The Next 10 Years: The Forecasts

A friend asked me last week, “Hey, Trev, what are your team’s forecasts for the next 10 years?” My response was, “Up.” I feel pretty safe in my prediction, but it got me thinking about recent JP Morgan and Goldman Sachs’ 10-year forecasts. I dove deep on long-term forecasts to determine how much stock we should put into them.

In today’s email:

- Everyone has a market prediction, but should we care?

- Bloomberg warns us to “strap into your seat… there’s a pretty potent cocktail of potential volatility”

- Halloween is almost here - here are some facts that you definitely did not need to know!

- Apparently there’s an election happening South of us. Adrian and I have a discussion on what possible outcomes could mean to your portfolio.

The Scoop

As we look ahead into the coming decade, predictions from major investment firms suggest a range of future returns—and some are strikingly modest. JP Morgan, for instance, recently set a conservative tone with its forecast of a 3% average annual return across assets over the next 10 years. This projection contrasts with their more optimistic views in past cycles, where the outlook was driven by low inflation, low rates, and high returns on both stocks and bonds. For context, JP Morgan’s 2013 projections, coming off the financial crisis, suggested a stronger rebound for equities, expecting returns above 6% for a globally diversified portfolio.

Interestingly, not every firm shares JP Morgan’s current conservative outlook. Both BlackRock and Vanguard project more favourable returns, especially for equities. BlackRock forecasts an average return of 6-7% for global stocks, backed by emerging technologies like AI, which they believe will spur productivity and growth. Vanguard also expects 5-6% returns for global equities, driven by stabilizing inflation and opportunities in international markets, where valuations are potentially more attractive compared to the U.S.

What’s Changed in These Forecasts?

These forecasts are shaped by the broader shifts we’ve seen in global markets over the last decade. From 2010 to 2020, low-interest-rate policies and quantitative easing led to significant equity gains and strong bond returns. As a result, the 10-year forecasts in that period were more bullish. In today’s environment, however, higher interest rates, inflation volatility, and geopolitical challenges are making forecasters more cautious.

JP Morgan’s expectation of a 3% return now reflects this changed landscape, but even they acknowledge there may be positive “surprises” on the horizon. Their model accounts for downside risks, such as credit stress in certain sectors, but also hints at the possibility that robust technology adoption could drive stronger-than-expected growth, especially in sectors like AI and renewable energy.

Where is the “Smart Money” Going?

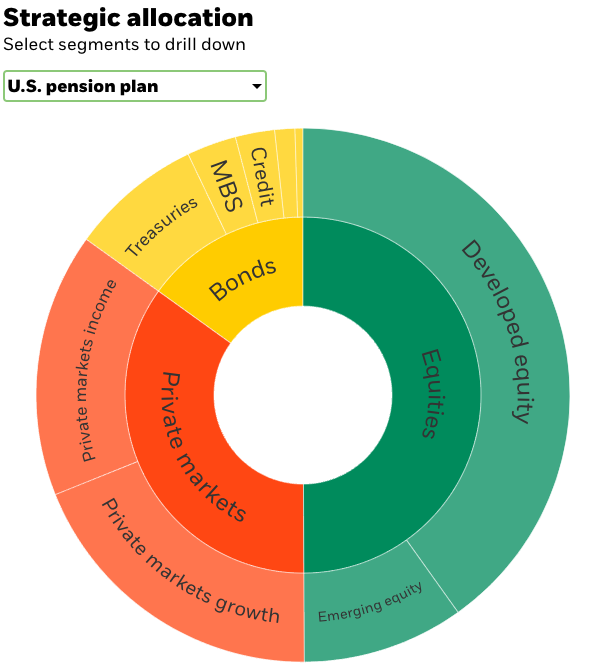

As part of BlackRock’s forecasts, they had a look at how pensions and family offices are allocating their funds. Pension funds and family offices both typically have longer time horizons, so they are always forecasting 10+ years out with their decision making. The U.S. pension plan is forecasting an asset allocation of about 35% in private markets, 50% in public equities, and the remainder in fixed income investments.

