The Psychology of Money:

Keys to Success

2025 has started off with a lot of surprises, which has left many of us trying to make sense of new information every day. This week I’m focusing on the parts of money management that you can control.

In today’s email:

- Not just for turbulent times, The Psychology of Money might be the best money book around. Here are my favourite points from it.

- A boring week in the markets last week, but not any more.

- From a new Canadian PM to Tariffs to a Housing Crisis, here is what happened in news this week that could affect your finances.

- Tax slips and some portfolio changes.

The Scoop

Investing is often seen as a numbers game—returns, percentages, valuations, and models. But if you’ve been in the markets long enough, you know it’s as much about psychology as it is about math. That’s the core lesson from The Psychology of Money by Morgan Housel, a book that explores how our behaviours and beliefs shape our financial success far more than our technical knowledge.

Let’s break down a few key insights from the book that can help us make better financial decisions.

1. Wealth Is What You Don’t See

People often equate wealth with high incomes, fancy cars, or big houses. But true wealth is invisible—it’s the money you don’t spend. Wealth is the freedom and flexibility that comes from financial security, not the outward signals of affluence. This is a major mindset shift. The most financially successful people aren’t necessarily those making the most money, but those who control their spending and save consistently.

2. The Power of Compounding and Time

One of the most famous stories from The Psychology of Money is about Warren Buffett. Yes, he’s a great investor, but the real reason for his immense wealth is time—he’s been investing since he was 10 years old. The longer you let your money compound, the greater the impact. It’s why someone who starts investing early and keeps it simple often outperforms the investor who tries to time the market or chase returns.

This ties directly into what we emphasize in our approach: reducing volatility and ensuring consistency, so you stay invested through all market cycles.

3. Risk vs. Luck: The Fine Line Between Success and Failure

Housel highlights that luck plays a bigger role in finance than we like to admit. Bill Gates had access to one of the first high school computers in the world. Meanwhile, equally intelligent and hardworking people never had that opportunity. When evaluating investments, it’s easy to assume past success was purely skill—but sometimes, good fortune plays a role.

The key lesson? Don’t base your financial strategy on a single story of success. Instead, focus on repeatable, disciplined habits that work over the long term.

4. The Importance of “Enough”

Many financial mistakes happen when people don’t recognize when they have enough. The endless pursuit of “more” can lead to unnecessary risk-taking—whether it’s an investor chasing one last gain before selling, or someone stretching too far for a bigger house.

Understanding what “enough” means for you is crucial in investing. Are you optimizing for financial security, growth, or generational wealth? Your strategy should reflect those personal goals, not what others are doing.

5. Survival Is the Ultimate Investment Strategy

The number one rule of investing is to stay in the game. Avoiding financial ruin is more important than maximizing returns. The best investors don’t necessarily shoot for the highest gains—they ensure they never take risks that could wipe them out.

This is why we focus so much on downside protection in our portfolios. Alternative investments, like private credit, real estate, and infrastructure, are key tools in smoothing out volatility so that you can stick with your plan through market cycles.

Final Thought: Investing Is a Behavioural Game

The best investors aren’t the ones with the most technical knowledge—they’re the ones with the best temperament. They stay patient, avoid panic, and focus on the long-term.

The Psychology of Money reminds us that success in investing isn’t about being the smartest person in the room—it’s about managing our own emotions, behaviours, and expectations.

Market Minute

2025 has been off to a rough start for major public markets. With a rolling tariff threat amongst other uncertain policies South of the border, markets have displayed its frustration. Yesterday marked another red day, which appears to be more of the norm as the U.S. President made comments about a possible recession.

