Holiday Prep for Your Portfolio:

5 Smart Financial Moves to Make Now

As we start closing out 2024 and look to the future, it’s important to take a short pause to ensure you end the year right. We have put together 5 things that will make sure you start 2025 on the right foot!

In today’s email:

- Even in your favourite Santa onesie, everyone can check these 5 items of their year-end planning list.

- Turmoil in the Canadian political arena, but the cracks might be deeper as it was a tough week for investors on both sides of the border.

- 2.4 million books given away for a store promotion and we have one of the most iconic Christmas characters.

- ‘Tis the season for giving and the CHPW team was out and happy to see so many of you!

The Scoop

It’s that magical time of year when the snow starts to fall, holiday lights go up, and you’re wondering if it’s too early to dig into the eggnog. (Spoiler alert: It’s never too early.) But amidst all the festivities, there’s one other tradition we need to uphold: year-end tax and investment planning. Before you groan and reach for another shortbread cookie, remember this—a little effort now could save you a lot of money (and stress) later. So, let’s dive into the Top 5 Things Every Canadian Investor Should Do Before Year-End:

1. Max Out (or Catch Up on) Your TFSA Contributions

Think of your Tax-Free Savings Account as Santa’s sleigh—it carries your investments tax-free through the skies of Canadian markets. If you haven’t maxed out your contributions for 2024, now’s the time. Any unused room rolls forward, but why wait? Maxing out early means more time for your investments to grow without the government taking a cut.

Quick tip: Not sure how much room you have? Check your CRA My Account or give us a call.

2. Tax-Loss Harvesting: Turning Lemons into Lemonade

Not every stock had a good year, and that’s okay. Selling investments at a loss can offset gains from your winners, reducing your overall tax bill. But remember, you can’t just sell and buy it back right away. The CRA has a “superficial loss rule” that requires you to wait 30 days before repurchasing the same asset.

Pro tip: If you’ve got a portfolio with us, we can help you identify tax-loss harvesting opportunities—no lemon-squeezing required.

3. Give Generously (and Tax-Efficiently)

‘Tis the season of giving, and donating publicly traded securities with unrealized gains to a registered charity is a win-win. You’ll get a tax receipt for the fair market value and avoid capital gains tax altogether. It’s like spreading holiday cheer and keeping the CRA off your back.

4. Review RRSP Contribution Limits

While the RRSP deadline isn’t until March 1st, 2025, contributing before December 31st gives you extra time for tax-deferred growth. Plus, if you’ve had an unusually high-income year, topping up now can help bring down your taxable income for this year.

Hot tip: Planning a big withdrawal in the next couple of years (say for a home purchase)? Using the First Home Savings Account (FHSA) could be a great option. This would have to be opened before the end of the year to accumulate contribution room for 2024. It’s also important to top up any other accounts that have calendar limits like RESPs and RDSPs.

5. Rebalance Your Portfolios

Markets have had their ups and downs this year (as always), which means your asset allocation might be out of whack (and likely too aggressive right now). Year-end is the perfect time to rebalance—selling high-performing assets and reinvesting in underperforming ones—to ensure you’re still aligned with your goals. Think of it as tidying up before the new year.

And let’s not forget: this is also a great time to chat about any major life changes that could impact your financial plan. Marriage? New baby? Dinosaur-themed room makeover for the kid? These things matter, and we’re here to help.

