Markets Crash - Run for the Hills

Over-the-top headlines like this are used by news sources all the time to catch our attention and inflict a sense of panic. This week, I thought it was a good time to reflect on some of the major headlines in 2024 and look at how they actually affected your investments.

Also - the RRSP Deadline is March 3.

In today’s email:

- When is “noise” just noise in the media?

- Five lessons from 2024.

- North American markets has a rough week, with the Dow and Nasdaq having their worst week since October.

The Scoop

This weekend I was scrolling through the news and it occurred to me how many headlines are out there right now that could lead investors to make poor decisions. It also got me thinking about how many headlines we saw last year that had similar affects. So, for this newsletter, I wanted to take a moment to look back at 2024—a year filled with market-moving headlines, predictions, and reactions. It felt like every week brought a new narrative that seemed poised to reshape the financial landscape. But did those headlines actually have the impact everyone expected?

Let’s break down some of the major stories of 2024, what was anticipated, and how the markets actually reacted. There are some valuable lessons here that can help guide our thinking for 2025.

Headline #1: The Inflation Rollercoaster

The Noise: Early in 2024, inflation readings remained stubbornly above target levels, leading to widespread fears that central banks would delay rate cuts. Many analysts predicted prolonged high-interest rates, a stalled housing market, and slowing growth.

Anticipated Impact: A pullback in equity markets, rising bond yields, and a slowdown in consumer spending.

What Actually Happened: While there were short-term dips in equity markets following inflation reports, markets rebounded as investors priced in eventual rate cuts. The bond market reacted with volatility, but longer-term yields stabilized by year-end. Consumer spending slowed slightly but remained resilient.

Lesson for 2025: Markets often price in bad news quickly. Inflation fears didn’t derail long-term growth, reminding us that reacting too quickly to short-term data can lead to missed opportunities.

Headline #2: Geopolitical Tensions Surge

The Noise: Geopolitical conflicts, particularly in Eastern Europe and the Middle East, dominated headlines. Pundits warned of supply chain disruptions, higher energy prices, and increased market volatility.

Anticipated Impact: Energy prices surging, global markets dipping, and a flight to safe-haven assets like gold and the U.S. dollar.

What Actually Happened: While there was initial volatility in energy markets, global equities proved surprisingly resilient. Energy prices normalized faster than expected, and although safe-haven assets saw short-term gains, risk assets performed well by the end of the year.

Lesson for 2025: Markets have a remarkable ability to look beyond geopolitical uncertainty, especially when underlying economic fundamentals remain strong.

Headline #3: Central Bank Pivot (Finally)

The Noise: After months of speculation, the Federal Reserve and Bank of Canada finally cut interest rates in the second half of 2024. The narrative shifted from fears of “higher for longer” to optimism about a soft landing.

Anticipated Impact: Surge in equities, declining bond yields, and a revival of the real estate market.

What Actually Happened: Equities indeed rallied, particularly in rate-sensitive sectors like technology and real estate. However, bond markets didn’t react as dramatically, suggesting investors were still cautious about inflation’s stickiness. The real estate market saw a modest recovery but remained tempered by affordability challenges.

Lesson for 2025: Rate cuts are positive for markets, but the extent and timing matter. The market had already priced in some of the optimism, showing the importance of staying invested rather than trying to time these events.

Headline #4: The AI Boom – Real Growth or Hype?

The Noise: 2024 saw an explosion in AI-related investments, with companies touting breakthroughs that promised to revolutionize industries. Analysts predicted a tech-led bull market.

Anticipated Impact: Massive growth in tech stocks, valuations soaring, and potential bubble warnings.

What Actually Happened: Tech stocks, especially those tied to AI, did see strong performance, but valuations cooled as investors sought real earnings growth. While AI remains a transformative theme, the market started distinguishing between hype and substance.

Lesson for 2025: New technologies can drive growth, but fundamentals still matter. Investors should stay focused on companies with solid business models and real earnings potential.

