Are We Already in a Recession?

In today’s email:

- More layoffs are coming, how does Canada’s economy stack up?

- What is GDP and does it matter?

- If there is a recession, does mean my investments will go down?

- Markets pulled back again this week, but what are we looking at going forward?

The Scoop

Each week, headlines give us new signals about the Canadian economy — but the picture is getting harder to interpret. Last week, TD Bank announced more job cuts, and several major automotive projects were either cancelled or delayed. At the same time, the TSX hit new highs. So, are we in a recession or not?

That’s the question many Canadians are quietly wondering.

What the Indicators Are Saying

Let’s start with the basics. A recession is typically defined as two consecutive quarters of negative GDP growth — but by the time that’s confirmed, it’s already old news. What really matters are leading indicators, and right now, several are flashing warning signs:

- Labour market softening: Job growth has slowed, and job vacancies have dropped across most sectors — even before TD’s latest layoffs.

- Retail sales have declined in multiple provinces, a red flag for consumer confidence and spending power.

- Business investment has cooled, especially in manufacturing and real estate development, both traditionally sensitive to economic downturns.

- The yield curve remains inverted, which has historically been one of the most reliable recession predictors in Canada and the U.S.

While GDP numbers show Canada avoided a technical recession through early 2025, many Canadians don’t feel like the economy is growing — and there’s a reason for that.

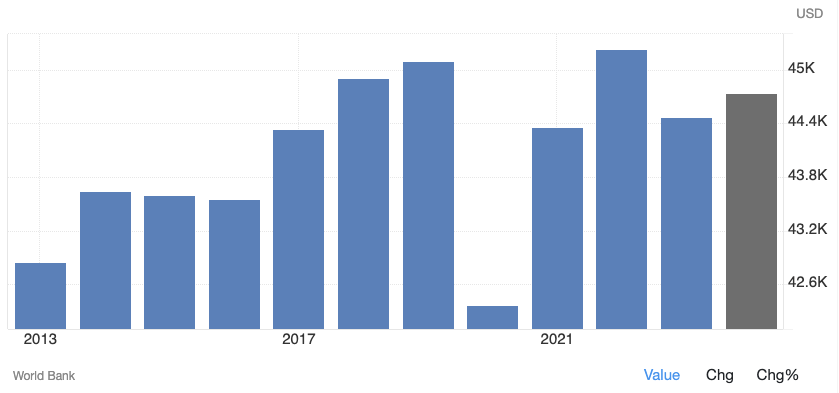

GDP vs. GDP Per Person

On paper, Canada’s economy is growing — but when you factor in the fastest population growth in decades, the picture changes.

GDP per capita — a more accurate measure of individual economic wellbeing — has been in decline for over a year. In other words, while the economy is technically expanding, it’s being outpaced by population growth. That means, on average, Canadians are producing (and often earning) less than they did before.

This mismatch is key. Businesses and policymakers often focus on aggregate GDP, but most Canadians experience the economy per person. And by that measure, we’re already in a per capita recession.

What Could a Recession Mean for Canadian Investments?

Here’s where it gets interesting: markets aren’t always in sync with the economy. Despite the sluggish data, the TSX has reached new highs. That’s largely due to:

- Strength in energy and commodities

- A global rally in tech and AI-adjacent companies

- Expectations of interest rate cuts, which tend to boost asset prices

However, a true recession — or even just slower earnings growth — could pressure Canadian equities, especially in cyclical sectors like financials, industrials, and discretionary retail. Investors may want to review their exposure to these areas.

At the same time, recessionary periods often create opportunity:

- High-quality dividend stocks can provide stability and income.

- Private credit and infrastructure have historically offered downside protection.

- Real estate values may soften, potentially opening doors for longer-term investors.

We continue to believe that portfolios built around diversification, downside protection, and a mix of public and private assets are best positioned to weather uncertainty — and capitalize on it.

One More Thing…

Recessions also shift public policy. We may see:

- Further rate cuts from the Bank of Canada to stimulate growth

- Government stimulus programs focused on housing or infrastructure

- Renewed immigration debates, especially if per capita output remains weak

These could affect everything from borrowing costs to housing affordability and investor sentiment.

The Bottom Line

While Canada may not be in a technical recession yet, many leading indicators — and lived experiences — suggest we’re headed in that direction, or already there in practical terms. But with the right strategy, recessions don’t have to be feared — they can be planned for.

As always, if you want to talk about how this could impact your investments or financial goals, we’re happy to connect.

