Does the Fed Rate Cut Make Sense?

It happened, it finally happened! The US made the bold decision to cut interest rates by 1/2%. This week we take a look at why they did this and what it could mean for you and your investments.

In today’s email:

- The Feds cut rates and investors loved it! Rate cuts can signal a weakening economy, so why did equities take off?

- Breaking News: Nvidia had another great week.. but so did some defensive sectors - what’s going on in the markets?

- Is coffee about to become a drink only for the wealthy?

- A story about what a financial plan could do for you, even if you think you’re going to be just fine.

- Rates are are going down, which means your fixed income is about to suffer. Are there any options for the 40% of your portfolio?

The Scoop

The financial headlines this week were dominated by one major event—the Federal Reserve’s decision to cut interest rates by 50 basis points. As expected, the markets responded with enthusiasm, sending stock prices soaring. But as we celebrate the gains in our portfolios, it’s essential to take a moment to understand what’s driving both the Fed’s actions and the market’s reaction, and why this moment represents a delicate balancing act between optimism and caution.

Why Did the Fed Cut Rates?

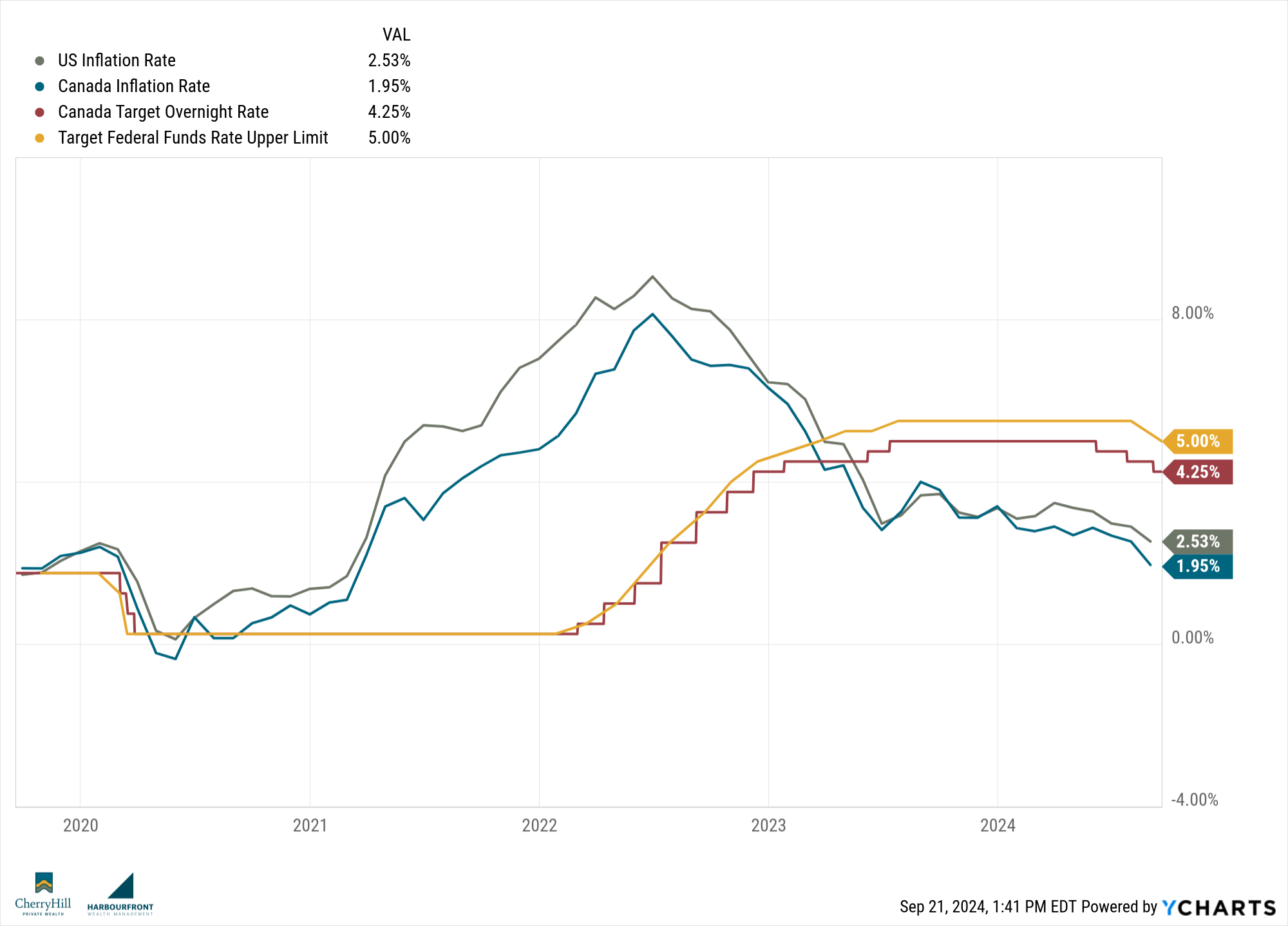

The Fed’s decision to reduce rates this week wasn’t exactly out of the blue, though the magnitude—50 basis points—certainly grabbed attention. It’s important to understand that central banks don’t make decisions like this lightly. The move signals their growing concern over underlying weakness in the economy, particularly around slowing consumer spending, softening employment data, and the cooling housing market. Inflation has come down considerably, but this cut shows the Fed is more focused on avoiding a deeper downturn.

Simply put, the Fed is attempting to provide a cushion as economic activity decelerates, aiming to keep liquidity flowing and avoid a more severe slowdown. Lowering interest rates makes borrowing cheaper, which can spur businesses to invest and consumers to spend, stimulating economic activity. However, it also signals that they are seeing cracks in the foundation of the economy, especially if they feel the need to make such a sharp cut.

Why Did Markets Rally?