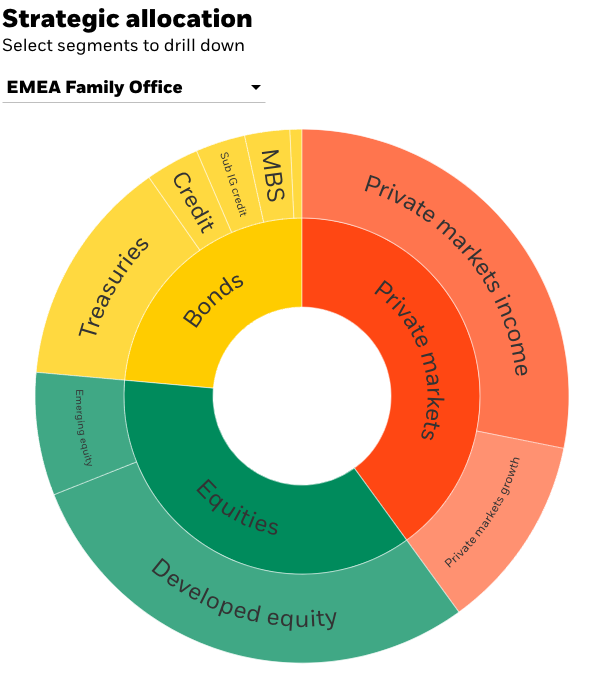

We’ve talked about family offices before, but they are typically set up for families that have a net worth greater than $50 million and often much larger. The family office allocation is similar to the pension fund, with slightly more in the private markets (40%), and slightly less in the public markets (36%).

Even with JP Morgan’s modest return forecasts, they did leave room for alternative investments being attractive options and anticipate these markets, notably private credit, boosting up a soft market.

The Pitfalls of Long-Term Forecasts

With these mixed predictions, one thing is clear: forecasts, especially for a 10-year horizon, are helpful but inherently flawed. Over a decade, countless variables—many of which are unknown or unknowable—can affect outcomes. Relying too heavily on a single forecast could lead investors astray, especially if it encourages conservative portfolios in a more growth-oriented environment or aggressive strategies during periods of heightened risk.