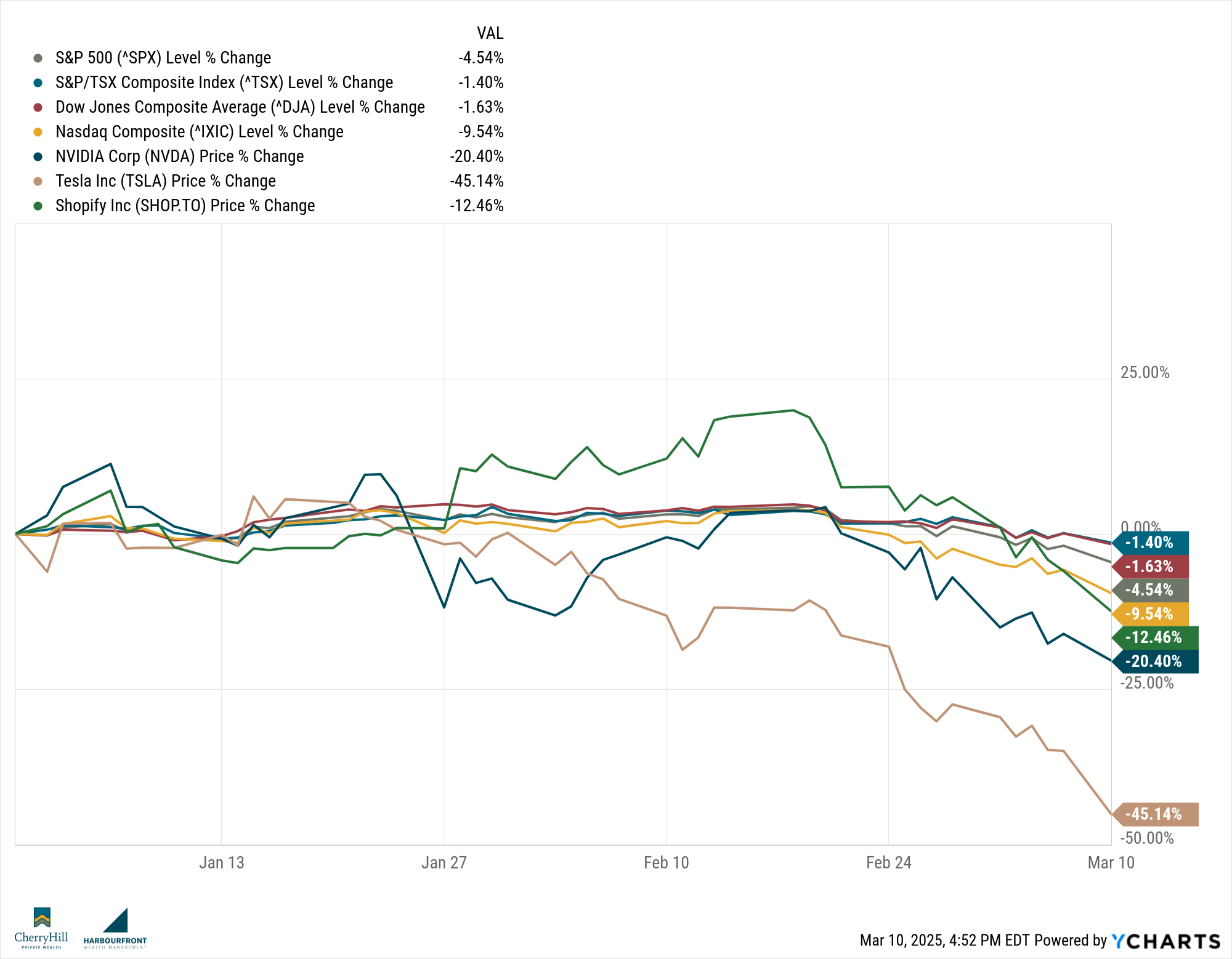

2025 Year-to-Date Market Performance

Canada:

The TSX finished slightly higher this week, up 0.4%, as energy and financials helped offset weakness in technology. Oil prices stabilized around $78/barrel, giving a boost to Canadian producers, while bank earnings showed mixed results—highlighting the ongoing tension between higher interest margins and rising loan loss provisions.

United States:

U.S. markets posted a modest gain, with the S&P 500 up 0.6% and the Dow Jones up 0.3% for the week. Technology and consumer discretionary led the way, but investors are still grappling with uncertainty over when the Federal Reserve will start cutting rates. Comments from Fed officials suggested that while inflation is cooling, they’re not ready to declare victory just yet. Apple and Microsoft were key drivers, both reporting stronger-than-expected earnings.

Global:

Global markets were mixed, as European indices were held back by weak manufacturing data, while Asian markets saw a small rebound after weeks of selling. China announced more targeted stimulus to support its struggling property sector, which lifted sentiment temporarily but didn’t fully calm concerns over broader economic weakness.