Market Minute

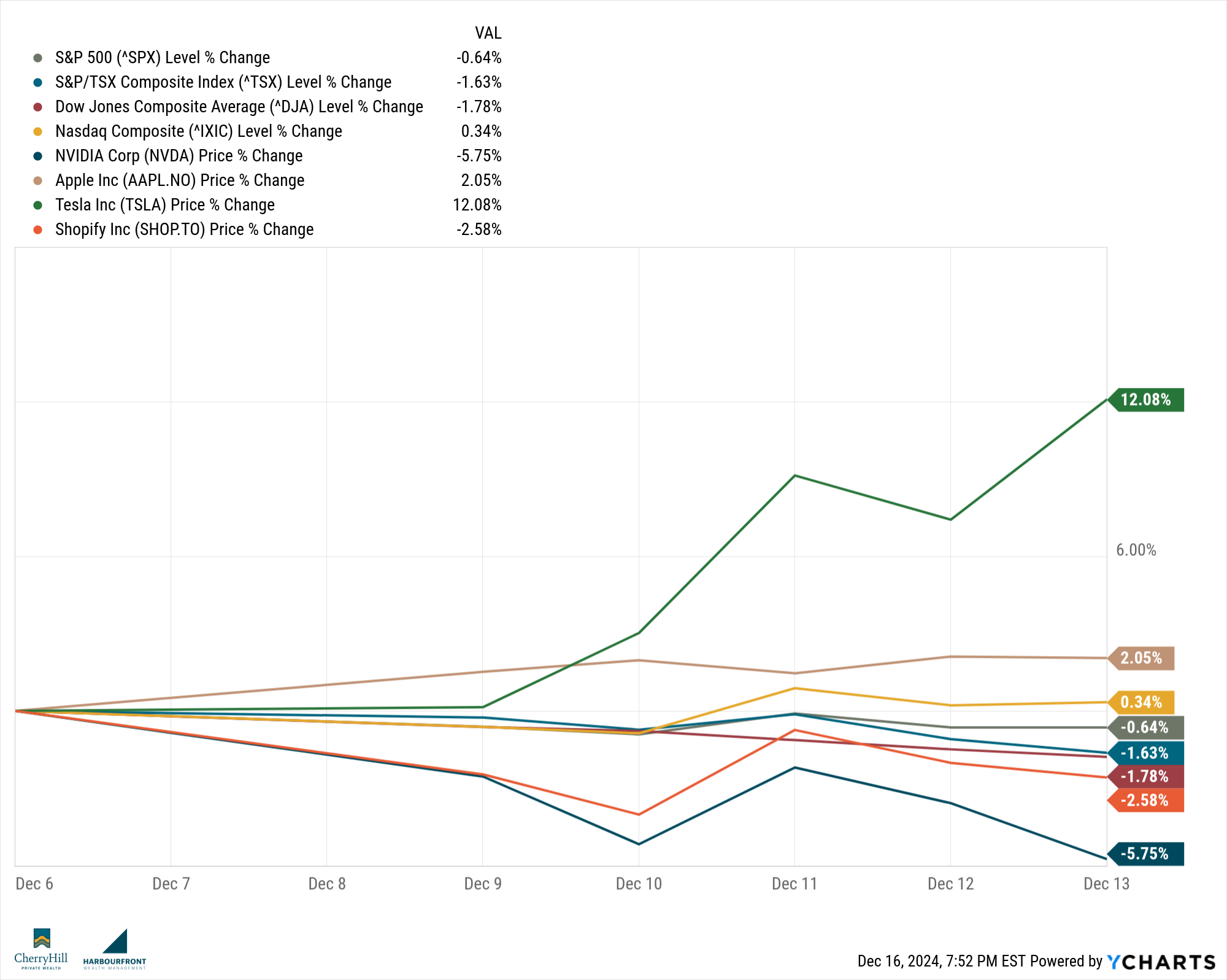

Last week, major North American stock markets exhibited mixed performances amid economic policy shifts and geopolitical concerns.

In Canada, the S&P/TSX Composite Index experienced a decline, influenced by resource sector weaknesses and apprehensions about potential U.S. trade tariffs under President-elect Donald Trump. The Bank of Canada’s recent decision to cut its benchmark interest rate by 50 basis points to 3.25% aimed to stimulate the economy but also contributed to market volatility.