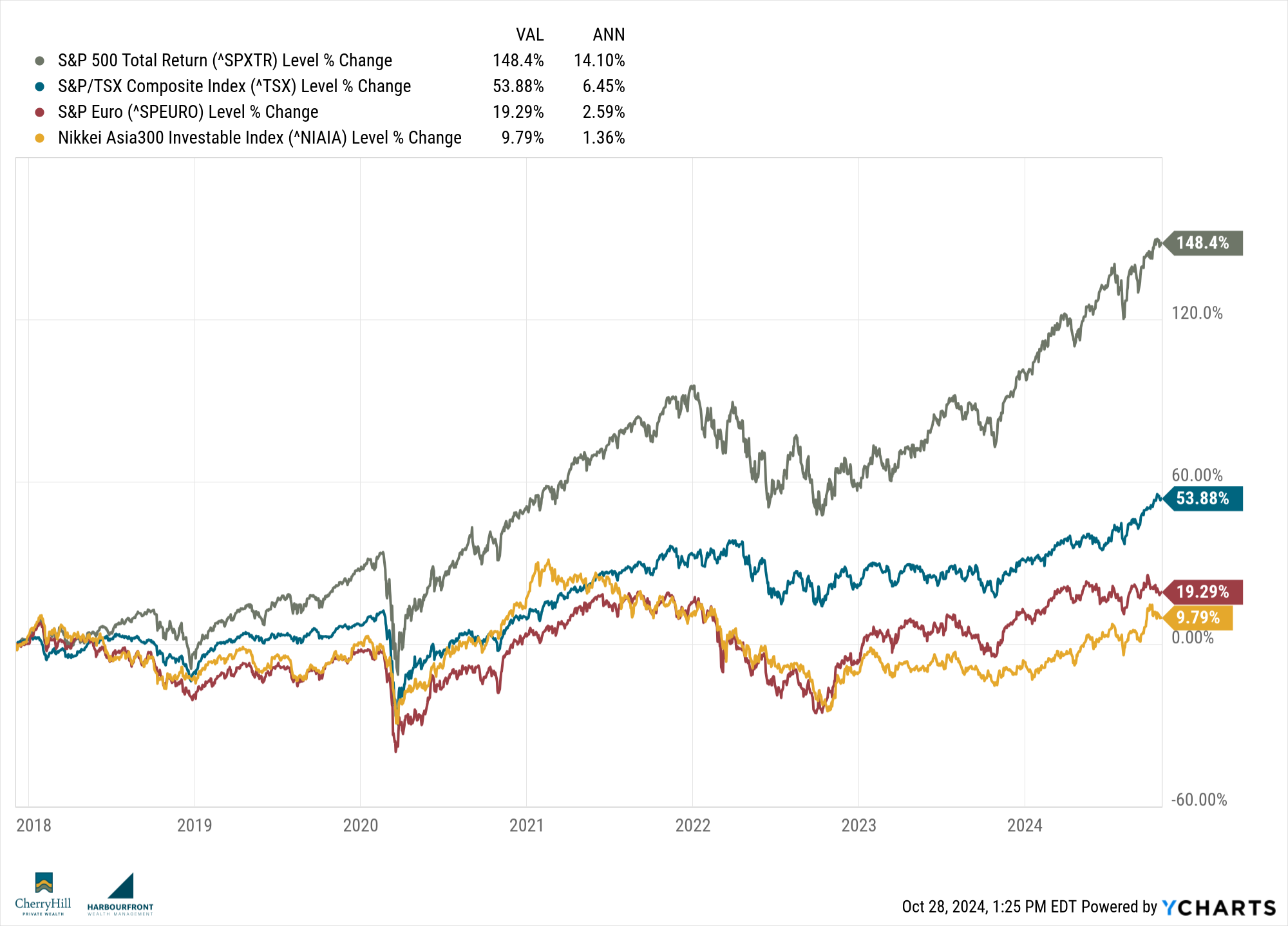

History shows us how forecasts can go awry. Just think back to the years following the 2008 crisis, when many analysts expected only modest equity returns. Instead, a prolonged bull market ensued, driven by favourable monetary policy and corporate earnings growth that outperformed expectations. Likewise, bond markets have defied expectations at times, particularly as central banks pursued unconventional policies that extended the low-yield environment much longer than anticipated.

Goldman Sachs, who is also predicting a 3% rate of return on the S&P 500 also does not have a great track record. Over the past five years, their year-end forecasts for the S&P 500 have been off by at least 10%, with the median prediction falling 14% short. This is not unique to Goldman or JP Morgan, however, as a study examining Wall Street predictions found that out of 6,627 forecasts, only 48% were correct.

The key takeaway here is diversification and adaptability. Forecasts can provide guidance and inform strategy, but they shouldn’t dictate every decision. Whether a firm like JP Morgan projects 3% or BlackRock expects 6%, the importance lies in maintaining a balanced approach that can weather both upside and downside surprises over the long term.

If you want to check out the forecasts, you can find them all here:

Market Minute

According to Bloomberg, “Financial markets are heading for a pivotal two-week stretch.” What do they mean by this? Well, the next couple weeks will see earnings reports from the big tech companies, jobs data, a Federal Reserve meeting, Chinese policy and Treasury market announcements… oh, ya, and there’s a US presidential election coming up.