Headline #5: U.S. Election Uncertainty

The Noise: As the 2024 U.S. presidential election approached, uncertainty around potential policy shifts spooked markets. Concerns ranged from trade wars to tax policy changes.

Anticipated Impact: Elevated volatility, investor caution, and possible market pullbacks.

What Actually Happened: Volatility did rise briefly, but markets quickly adjusted post-election. Investors realized that regardless of the outcome, fundamental economic forces remained unchanged.

Lesson for 2025: Political uncertainty creates noise, but markets care more about economic fundamentals than political drama.

Key Takeaways for 2025

- Don’t Overreact to Headlines: Short-term volatility often doesn’t translate into long-term trends. Staying disciplined is key.

- Market Expectations Matter: Often, the market reacts not to the event itself, but to how the outcome compares to expectations.

- Focus on Fundamentals: Earnings growth, interest rates, and economic health still drive long-term returns.

- Diversification Wins: From geopolitical tensions to sector-specific booms, diversified portfolios proved resilient again in 2024.

Final Thoughts

Looking back at 2024, it’s clear that while the headlines were dramatic, the markets responded with a degree of calm that defied many expectations. As we move through 2025, remember that disciplined investing—rooted in long-term thinking—remains the best strategy.

If you’d like to discuss how these lessons apply to your portfolio or what opportunities might arise in 2025, don’t hesitate to reach out.

