Do You Own Mutual Funds, ETFs, or Individual Stocks: Should You?

Fall is here - the leaves are turning colours, the salmon are heading upstream, the Blue Jays are golfing, and all other major sports are in full swing. It’s also my favourite time of year to get out and enjoy nature - but after checking out what we have for you this week, of course!

In today’s email:

- Can I reach my goals more efficiently with ETFs, Stocks, or Mutual Funds?

- Our Portfolio Managers reflect on September and what a volatile month it was for major markets.

- We also have a look back the Q3 and what the markets and your portfolios have done, while keeping an eye on the Q4.

- Canadian Thanksgiving’s history is much different than the US’s - do you know what it is?

- Interest rates are on a downward trend, so we caught up with our interest rate person to find out what’s next and how it can affect your debt.

The Scoop

As we navigate through this unpredictable financial landscape, a common question I get from clients is about the best way to invest - whether through exchange-traded funds (ETFs), mutual funds, or individual stocks. Markets continue to go up, but there are definite cracks that are starting to be exposed - how do we take advantage of the roaring market, but protect ourselves as well? There’s no one-size-fits-all answer, but understanding the pros and cons of each can help you decide which option aligns with your goals.

ETFs: The Efficient Way to Diversify

ETFs have gained significant popularity in recent years, and for good reason. They’re a convenient way to gain exposure to a wide range of assets without having to pick individual stocks. Most ETFs track an index, like the S&P 500, providing you with broad market exposure.

The Pros:

- **Low Fees: **One of the main advantages of ETFs is their low cost, especially compared to mutual funds. Since most ETFs are passively managed, their fees (expense ratios) are typically much lower.

- **Liquidity: **ETFs trade like individual stocks on the exchange, meaning you can buy or sell them at any point during the trading day. This can be helpful if you want to react quickly to market movements.

- Diversification: With just one ETF, you can diversify across dozens or even hundreds of stocks or bonds, reducing risk compared to owning individual stocks.

The Cons:

- **Market Volatility: **Because ETFs trade like stocks, their prices can fluctuate throughout the day. While this can be an advantage for traders, it may cause some investors to react emotionally during market swings.

- Less Control: Since you’re buying into a basket of assets, you don’t have control over which specific stocks or bonds are included in the ETF.

ETFs have come a long way in recent years. You can use it to passively track an index, or many now can be used to narrow in on certain sectors, geographies, or even exclude companies or sectors. There are many low-cost ETFs that can supplement a portfolio or be a low-cost, passive option. The options have exploded in recent years!

Mutual Funds: A Hands-Off Approach

Mutual funds have been around for much longer and offer a more hands-off approach for investors. These funds pool investors’ money to invest in a diversified portfolio managed by professionals. Some mutual funds are actively managed, while others track indices like ETFs.

The Pros:

- **Professional Management: **One of the main selling points of mutual funds is the active management by experienced professionals. They’re constantly adjusting the portfolio to achieve the best possible returns, which can be comforting, especially in volatile markets.

- **Diversification: **Similar to ETFs, mutual funds offer broad diversification across various assets. However, actively managed funds often have a more targeted strategy, allowing the fund manager to pick specific stocks.

- **Automatic Investing: **Mutual funds often allow for automatic contributions, making it easy to regularly invest without having to time the market.

The Cons:

- **Higher Fees: **Actively managed mutual funds tend to have higher fees than ETFs, which can eat into your returns over time.

- **Less Liquidity: **Unlike ETFs, mutual funds are priced at the end of the trading day. This means you can’t sell them in real time if you need immediate liquidity.

- **Performance Risk: **Just because a fund is actively managed doesn’t mean it will outperform a passive index fund or ETF. In fact, many actively managed mutual funds underperform their benchmarks after fees are considered.

- **Strict Mandates: **This could go in either the Pro or Con column depending on several factors. If the funds mandate is to have 30% Canadian equities, for example, the fund manager likely can’t increase or lower this percentage more than a couple points to lower market risks or take advantage of opportunities elsewhere.