Market Minute

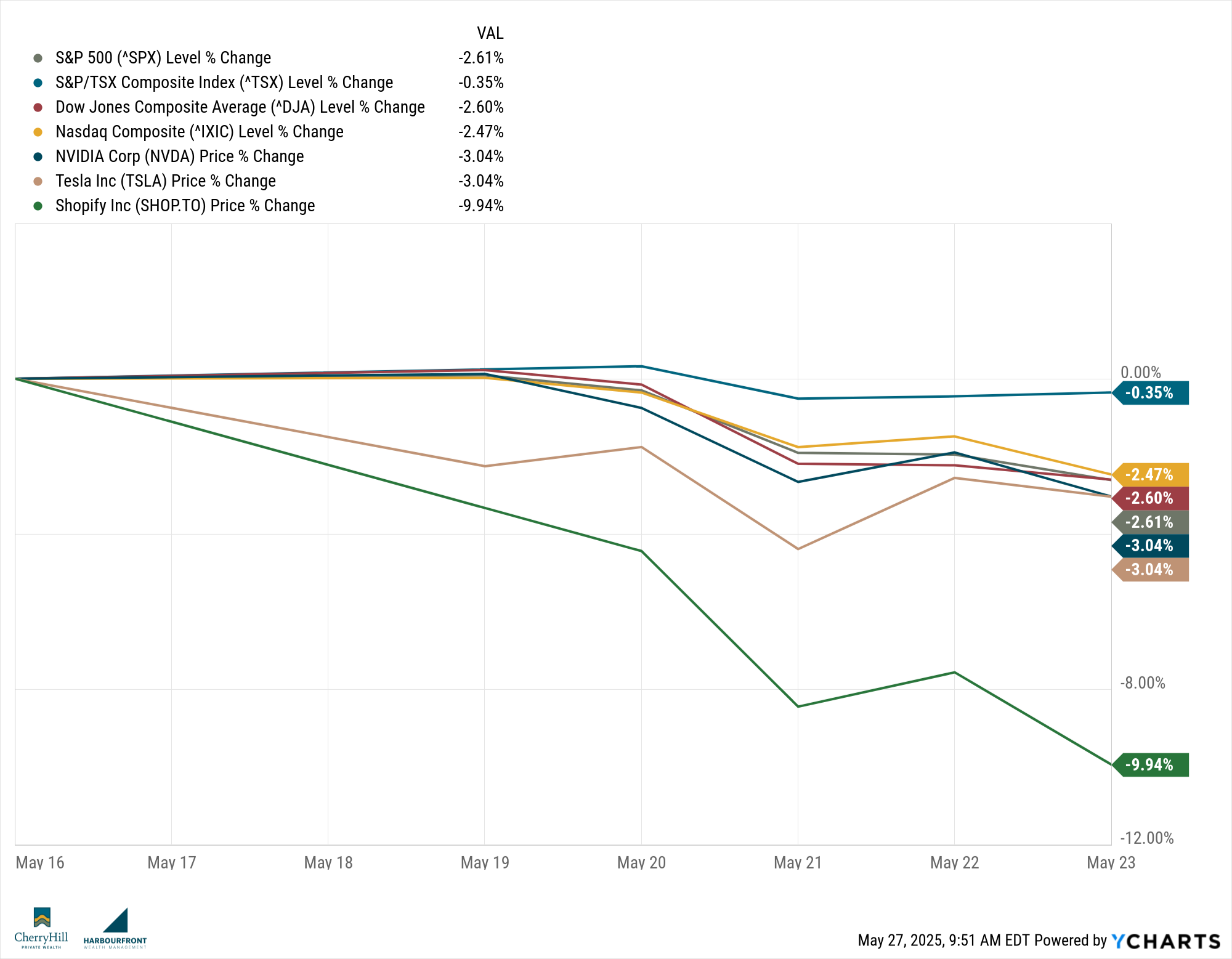

This past week, markets faced renewed volatility as fiscal concerns and geopolitical tensions weighed on investor sentiment. Equities, bonds, and the U.S. dollar all retreated amid a backdrop of rising debt levels and fresh tariff threats.

Canadian Markets:

The TSX Composite Index experienced a modest decline, influenced by global market trends and domestic economic indicators. Energy and financial sectors faced headwinds, while technology stocks showed relative resilience. Investors remained cautious, balancing concerns over economic growth with sector-specific developments.

U.S. Markets:

U.S. equities pulled back, with the S&P 500 declining by 2.6%, the Nasdaq by 2.5%, and the Dow Jones Industrial Average by 2.5%. The retreat followed a near 20% rally since early April. Contributing factors included Moody’s downgrade of U.S. government credit, a weak 20-year Treasury auction, and the House’s passage of a tax bill expected to add nearly $3 trillion to the deficit over the next decade. Additionally, fresh tariff threats reminded investors of ongoing trade uncertainties.

Global Markets:

European markets showed mixed results. The MSCI EAFE index rose by 1.0%, while Germany’s DAX reached a new record high. In contrast, Asia presented a varied picture; Japan’s first-quarter GDP contracted at a 0.7% annualized pace, marking the first negative reading in a year.

Trends to Watch This Week:

- U.S. Inflation Data: Investors will closely monitor the upcoming Personal Consumption Expenditures (PCE) inflation report for insights into the Federal Reserve’s potential policy moves.

- Consumer Confidence: The latest readings on consumer sentiment will provide clues about spending trends and economic outlook.

- Tech Earnings: Key technology companies are set to report earnings, which could influence market direction, especially in the context of recent volatility.

Summary:

Markets are navigating a complex environment marked by fiscal policy shifts, credit concerns, and geopolitical tensions. While recent developments have introduced headwinds, underlying economic fundamentals and corporate earnings will play a crucial role in determining the market’s trajectory in the coming weeks.

Final Thought

We’ve seen a familiar pattern lately — a week of encouraging gains that hints we’ve turned the corner, only to see markets pull back the next. Despite the ongoing volatility and negative headlines, the TSX remains up year-to-date, and major U.S. markets are hovering near breakeven.

It’s easy to get swept up in the doomscrolling or dramatic headlines, but the reality is rarely as bleak — or as rosy — as it’s portrayed. That’s why we continue to position your portfolios to weather the down weeks while staying ready to participate in the rebounds.

Until next time, stay informed and strategically invested!

Trevor