Interest Rates are Finally Trending Down!

As we near the close of July, we have a scorcher of a newsletter for you today!

In today’s email:

- The Bank of Canada lowered interest rates for the second consecutive month, but are the savings being passed on to you?

- Tech stocks got beat up again last week, is the AI craze over?

- We would never know who ate the most Big Macs (it was Donald Gorske and he ate 30,000) ever if it wasn’t for this didn’t happen 70 years ago.

- Don’t forget to check out the new podcast!

The Scoop

Interest Rate Reductions: Relief or Too Little, Too Late?

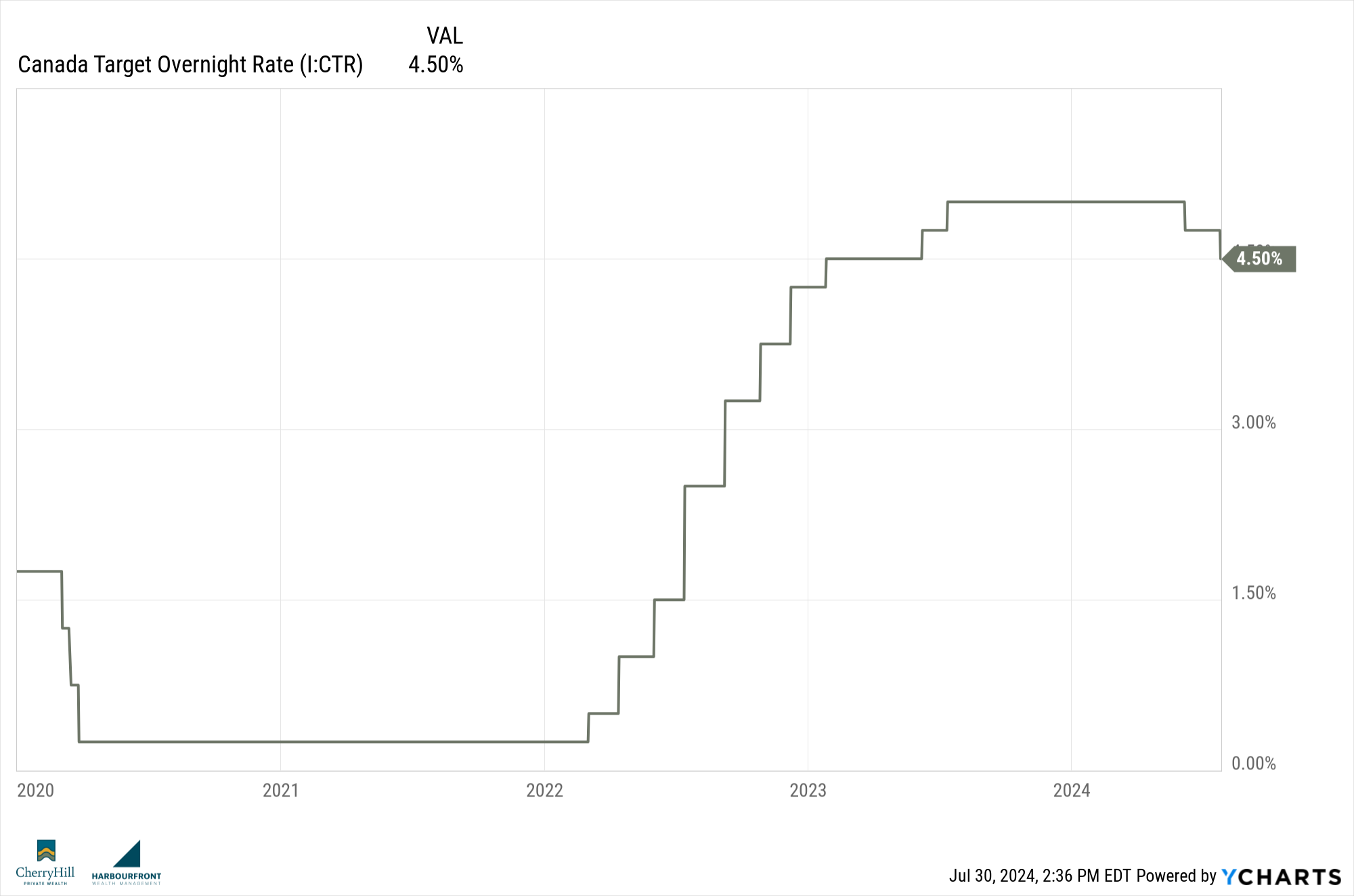

Last week, the Bank of Canada (BoC) reduced its lending rate by another 25 bps, bringing the current rate down to 4.5%. This marks a second consecutive month of rate cuts, aiming to provide some relief to Canadian borrowers. But is it enough?