There are thousands of mutual fund options in Canada alone. If you are with one of the big banks, or a mutual fund company, you don’t have to worry about all the options - they can likely only sell you their products. If you are one of the lucky ones who gets to choose the best companies, mutual funds can be a good choice. Many mutual funds are set up so you only have to hold one fund and get exposure to many sectors, geographic locations, and strategies.

Individual Stocks: Taking Control of Your Portfolio

Owning individual stocks offers the most control and flexibility. You can pick specific companies you believe in and directly benefit from their success. However, this level of control also comes with greater responsibility.

The Pros:

- **Control and Flexibility: **With individual stocks, you can build a portfolio tailored to your beliefs and values. Want to invest only in companies focusing on green energy? You can do that. Prefer companies with high dividends? No problem.

- **Potential for High Returns: **If you pick the right companies, individual stocks offer the highest potential for growth. Many of the best-performing investments over time have been individual stocks.

- **Tax Efficiency: **You have greater control over the timing of capital gains or losses, allowing for more strategic tax planning.

The Cons:

- **Risk: **With individual stocks, you’re exposed to the specific risks of that company. If the company struggles, so does your investment. Diversifying across multiple stocks can help, but it requires significant research and effort.

- **Time-Consuming: **Picking and monitoring individual stocks requires research, discipline, and time. You have to stay on top of news, earnings reports, and industry trends to make informed decisions.

- Lack of Diversification: Unless you build a large portfolio of stocks, you may not achieve the same level of diversification as with ETFs or mutual funds.

Picking stocks is not for the faint of heart. Many times by the time we hear about the “can’t lose” stock, the benefits are already priced in. We can also fall in love with our stock pick and make poor decisions. A lot of emotion can go into picking a company that is going to “take off” and humans can have a bias towards things they own (this goes for many aspects of life). Having the discipline to make tough decisions on when to buy and sell can have major impacts if done incorrectly.

Which One is Right for You?

Choosing between ETFs, mutual funds, and individual stocks depends on your investment style, risk tolerance, and time commitment. ETFs and mutual funds offer a more diversified and hands-off approach, while individual stocks give you greater control but require more time and risk management.

The great thing is - you don’t have to choose.

Many of our portfolios, including the ones managed by our Watermark team, hold a combination of mutual funds, ETFs, and individual stocks and bonds. Creating a portfolio that is low-cost, diversified, includes downside protection, but also top-tier gains can be possible with the right mix.

If you’re unsure which strategy is right for you, let’s discuss your goals, risk tolerance, and how each option can fit into your broader financial plan. Remember, the right choice today might change as your financial situation evolves.