Market Minute

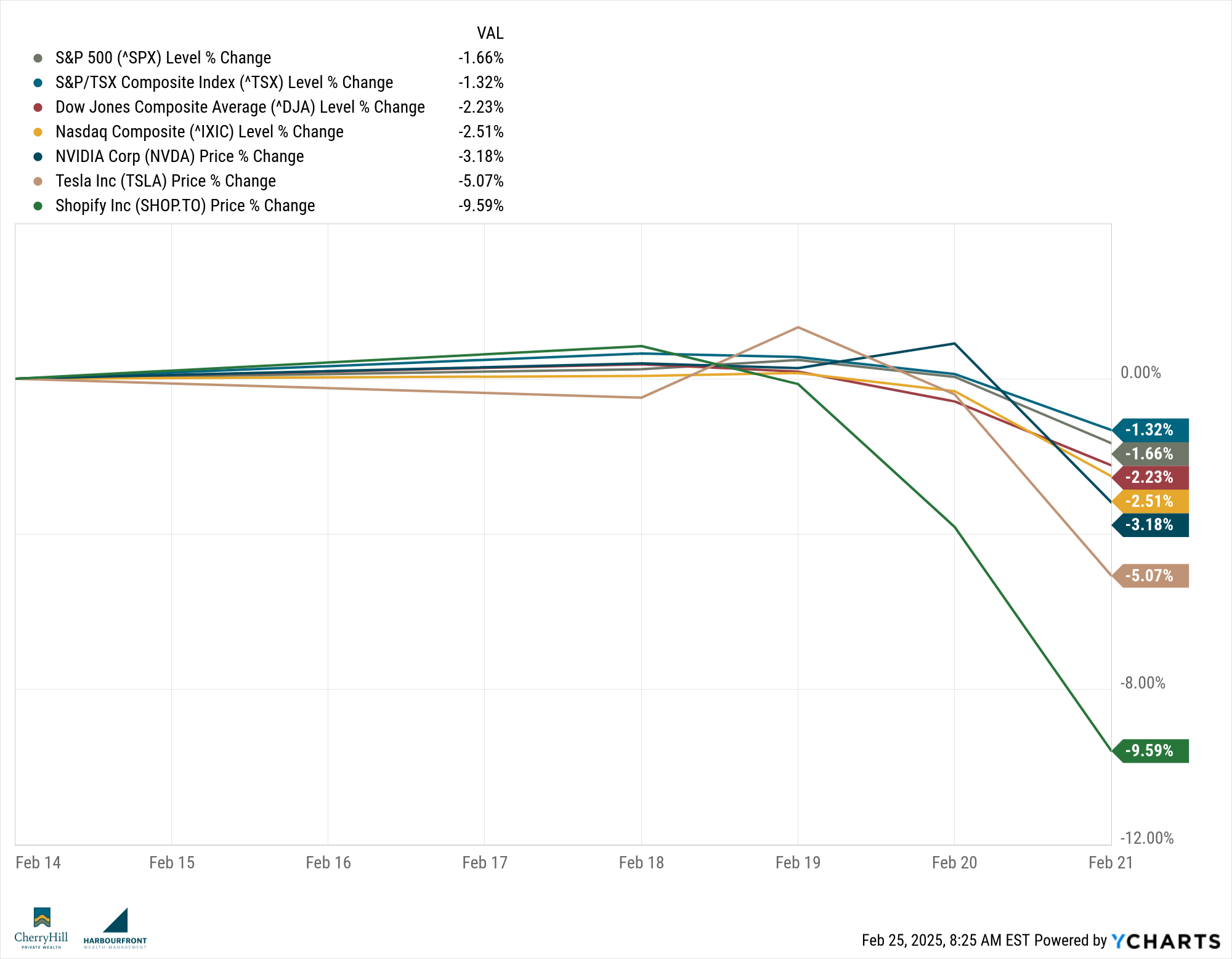

As we move towards the final weeks of February, the markets, globally, continue their volatile start to the year. Year-to-date, most indices are positive, but have had mixed results week to week.

United States:

U.S. markets saw notable declines last week, with the Dow Jones Industrial Average dropping 2.23%, the S&P 500 falling 1.66%, and the Nasdaq Composite decreasing by 2.51%. These losses were driven by disappointing economic data showing a slowdown in business activity and rising consumer inflation expectations. Additionally, Walmart’s conservative sales forecast raised concerns about the resilience of consumer spending, adding to investor caution. For the week, both the Dow and Nasdaq posted their largest drops since late October.

Global:

Globally, investor sentiment was mixed, with European markets showing relative resilience despite concerns about slowing global growth. However, hedge funds were reported to be exiting tech and media stocks at the fastest pace in six months, reflecting caution around high-valuation sectors. Additionally, the Federal Reserve’s announcement of an exploratory analysis focusing on risks posed by nonbank financial institutions highlighted growing regulatory attention to private credit markets, which are becoming more interconnected with traditional banking systems.

Canada:

In Canada, the S&P/TSX Composite Index declined by 1.32% on Friday, closing at 25,147.03, marking its lowest level since mid-January. The index fell as concerns about slowing U.S. economic activity and cautious corporate earnings guidance weighed on investor sentiment. Canadian markets tracked U.S. performance closely, with energy and financial sectors seeing particular pressure.

Key Influencing Factors:

- Economic Data: Reports in the U.S. indicated a slowdown in business activity, with rising consumer inflation expectations contributing to market declines. Weak retail sales and cautious corporate earnings forecasts added further pressure.

- Corporate Activity: Walmart’s conservative outlook on sales signalled potential softness in consumer spending. In the private equity space, KKR submitted a £4 billion bid to acquire a majority stake in Thames Water, highlighting continued interest in infrastructure investments.

- Private Markets: Neuberger Berman closed its third specialty-finance fund, raising over $1.6 billion, reflecting robust investor interest in asset-based finance strategies. However, the Federal Reserve’s focus on risks from private credit funds signals growing regulatory scrutiny in this rapidly expanding market.

Trends We’re Watching

- Private Market Growth: The surge in capital toward private credit strategies underscores their increasing relevance. However, regulatory developments could shape future opportunities and risks in this sector.

- Economic Indicators: With rising inflation expectations and slowing business activity, upcoming economic reports, including PMI indexes and retail sales data, will be key in assessing the trajectory of North American markets.

- Regulatory Developments: The Federal Reserve’s exploratory analysis into nonbank financial institutions, including private credit funds, could have significant implications for the private lending landscape, particularly given its growing links to traditional banking systems.

Until next time, stay informed and strategically invested!

Trevor