In the United States, the Nasdaq Composite briefly surpassed the 20,000 mark, driven by robust performances in major tech stocks, including Tesla and Alphabet. However, the broader market showed signs of underlying weakness, with the S&P 500 experiencing more declines than gains over ten consecutive days, the longest streak since 2000.

Canadian Dollar and Interest Rates:

The Canadian dollar reached a 4.5-year low against the U.S. dollar, trading at 1.4230 per U.S. dollar, influenced by a widening yield spread between Canadian and U.S. bonds. This depreciation is partly due to the Bank of Canada’s rate cuts and concerns over potential U.S. tariffs on Canadian imports.

These developments underscore the dynamic nature of the current economic landscape, with central bank policies and geopolitical factors playing significant roles in shaping market movements.

This week, several key developments are influencing mark markets, particularly in Canada and the United States.

Canadian Markets and the Canadian Dollar:

The unexpected resignation of Canada’s Finance Minister, Chrystia Freeland, has introduced political uncertainty, impacting financial markets. The Canadian dollar (loonie) reached a 4.5-year low against the U.S. dollar, trading at 1.4268 before recovering to 1.4225. This volatility is attributed to concerns over fiscal policy direction and potential economic implications.

Additionally, the Bank of Canada’s recent 50 basis point interest rate cut to 3.25% aims to stimulate the economy amid weaker-than-expected growth and a softening labor market. This monetary policy adjustment has contributed to the loonie’s depreciation.

U.S. Markets and Federal Reserve Actions:

In the United States, markets are focused on the Federal Reserve’s upcoming meeting, where a 25 basis point interest rate cut is anticipated, bringing the federal funds rate to a range of 4.25% to 4.5%. Investors are particularly attentive to the Fed’s guidance on monetary policy for 2025, especially in light of President-elect Donald Trump’s proposed economic policies, including potential tariffs on imports.

The Lighter Side

Rudolph the Red-Nosed Reindeer has become synonymous with Christmas and making sure that the Big Guy dressed in Red is able to get through all the potential wintery weather. Rudolph first appeared in 1939 as part of a promotional campaign for the Montgomery Ward department store. The store’s advertising writer, Robert L. May, created the character to spread holiday cheer through a children’s storybook given out during the holiday season. The story follows Rudolph, a young reindeer teased for his glowing red nose, who ultimately saves Christmas by guiding Santa’s sleigh through a foggy night.

Rudolph’s popularity skyrocketed when songwriter Johnny Marks, May’s brother-in-law, turned the story into the now-iconic Christmas song in 1949, sung by Gene Autry. It has since become a beloved holiday classic, inspiring TV specials, movies, and countless holiday traditions.

Here are some fun facts about the Red-Nosed Reindeer:

- He Was Almost Named “Rollo” or “Reginald”: Before settling on “Rudolph,” Robert L. May considered names like “Rollo” and “Reginald,” but neither felt right. “Rudolph” had a catchy, whimsical feel.

- His Story Was a Holiday Giveaway: Montgomery Ward gave away over 2.4 million Rudolph storybooks in its first year. The book’s popularity led to repeat printings in subsequent years.

- Rudolph’s TV Special Was a Stop-Motion Milestone: The classic 1964 TV special used “Animagic” stop-motion animation, making it a groundbreaking holiday production that still airs annually.

- He Inspired a Science Study: In 2012, Norwegian scientists studied why Rudolph’s nose might glow. Their theory? His nose has a dense network of blood vessels to keep it warm in freezing weather—science meets holiday magic!

The CHPW Team

Last week the Cherry Hill team was out in Milton, supporting the Salvation Army. The team rang the bell and helped raise money to provide food and toys for families that are in dire need of some support.

We loved seeing the generosity of so many who were so busy at this time of year. It was also wonderful seeing many of our friends and clients that popped by to give a donation and say “hi”!

If you have found this valuable, please pass it along to your friend or family member that would benefit from an unbiased take on what’s happening in the markets and how it actually affects their family.

Until next time, stay informed and strategically invested!

Trevor