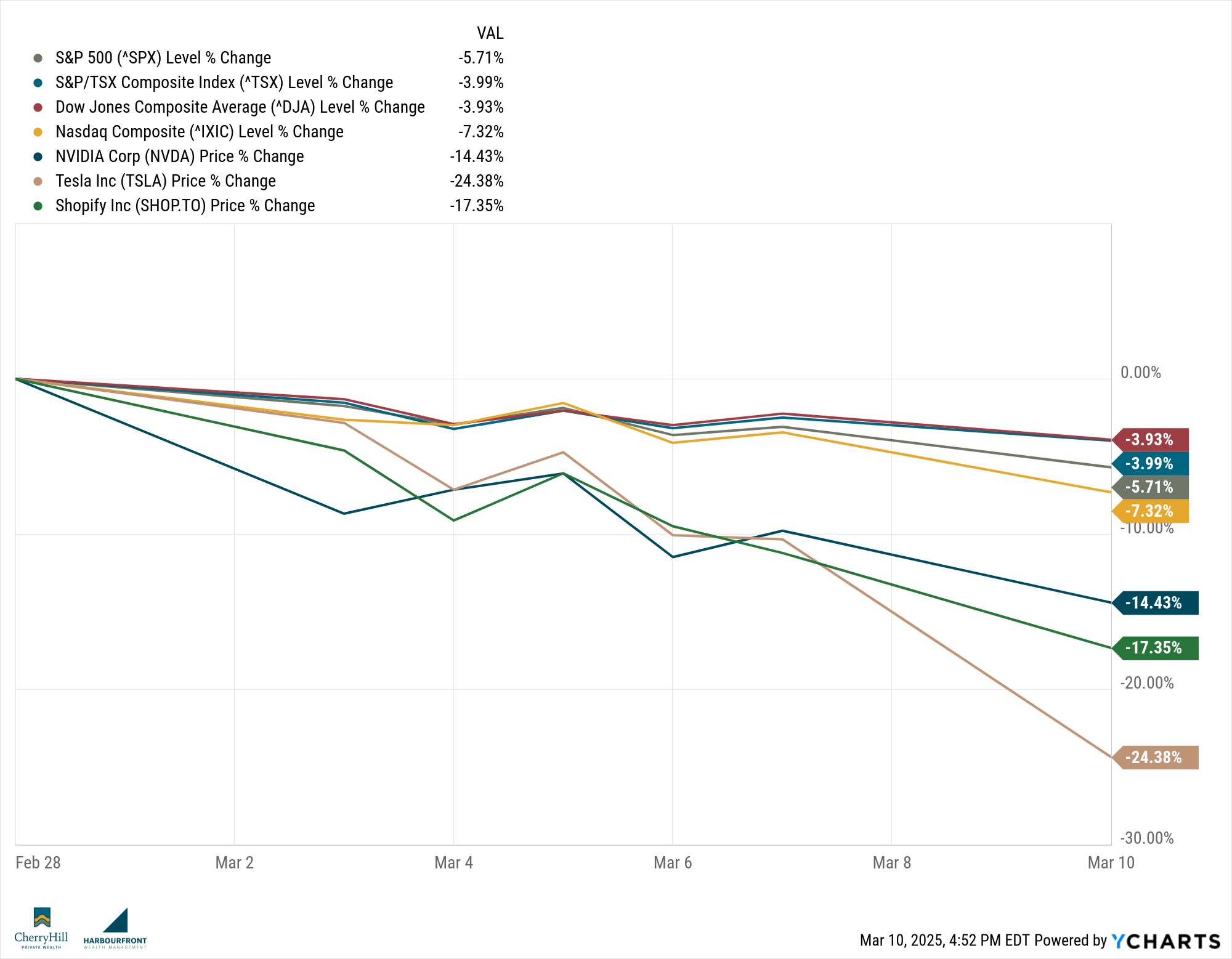

Last Week’s Market Performance, Including Monday, March 9

Trends to Watch This Week

- U.S. inflation data (CPI) set to be released—markets will be watching closely for signs that inflation continues to moderate.

- Bank of Canada speaks on monetary policy—investors are looking for hints about potential rate cuts in the second half of the year.

- Corporate earnings season continues, with a focus on consumer companies—giving insight into how resilient household spending remains.