The Current Situation

The BoC’s decision to lower rates, reducing them from a recent high of 5% to 4.5%, comes amid declining inflation trends and slowing economic and labor growth. Canada has been experiencing a “soft” economy, with much of the GDP growth attributed to population increases rather than economic expansion. The BoC faces the challenging task of managing post-pandemic inflation alongside federal policies that have increased immigration, contributing to inflationary pressures.

According to the recent Monetary Policy Report (MPR), the BoC seems to have shifted focus away from urging the federal government to adjust immigration levels to manage inflation. There is potential for further rate cuts if inflation continues to trend downward according to the report.

Impact on Canadians

The recent 50 basis point reduction in rates should theoretically ease borrowing pressures. However, Canada’s economy, which heavily relies on consumer debt, may not see significant benefits. The country is grappling with record-high credit card debt, now totaling approximately $91.5 billion. The delinquency rate has also surged, with a year-over-year increase of 17.27%, bringing the total to around $2.67 billion.

Unlike in the U.S., where credit card rates are tied to the prime lending rate, Canadian credit card rates are set independently by lenders. Therefore, the BoC’s rate cuts do not directly impact credit card interest rates, potentially allowing banks to benefit from a wider spread on earnings from credit card debt.

Mortgage and Housing Costs

Mortgages and rent are major expenditures for Canadian households. While variable rate mortgages (VRMs) may benefit from the BoC’s rate cuts, fixed rate mortgages (FRMs) are more closely tied to government bond yields. These yields have increased significantly since 2020, rising from 0.43% to approximately 3.34% as of late July 2024.

As a result, even with the BoC’s reductions, many Canadians could face higher borrowing costs for mortgages. For example, a homeowner with a $500,000 mortgage, initially locked in at 2.04% in 2021, might now face rates around 4.84%, potentially increasing their monthly payments by about $750.

Vehicle Financing

Similarly, vehicle lease and finance rates have not seen reductions, despite the BoC’s actions. Many Canadians renewing their leases or financing agreements may face higher monthly payments. Personally, as my vehicle lease approaches its end, I anticipate an increase of approximately $300 per month for a new lease.

Conclusion

While the BoC’s recent rate cuts offer some relief, they may come too late for many Canadians who are already feeling the squeeze of high credit card debt, rising mortgage costs, and increased vehicle expenses. The economic landscape remains challenging, and the effects of these reductions on individual finances may be limited.