On the surface, a rate cut is good news for markets. Cheaper borrowing costs benefit companies by lowering their interest payments, improving profitability, and making growth projects more feasible. For consumers, lower rates can encourage spending, which is good for corporate revenues. These are just a few reasons why investors were quick to bid up stock prices following the announcement.

Investors also see rate cuts as a reason to take more risk. With lower yields in the bond market, equities become more attractive, as they offer better potential returns in a lower-rate environment. There’s a sense that “there is no alternative” (TINA), so stocks tend to rally after rate reductions.

But here’s where it gets tricky.

Rising Stock Prices and a Weakening Economy

There’s a bit of a dichotomy we need to address. The very reasons the Fed felt compelled to cut rates—slowing growth, weaker employment numbers, and soft consumer demand—are not exactly the ingredients for a robust economic future. Yet, the stock market’s reaction would make you think we’re in for a boom.

So, why the disconnect?

Markets are forward-looking. Investors are betting that lower rates will fuel growth down the road, and that companies will find ways to thrive in a low-interest-rate environment. But at the same time, the Fed is acknowledging that the economy is not as strong as it once seemed. In other words, while stock prices rise, the economic fundamentals are signaling something more concerning.

This divergence creates a potential risk. If the economic data continues to weaken, there may come a point where rate cuts alone won’t be enough to lift markets. In that case, the rosy optimism we’re seeing today could shift as investors confront the reality that lower rates are a Band-Aid, not a cure, for a weakening economy.

What Does This Mean for Investors?

As investors, we’re in a tricky position. It’s easy to be swept up in the market’s enthusiasm, but it’s critical to remain grounded in the bigger picture. The Fed’s rate cut is a tool to stabilize the economy, but it’s also a signal that the outlook isn’t as positive as we’d like it to be. This is a good time to reassess portfolios, ensure proper diversification, and focus on quality investments that can withstand slower growth.

In times like these, balancing optimism with caution is key. Enjoy the market’s rally, but remember: we’re not out of the woods yet.

