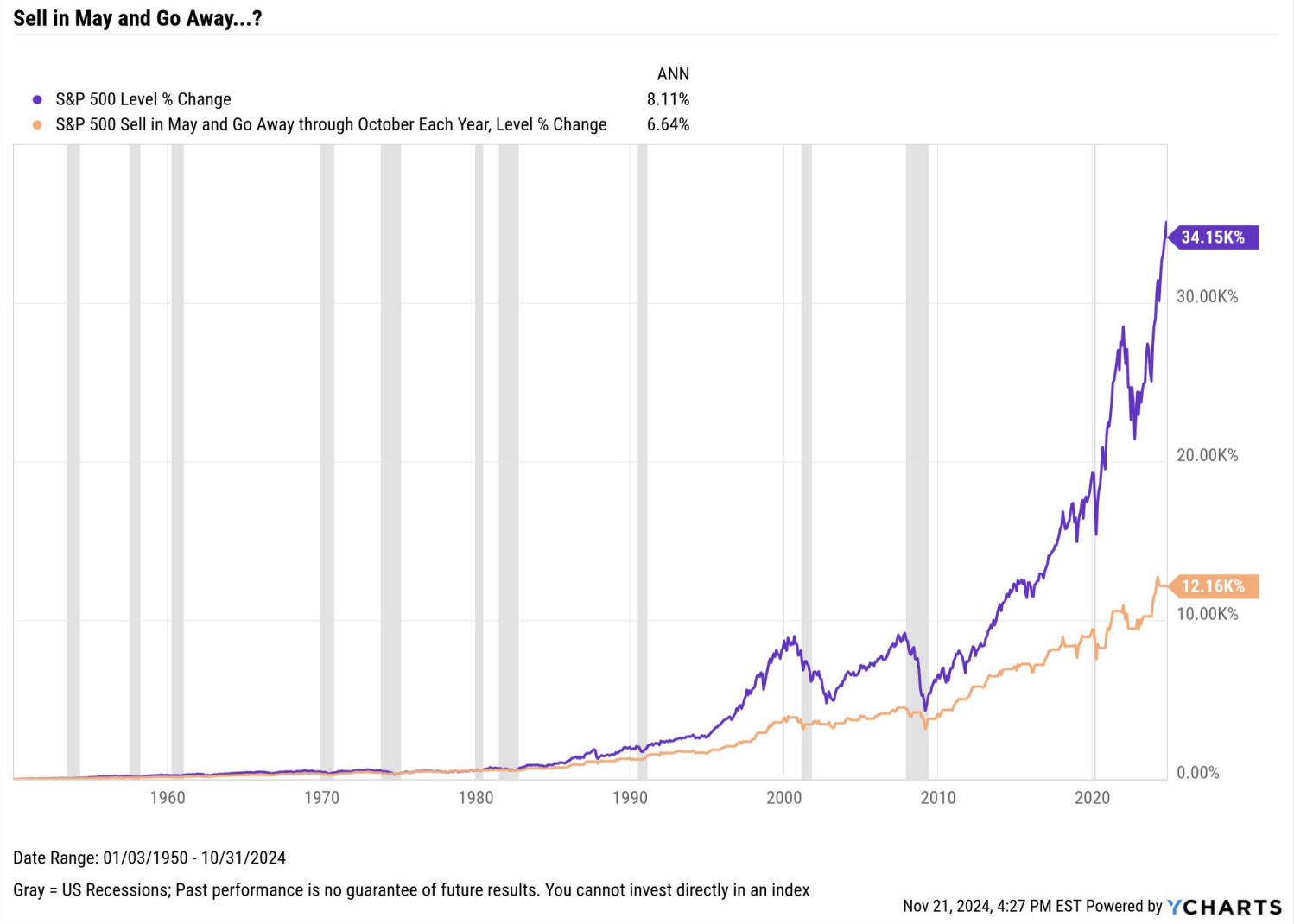

The “Summer Slump” – Real or Perceived?

The idea behind the summer slump is that markets tend to underperform between May and October, compared to the stronger November–April period. The phrase actually originated in London’s financial circles, where many traders would disappear to the countryside for the summer and return in the fall. But does the pattern hold up in North American markets?

Historically speaking, there is some data to support it—but with a big asterisk. Over the past few decades, the S&P 500 has averaged better returns from November to April than during the May–October window. But the difference isn’t massive, and it certainly isn’t guaranteed every year. For example, summer 2020 and 2023 were both strong periods for equities.