Markets remain very fluid from week to week, but our team is weighing the short-term turbulence with providing you long-term results. Over the past several months we have de-risked many of our positions and continue to cut through the “noise” to give you the best results possible. With our ability to invest in private credit, private equity, private real estate, infrastructure, and other “Alternative” asset classes, we have your portfolios well positioned for what’s to come.

News Update

This week I wanted to take a quick look at what has been happening in the news and how it affects your investments. This will be a semi-regular section and will focus on big news items that affects your financial situation. If you want to dive deeper into any of the topics, please reach out - we’re always open for a more in-depth discussion.

Canadian Politics – New Prime Minister, New Direction?

In a political shakeup, Canada has a new Prime Minister, not elected directly by Canadians, but chosen as leader of the ruling party to replace the outgoing PM. While it isn’t a first for a change in Prime Minister mid-term (the first was John Turner replacing Pierre Trudeau in 1984), this will be the first time in history where the PM hasn’t held a seat as a Member of Parliament.

With Canadians facing stubborn inflation, a housing crisis, pressures from the U.S., and slowing economic growth, all eyes are now on how the new Prime Minister will approach these pressing issues. Early signals suggest a renewed focus on affordability, housing, and rebuilding public trust, but major policy shifts are still unclear. Investors and households alike will be watching closely for any new fiscal measures, tax adjustments, or spending programs that could impact both personal finances and broader economic stability.

Tariffs and Trade:

Trade tensions are heating up as Canada considers matching U.S. tariffs on Chinese electric vehicles (EVs). The U.S. recently announced sweeping tariffs on Chinese EVs and components, and Canada is now weighing whether to follow suit. While aimed at protecting North American manufacturing, these tariffs could raise prices on EVs and related technologies for Canadian consumers, and potentially disrupt auto sector supply chains. This could also affect inflation, which remains a top concern for policymakers.

With a Trade War gaining unprecedented momentum, the U.S., this morning, vowed to raise the tariffs on Steel and Aluminum to 50%. This appears to be in retaliation to an Ontario electricity surcharge being implemented. Trump has also reiterated his desire to annex Canada as well as penalizing Canadian lumber, automobiles (promising to destroy this industry), dairy and penalizing Canada for is defence spending.

Housing Policy in Focus:

With housing affordability a top priority for Canadians, the government is expected to introduce new incentives for developers to increase housing supply—possibly through relaxed zoning rules and faster permitting processes. However, these solutions will take time to materialize, and Canadians facing mortgage renewals or trying to buy homes are still feeling significant pressure as borrowing costs remain high.

Inflation and Cost of Living:

Although inflation has moderated slightly, groceries, rent, and mortgage costs remain elevated. The Bank of Canada continues to signal caution, walking a fine line between holding interest rates steady to avoid further strain on borrowers and preparing for potential rate cuts if the economy continues to slow. Canadians should expect continued cost-of-living challenges in the short term, with gradual relief possibly on the horizon if rates eventually fall.

CHPW Update

As the rush to get taxes files starts coming down, we wanted to send a quick reminder as to when you will be receiving you tax slips for your Watermark Private Portfolios. Since these investments contain private holdings, they are reported to us later than public investments. The tax slips will be mailed out by March 31. We will also have soft copy access to these slips as of this date, so if you are trying to file early, your accountant will not have all the information. We can send you the .pdf version if you reach out to us as they become available to us.

Also, when it comes to portfolio construction, I am often getting asked about how they stand up to the volatility that we’re seeing recently. The landscape is scary and we understand your trepidation. This morning we received the trade notes on Enhanced Conservative and Balanced portfolios. In February, our team trimmed the Dynamic Active Enhanced Yield ETF, which holds many growth and technology stocks. They are now adding this back to the portfolios, saying, “We feel this is a good place to add back to equities, however, we may be quick to take any profits and go back to cash.” At a better value than last month, they can take advantage of this volatility and make sure that you are always in the best position to be protected on the downside, while not losing out on the upward swings.

Final Thought

This was a bigger newsletter than I initially intended, so thank you for ending up here! There is a lot going on right now and our team is here for you. Our portfolio management team is working hard to set your investments up for success, while the Cherry Hill team is here to make sure you have all the information to make the best decisions. If you are feeling uneasy or want to discuss anything that is happening right now - we are here for you. Click the link below and book a time with us, give us a call, or send us an email.

Until next time, stay informed and strategically invested!

Trevor