Market Minute

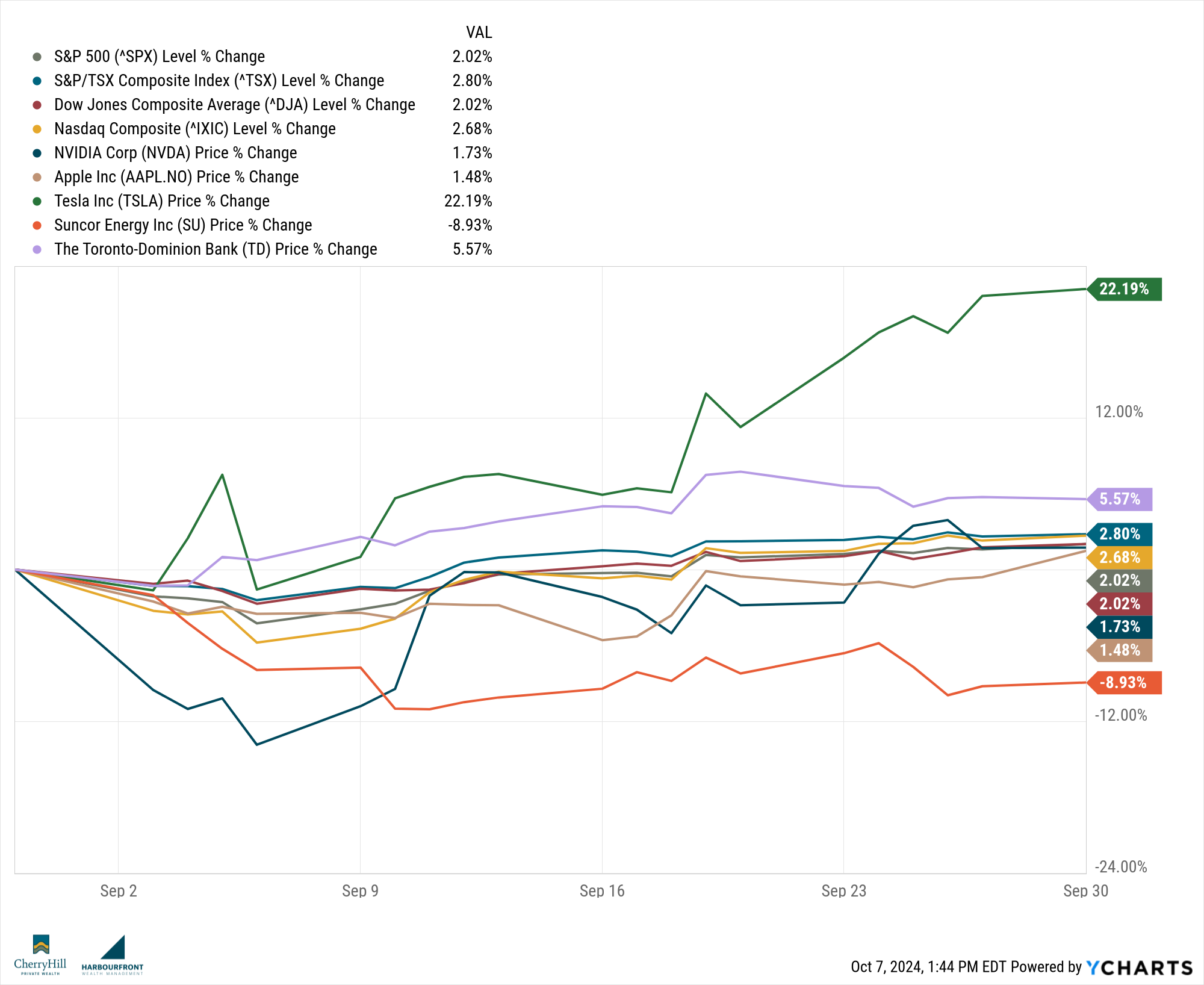

September was quite the month for the Canadian and US stock markets! Our Watermark Portfolio team just released the commentary for September and you can check it out here.

In this month’s commentary you can find more on some of these key points:

Market Review in Minutes

· Global stock markets had a volatile month. The S&P 500 (in CAD) fell nearly 4% earlier in the month but rallied back to finish the month higher by +2.38%. The S&P/TSX Composite ended September higher by +3.15%.

· The Canadian Universe Bond posted its fifth consecutive monthly gain, ending slightly higher by +1.90%.

· Crude oil fell another 7.31% in September. The US Dollar appreciated by +0.24%. Gold logged another strong month, ending +5.21% higher.

Notable Monthly Highlights/Economic Data

· The US Federal Reserve cut interest rates by 0.50%.

· The Bank of Canada cut interest rates by 0.25%.

· China announced its largest monetary stimulus since pandemic to meet its growth target and stabilize its economy.

· European Central Bank cut its deposit facility rate (the rate used mainly to steer monetary policy) by 0.25%.