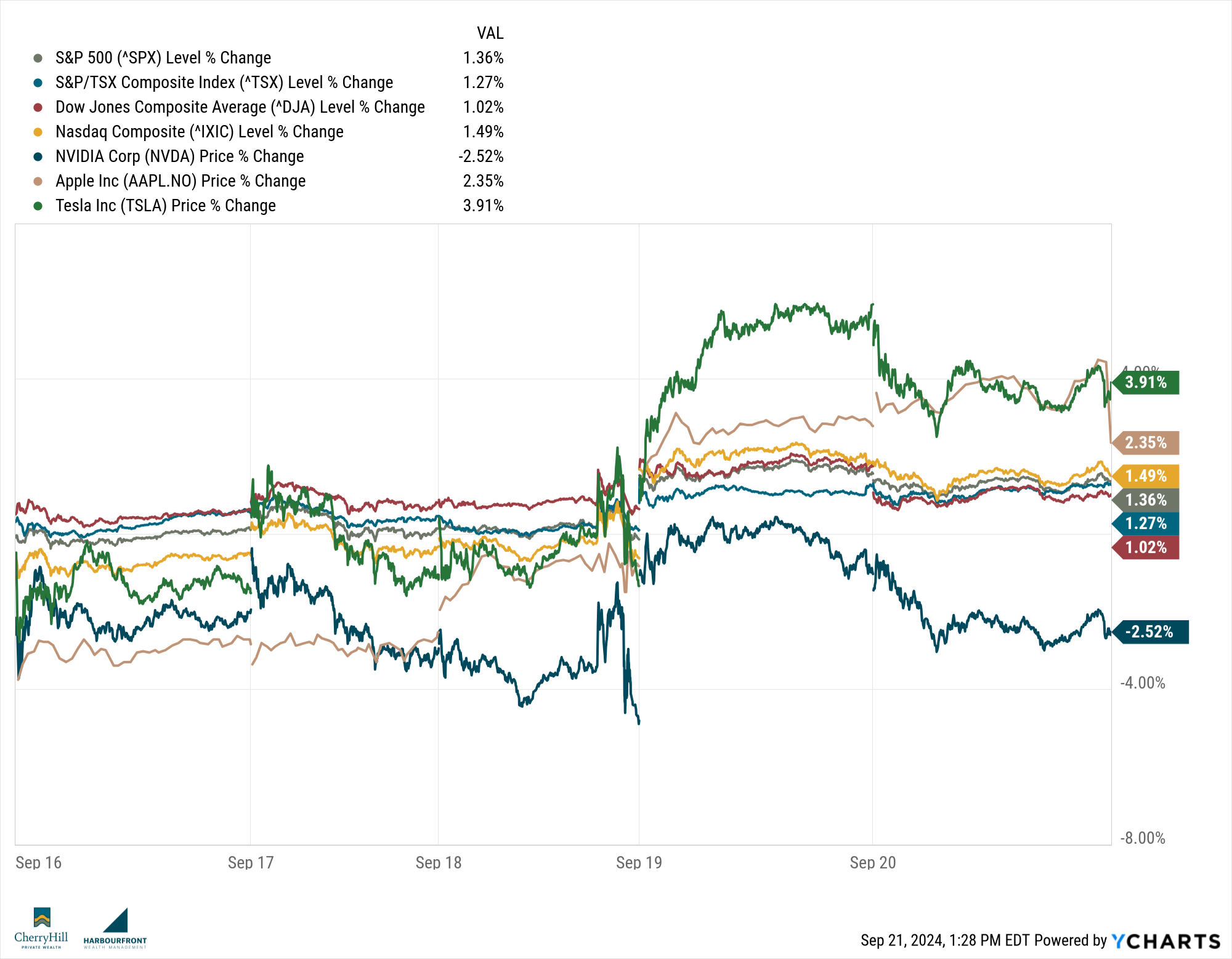

Last week, major markets were mixed, with a focus on earnings reports and investor reactions to economic data. The Nasdaq saw its fifth consecutive day of gains, driven by tech stocks and optimism in the AI space, particularly around Nvidia, whose shares continued to rally due to high demand for its AI chips. Nvidia is approaching record highs and remains a key player in driving tech momentum.

On the other hand, the S&P 500 was more volatile, largely due to weak earnings from industrial giants. Genuine Parts Company saw a sharp decline after missing profit expectations and lowering its outlook for the year, primarily due to weakness in its European and industrial businesses. GE Aerospace also disappointed investors, with a significant drop in its stock price following weaker-than-expected revenue from its commercial engine division, despite overall strong earnings.

In the auto industry, General Motors had a standout week, with its shares soaring after reporting better-than-expected third-quarter results and raising its profit guidance for the year. Strong pricing, improved EV performance, and cost controls helped the company beat expectations, leading to a surge in its stock price to levels not seen since early 2022.

Overall, tech stocks continued to push higher, but weakness in industrials created a more mixed picture across broader indices.

The Lighter Side

Halloween has evolved into the second largest holiday for spending money in North America. Americans spend over $10 billion on costumes, candy, and decorations each year. I scoured the internet to find you some of the weirdest or least known facts that I know you’re going to want to share with your friends and family!

- **Halloween’s Origins: **Like all great origin stories, Halloween dates back over 2,000 years to the Celtic festival of Samhain. The Celts believed that on the night of October 31, the boundary between the living and dead blurred, allowing spirits to return to Earth. People would light bonfires and wear costumes to ward off ghosts. Historical documents have revealed that there were, however, fewer Spiderman costumes at the time.

- Trick-or-Treating: Maybe the weirdest Halloween ritual is going door-to-door asking for candy from strangers. This tradition has origins in the medieval European practice of “souling” and “guising”. On All Souls’ Day, poor people would go door to door, offering prayers for the dead in exchange for food. In Scotland and Ireland, children would dress up and go house to house, performing songs or jokes in exchange for treats.

- **The Largest Pumpkin: **The largest pumpkin ever carved weighed a massive 2,350 pounds and was transformed into an intricate and spooky “zombie-themed” display. The artist, who set the record in 2021, turned the enormous gourd into a haunting masterpiece, complete with detailed, creepy faces and scenes that depicted zombies rising from the pumpkin. This unique carving added to the excitement surrounding pumpkin-carving records each Halloween season!

What are some of the weirdest, spookiest, or most interesting things you’ve heard about Halloween? Do you have any weird or fun traditions that you do or did?

The CHPW Team

The Presidential elections are fast approaching and looks to come down to the wire. Every four years we find ourselves having deep conversations with our clients, friends, and family about what happens to the investments “if”…

With the help from our friends over at YCharts, we have the answers for you! They provided us with the tools to look back on what has happened historically if the Democrats or Republicans won. Adrian and I have a candid discussion on all things election and your investments in this week’s podcast. you can check it all out here.

Until next week, happy investing!

Trevor