Market Minute

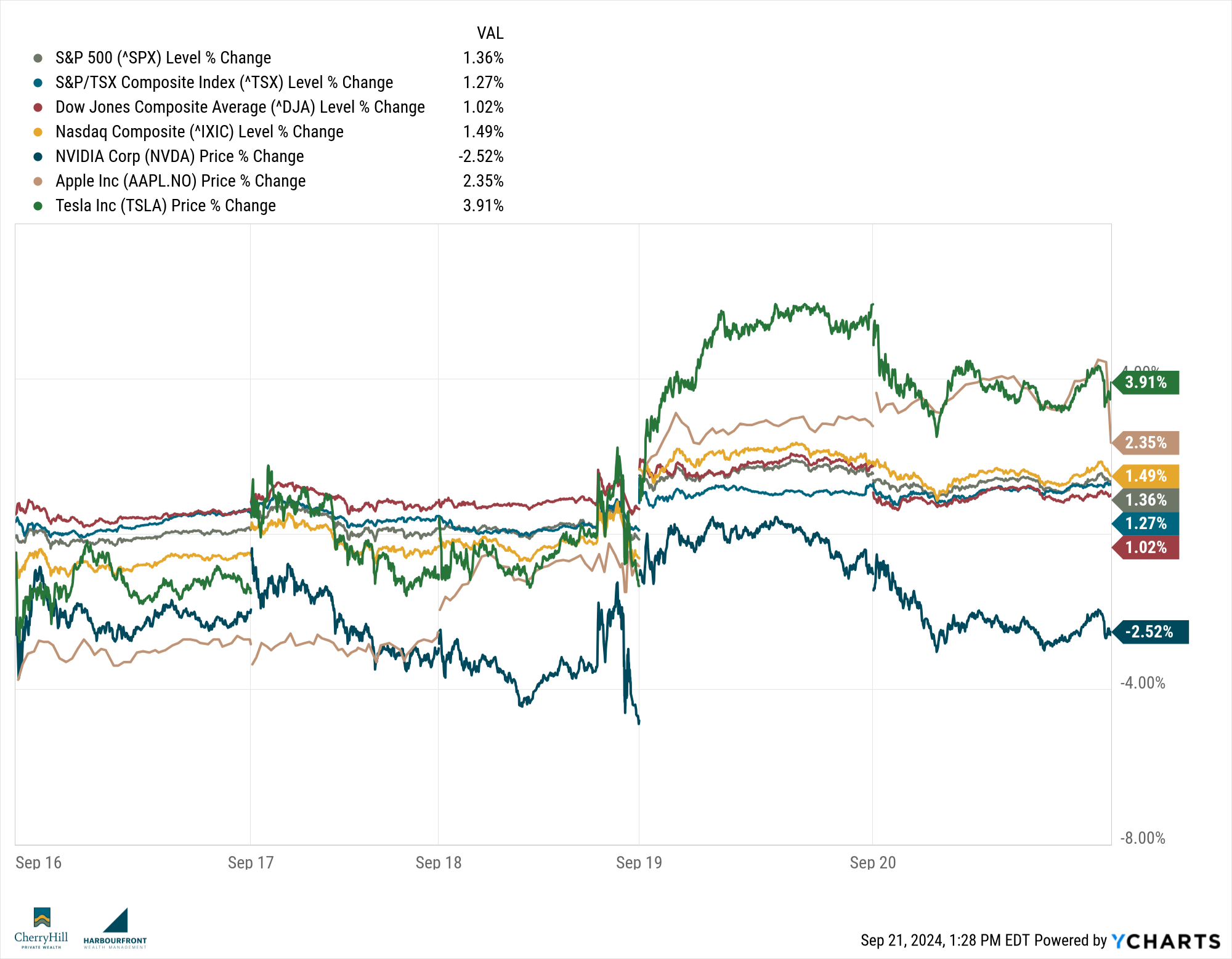

Last week, the US and Canadian markets posted strong gains, fuelled by the 50 bps rate cut by the Federal Reserve. Investors interpreted the cuts as a sign of future support for growth, which helped boost sentiment despite continued concerns over slower economic data.

Here’s what happened:

- **Technology Stocks: **Companies like Nvidia and Apple continued to push the sector higher, again posting large gains. Lower interest rates will reduce their borrowing costs, making future earnings more attractive.

- Energy Stocks: This sector has seen much volatility recently and that trend continued last week. Weakening demand, supply constraints, and geopolitical issues are causing investors to think twice before investing in many of these companies.

- **Shift Towards Defensive: **Consumer staples and health care are areas in which investors gravitate towards durning times of uncertainty. We saw this trend continue last week as companies like Procter & Gamble and Johnson & Johnson posted modest gains.