What we do tend to see is lower trading volumes during the summer months, which can lead to more volatility and sometimes slower upward momentum. But a “slump”? Not consistently.

Timing Theories: Fun to Follow, Hard to Rely On

The summer slump isn’t the only calendar-based market theory out there. Others include:

- The January Effect: Small-cap stocks supposedly outperform in January.

- Santa Claus Rally: Markets often rise during the last week of December.

- Election Year Cycle: Year three of a U.S. presidential term tends to be strong for stocks.

- Halloween Indicator: Stocks perform better from Oct 31 to May 1.

While there’s some historical evidence behind each, they all share one fatal flaw: they’re not consistent enough to build a plan around. For every year the pattern works, there’s another that breaks the mold.

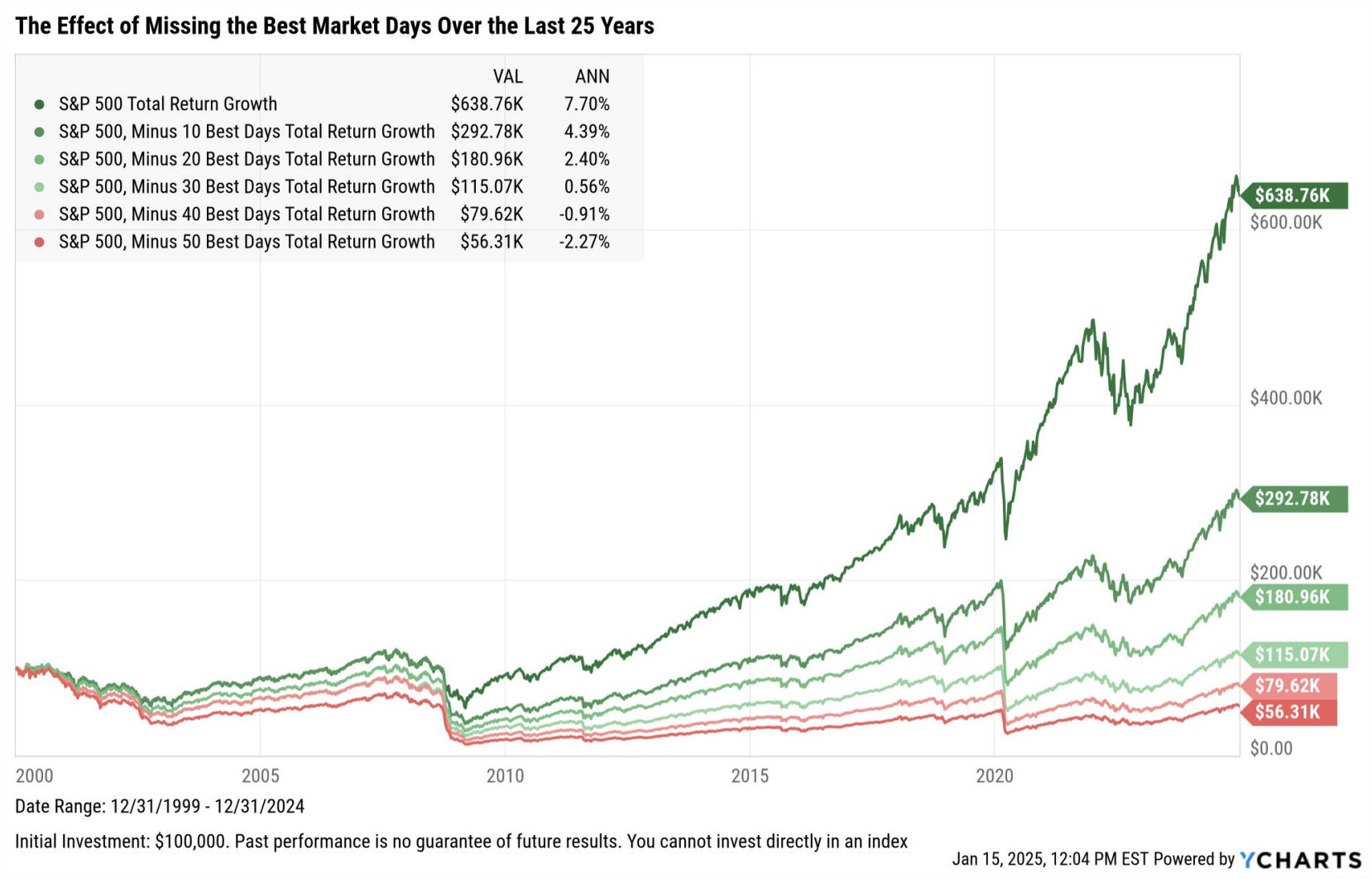

Why Timing the Market Rarely Works

Even if you could correctly predict market seasonality (which is doubtful), missing the market’s best days is devastating for long-term returns.