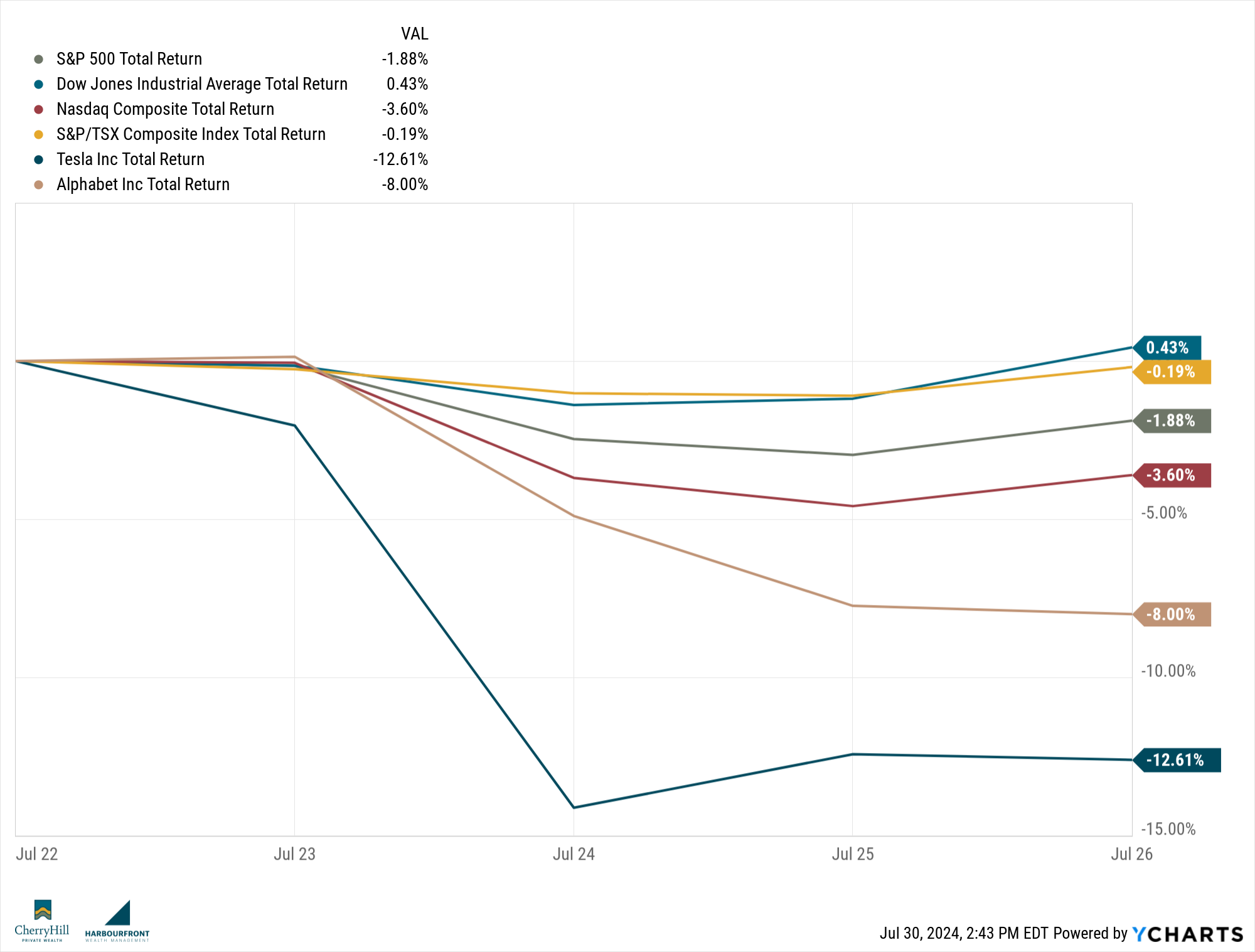

Market Minute

Last week saw the downward trend continue for most of the major North American markets.

In Canada, the TSX saw a slight decline, partly due to the Bank of Canada’s decision to lower its policy rate to 4.5%, marking its second consecutive rate cut. This easing aims to support domestic growth amid softer inflation and economic conditions.

In the U.S., the markets were marked by volatility, with the S&P 500 and Nasdaq facing declines due to underwhelming earnings from major tech companies like Tesla and Alphabet. Despite this, the U.S. GDP report showed stronger-than-expected growth at 2.8% for Q2, highlighting resilience in consumer spending. The 10-year U.S. Treasury yield remained around 4.15%, while the 10-year Canadian bond yield was approximately 3.34%. These developments suggest a cautious but ongoing economic expansion, with markets adjusting to mixed signals from corporate earnings and economic data.

Trends to Watch

- Central Bank Policies: We will continue to watch for potential rate cuts and policy changes from the Bank of Canada and the US Federal Reserve, especially as inflation and economic data evolve.

- Corporate Earnings: We have seen some underwhelming earnings reports from some of the major tech companies. This will continue to impact market sentiment.

- Geopolitical Developments: Global trade tensions are evolving, especially between major economies like the US and China.

The Lighter Side

We all know the Guinness World Records and I’m sure we’ve heard some really strange records that are now a part of this iconic book. Records like longest fingernails (it’s 8.65m) and largest collection of rubber ducks (9,000) might not even be the weirdest records in this collection.

But it was on July 29, 1954 that Sir Hugh Beaver, managing director of Guinness Breweries, conceived the idea of this record book. The idea came when Sir Beaver and his friends were debating which game bird was the fastest.

After much debate they found that the reference books couldn’t provide the definitive answers to such questions. Sir Beaver hired twin brothers Norris and Ross McWhirter, who were fact-finding researchers to compile the first edition, which was published in August 1955. It quickly became a best-seller and has been published yearly since.

The CHPW Team

In case you missed it, last week we also released our 3rd podcast episode! You can check out the full episode here as we talk to fitness expert, Raymond Lambert. He works with the 40+ crowd and is an expert at keep you fit and healthy all the way through retirement!

Until next week, happy investing!

Trevor