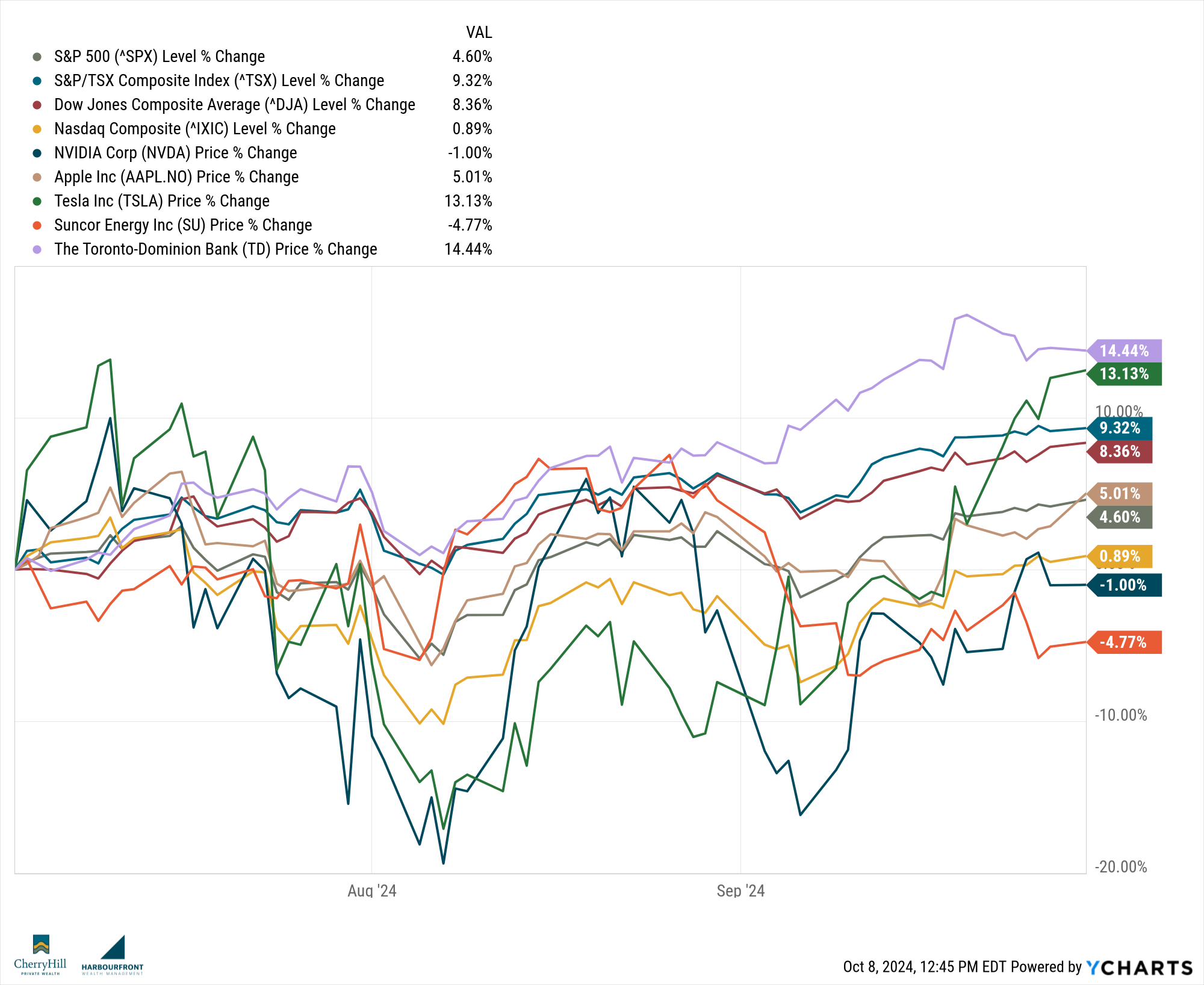

They also released the third quarter commentary, which I have included below:

Market Highlights

The third quarter of 2024 was eventful as global interest rate cuts dominated headlines and volatility picked up ahead of the election. Despite huge swings during the quarter, the equity markets ended higher; the S&P 500 (in CAD) gained +4.43%, and the S&P/TSX Composite gained +10.54%. In addition, the Canadian Universe Bond Index rose +4.66% during the quarter as interest rates fell.