Consider this: If you missed just the 10 best days in the S&P 500 over the past 20 years, your overall return would be cut in half. And when do those “best days” often occur? Right after sharp drops—when emotional investors have already pulled out.

As Peter Lynch once said: “Far more money has been lost by investors preparing for corrections than has been lost in the corrections themselves.”

So What Should You Do During the Summer?

Instead of worrying about a seasonal slump, here are a few productive strategies:

- Review your plan. The quiet summer months are a great time to step back and ensure your investments still align with your long-term goals.

- Rebalance your portfolio. Take advantage of any asset class shifts to realign your risk.

- Stick to your process. If you’re systematically investing (e.g., dollar-cost averaging), stay the course.

- Look for opportunity. Market pullbacks—summer or otherwise—can be good entry points for long-term investors.

The Cherry Hill Perspective

At Cherry Hill, we don’t invest based on calendar rhymes. We focus on building portfolios that can thrive in all environments—not just the seasonally strong ones.

We diversify with purpose, protect against downside risk, and keep your plan on track through the noise. Whether it’s summer or winter, bull or bear, the key is consistency—not clever timing tricks.

Market Minute

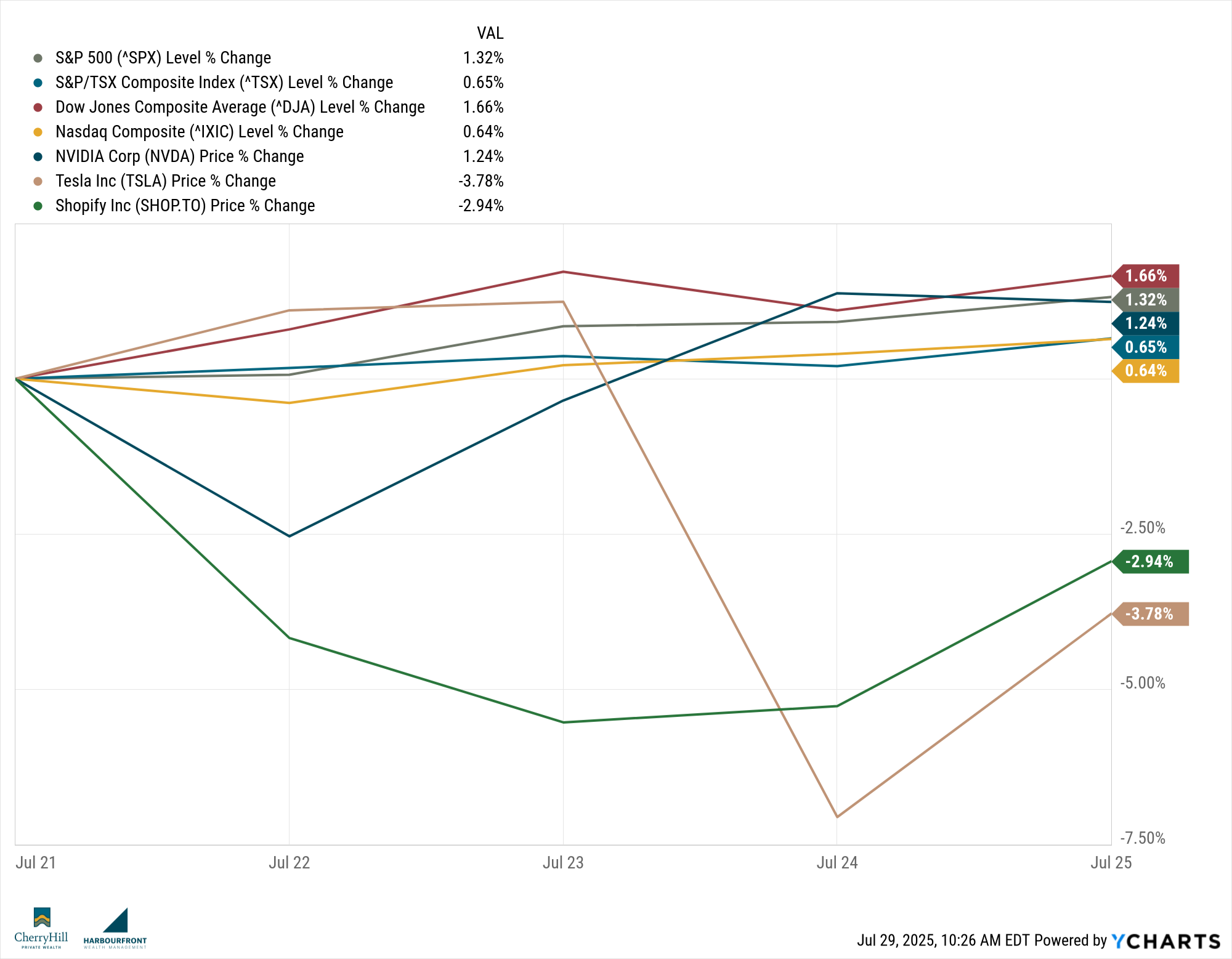

Markets were broadly higher this past week as strong earnings, encouraging economic data, and renewed optimism around global trade supported sentiment. Investors largely brushed off lingering inflation concerns, focusing instead on solid fundamentals and progress in international policy.

Canadian Markets:

The TSX posted a gain of +0.65%, driven by strength in financials and industrials. According to TD Economics, Canadian retail sales softened in May but likely rebounded in June, while business and consumer sentiment showed signs of weakening. Still, the resilience of core sectors helped offset macroeconomic caution. The Bank of Canada is expected to hold rates steady in July, though market participants are watching closely for forward guidance into the fall.

U.S. Markets:

U.S. equities advanced across the board: the S&P 500 rose +1.0%, the Dow gained +1.3%, and the Nasdaq added +2.0%. Earnings from tech heavyweights were a highlight, with Alphabet (+4.4%) outperforming on ad revenue and Amazon (+4%) continuing to impress on margin expansion. Flash PMI data hit a 7-month high at 54.6, indicating economic momentum. A slew of newly signed trade deals — including one with Japan involving a 15% tariff — also boosted confidence. However, Tesla shares declined following a cautious outlook.