- **Precious Metals: **One standout in the Canadian markets last week were around companies like Barrick Gold and Wheaton Precious Metals, which both saw positive gains. With ongoing global uncertainty, gold and silver prices remained elevated.

Trends to Watch

- **Inflation Data: **This continues to headline the “what we’re watching” news. With the reduction in the Fed rates, Canada might be tempted to reduce rates quicker. Recent inflation data, in Canada, has inflation falling to the 2% benchmark. There is now concern that inflation will continue to fall, which could put Canada in a precarious situation.

- **Earnings Reports from Major Realtors: **We have seen many of the earning reports from the tech companies, but companies like Costco, Walmart, and Lululemon are coming this week. This will give us a better perspective on consumer demand and a good view of the strength of the economy.

- Commodities and Safe-Haven Assets: With economic uncertainty looming, demand for gold and silver remain strong. Depending on some of the earning reports, as well as other economic data, this sector could see a boost this week.

The Lighter Side

This might be my saddest Lighter Side yet. Coffee prices are on the rise around the world and it’s more than just a temporary trend.

There are a couple things at play here and both have a massive impact on the costs.

The first is that there has been a surge in global demand, which has come primarily from emerging markets in Asia, Africa, and Latin America. Countries like China and South Korea historically leaned towards tea consumption, but in recent years the café culture has found its footing. Additionally, younger generations, particularly Millennials (always the Millennials fault) and Gen Z have increased the demand for coffee experiences. No longer is coffee just a morning pick-me-up; the demand is now for specialty brews, artisinal roasting, and ethnically sourced beans.

The other major factor is the change in climate in many of the growing regions. Coffee is highly sensitive to changes in weather, particularly in key coffee-growing regions like Brazil, Columbia, and Vietnam. Coffee plants, especially the popular Arabica variety, are becoming more susceptible to diseases and pest due to changing environmental conditions.

These realities are leading to efforts to develop and find more resilient coffee varieties or even lab-grown alternatives to secure the future of one of the world’s favourite beverages.

The CHPW Team

This past week was a busy one for the team at Cherry Hill. One of my favourite parts of this business is being able to take all the financial information from my clients and go deep with an analysis. It can be sobering when a client feels they’re better off than they are, but it can also be exhilarating when the opposite is true.

This past week I was able to present a Financial Plan to a client of mine who is thinking about winding down his business. There are so many scenarios to consider and we crash tested many alternatives. He had had an idea in his mind of “his number” and also, it turns out, had limited his dreams for his retirement. We were able to increase his vacation spending, add a bit to a vacation rental he’d been contemplating and still make sure he was going to be ok.

Financial Plans aren’t just for determining if you’re going to be “ok” in retirement, but also to make sure that you don’t under-live your life to the fullest. Whether we’re able to figure out a way to increase your spending or maybe make some changes in your working years so you can the most fulfilling retirement, knowing where you stand is paramount to living your best life.

Let us know when you want to go through this process and find out how you can life your best financial life!

Across Our Desks

With interest rates on the decline, it can be great for mortgages and lending, but the fixed income market tends to suffer. Prior to the increases in interest rates that started a couple years ago, traditional fixed income had struggled to keep up with inflation, many times failing to do so. These past couple years GICs and HISAs have been more attractive as “risk-free” investments. As rates are declining we’re seeing these rates come down significantly. A balanced portfolio should have about 40-50% of their portfolio in this asset class.

So how to we get some yield from such a big part of our portfolio?

We have some in-house solutions as you’re likely well aware of, but what I was looking at this week was the Clifton Blake Mortgage Income Fund. This fund has been around since 2015 and targets properties around the GTA. There are two options as the investor, one with a reinvested dividend (DRIP), and the other with the dividends paid in cash. The average returns for the fund, since inception is 10.87% for the DRIP fund and has not had a year below 7.5%. What really struck me with this fund in particular is that they have an average credit score of their borrowers of 748.

Clifton Blake is one of the providers we have access to and some of their holdings can be found in our Watermark Portfolios. There are several other companies that offer high returns for your fixed income side that might be worth exploring.

Until next week, happy investing!

Trevor