Major Themes and Events in Q3 2024

- Major central banks cut key policy interest rates: Canadian and European central banks continued cutting their interest rates as inflation eased, with Canada’s target rate now sitting at 4.25% and Europe’s deposit facility rate sitting at 3.5%. In the US, the US Federal Reserve made its first interest rate cut in September at 0.50%, with a target of 4.75%-5.00% for their federal funds rate.

- Rise in volatility: During the quarter, public equity markets saw large volatility swings, with levels not seen since the pandemic, as an unexpected interest rate increase in Japan caught market participants off guard. In addition, equity markets have historically been more volatile during the months immediately ahead of the presidential election. Despite the volatility, the S&P 500 held key technical levels, as buyers continue to step in and “buy the dips.”

- Market breadth improved: For Q3 2024, we saw some profit-taking from the mega cap tech companies with proceeds rotating into other sectors, improving market breadth. This helped stocks at home, with the S&P/TSX Composite outperforming the S&P 500 as financials and commodity miners outperformed the information technology sector.

- China tries to save its struggling economy: In Asia, China’s property sector continues to be a main concern; thus, the Chinese central bank announced its biggest stimulus package since the pandemic to try and stabilize its economy and provide a boost to future growth.

**Portfolio Positioning **

We continue to keep the portfolios overweight to equity (including private real estate) so you can participate in the market run up, as global central banks continue to reduce interest rates to stimulate growth. Early in the quarter, we took profits on the iShares Canadian Short Term Corporate ETF in the more conservative portfolios to lengthen the maturity of the debt on the public fixed income portion of your portfolio. In response to the US Federal Reserve’s interest rate cut of 0.50%, we trimmed our defensive equity holding and moved those proceeds into a pure play US value ETF that buys quality companies that are growing their earnings and trade at attractive valuations. Our investment strategy remains focused on long-term value creation through risk management, diversification, and identifying growth opportunities when applicable. We continue to maintain diversified portfolios that can weather market fluctuations while capturing upside potential by investing into high quality businesses at reasonable valuations that are growing their earnings.

Did you know?

Historically, the S&P 500 has averaged a negative return three months after the first rate cut. During recessionary periods, the returns have been negative three months later after the first rate cut. However, during non-recessionary periods, the S&P 500 has performed well, ending higher both six and twelve months later.

Our team also made some trades this week that you can find here.

The Lighter Side

With Thanksgiving quickly approaching, we wanted to thank all of you who open up our newsletter each week. We are extremely grateful for those of you who trust us with their family’s financial wellbeing, and all of you who make doing what we do worthwhile.

The Canadian Thanksgiving history and tradition often gets overshadowed and confused with the American Thanksgiving, but the histories are very different.

The first recorded “Canadian” Thanksgiving dates back to 1578, over 40 year prior to the Pilgrims’ feast with the Wampanoag people. English explorer Martin Frobisher held a ceremony in Newfoundland giving thanks for safe passage across the Atlantic, which is largely considered the first Canadian Thanksgiving.

In the early 17th century, French settlers celebrated harvest season by giving thanks and hosting large feasts and sharing meals.

Out of this new tradition, the Order of Good Cheer was created, which was a social gathering of settlers and Indigenous people to share food and entertain each other. This would be the basis for what we now celebrate as Thanksgiving.

Unlike our neighbours to the South, Canadian Thanksgiving is not based on a certain date, but is a celebration of the season’s bounty and an opportunity to gather with families and friends to enjoy a meal. Born out of European settlers and Indigenous people’s traditions of celebrating the harvest, we have created something that is uniquely Canadian.

The CHPW Team

Interest rates are finally starting to decrease after a historic increase over the past couple of years. As more and more mortgages are coming up for renewal, Canadians have been waiting for this moment. On the heals of the most recent decrease, the Canadian government also made some changes to the mortgage rules.

We had the opportunity to speak with mortgage expert, Tania Labonte to talk about these changes, as well as, the rise of “severe delinquencies” in Ontario, which has surpassed $1.3B. Whether or not you have a mortgage, you aren’t going to want to miss this episode as we talk all things interest rates and mortgages with one of the industry’s best.

Until next week, happy investing!

Trevor