Global Markets:

In Europe, the FTSE 100 climbed +1.4% and the STOXX 600 edged up +0.5%, aided by the ECB’s decision to hold rates steady at 2.00%. Germany’s DAX was slightly negative (-0.3%), reflecting ongoing industrial weakness. Japan’s Nikkei soared +4.1% as investors cheered both stimulus speculation and a trade agreement with the U.S. Meanwhile, China’s CSI 300 (+1.7%) and Hong Kong’s Hang Seng (+2.3%) rebounded on hopes of tariff resolution ahead of the August 1 deadline.

Sector Spotlight:

Technology led markets this week, buoyed by robust earnings and continued AI momentum. Companies like Alphabet and Amazon outperformed, while older-economy sectors such as utilities and telecom lagged amid rising yields.

Quote of the Week:

“We are seeing real economic momentum, not just a tech story.”

— Jonathan Curtis, CIO at Franklin Equity Group, speaking on the strength of broad-based U.S. growth

Trends to Watch This Week:

Here’s what were watching this week:

- Canadian GDP (Tuesday): A key gauge of domestic strength and a potential driver of BoC policy direction.

- U.S. Employment Report (Friday): Markets are watching wage growth and job creation to guide Fed expectations.

- Tech Earnings Wrap-Up: The last batch of reports could further validate the AI-driven rally or introduce volatility.

- Tariff Countdown: The 90-day extension on select global tariffs expires August 1; negotiations remain fluid.

Summary:

Equity markets climbed steadily last week, buoyed by strong corporate earnings and a flurry of global trade agreements. With monetary policy largely on pause in North America and Europe, investor attention is now shifting toward economic data and fiscal developments. The tone remains cautiously optimistic heading into August.

Final Thought

Summer slump, new tariffs, conflicts in Europe and the Middle East - markets continue to react in ways that are difficult to predict. If we get closer to the August 1 deadline it’s likely we’ll see more volatility. If history is any indication, it will be temporary.

So, enjoy your time at the cottage, camping, or tending to your garden. Our team and our portfolio managers are making sure that you are well positioned so that you won’t miss out on those “unexpected” great market days.

Until next time, stay informed and strategically invested!

Trevor