If a Recession Happens at This Point, it Could be Devastating

We’ve got a great, packed newsletter for you today!

In today’s email:

- At retirement we need to look at more than just average returns. We dive into one of the most important aspects of your portfolio when approaching retirement.

- Should these disappointing earning reports from the big tech companies have you running for alternatives?

- If you could have a month renamed after you, which would it be?

- Can you really get more from a company if you’re not working for that company?

The Scoop

I had an interesting conversation with a client recently about their investments, which highlighted a topic I believe is often overlooked when planning for the future.

If you’ve spoken to a financial advisor over the last couple of years, they’ve likely tried to sell you on their preferred fund or portfolio, showcasing exciting graphs and fund sheets with impressive returns. These enticing returns are designed to make you eager about the potential benefits of this new direction. They might remind you that “past performance doesn’t guarantee future performance,” but you’re already hooked—who wouldn’t be excited about the prospect of getting 15%+ returns every year?

We all know that no two years are the same when it comes to investments. We’ll have good years and not-so-good years. While building our wealth, it’s crucial to keep our eye on the long-term and not get too caught up in short-term gains and losses. But is this always the best approach?

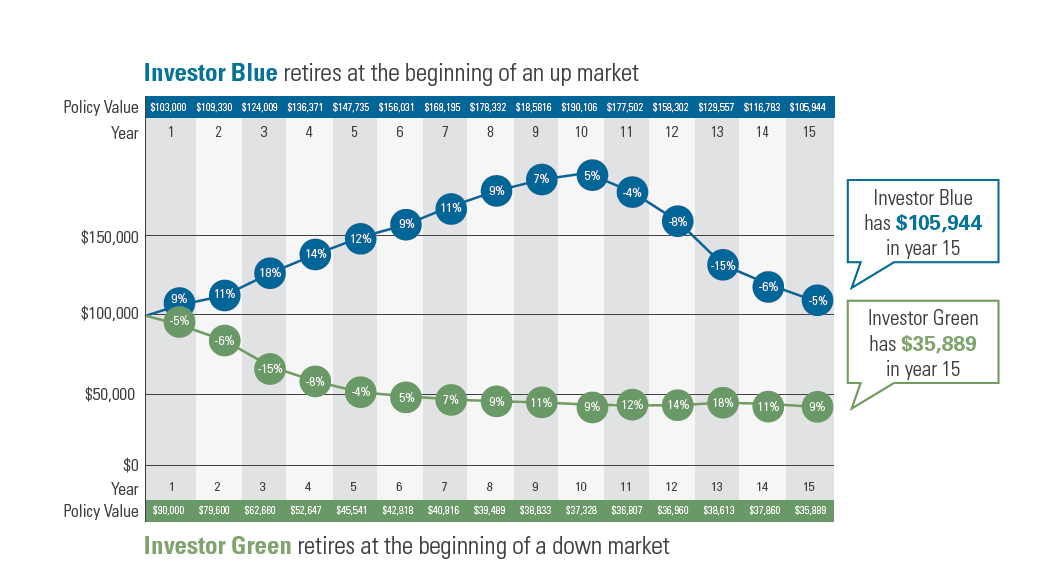

There is one instance where the short term is very important: the first few years of retirement. This concept isn’t necessarily new. There was a time when, as you neared retirement, you would reduce your risk and move from a “growth” portfolio to a more “conservative” allocation. The problem today is that we’re living longer and often spending more in retirement than we did 20-25 years ago. Unlike previous generations, it’s common now for retirees to spend a month in Australia or buy their first luxury car. I even have a client nearing retirement looking to “downsize” into a new build, their first ever.

So, how do you retire, enjoy an amazing lifestyle, and also reduce the risk in your portfolio?

The AARP Bulletin addressed this question in their July issue, offering four points to help mitigate the risk of a significant market downturn early in retirement. Their first two points focused on cash flow and understanding your budget, which a great financial plan can help with. They also discussed adjusting your investments and maintaining some “risk-free” assets.

Today, I want to focus on the investment side of the equation. Most of us don’t retire with a “worry-free” amount of investments and savings. We typically have just enough to achieve our goals but can’t afford to see our average rate of return drop from 8% to 4%. So, how do we maintain a high rate of return without sacrificing stability?

The reason why the first couple of years in retirement are so critical is that they are typically your bigger spending years, often referred to as your “Go-Go” years. If you are withdrawing an average of 4% and the markets are down by 10%, your portfolio will have shrunk by 14%. Conversely, if your portfolio grows by 8%, your portfolio would increase by 4%. This means that a few good years at the start of retirement could leave you with more money than you started with. On the flip side, a few bad years could significantly reduce your portfolio, more than it can handle.

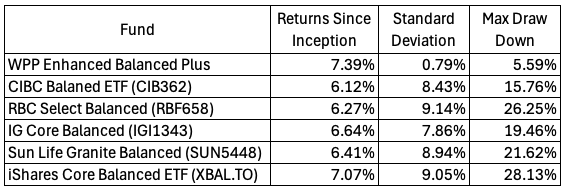

You’ve likely heard our team discuss Standard Deviation. While it might have been a snooze-inducer in high school, it’s a valuable tool for assessing risk in portfolios. It helps us understand the variability of your returns. When nearing retirement, minimizing standard deviation while still trying to maximize returns becomes crucial. This is where incorporating private asset classes and building a downside-protected portfolio can create a retirement plan that is both predictable and successful.

Although I likely wouldn’t make a change to a different advisor or firm for a 1% increase in overall returns, I would definitely think about making that change to protect my retirement and reduce the risk to my investments and family.

Market Minute

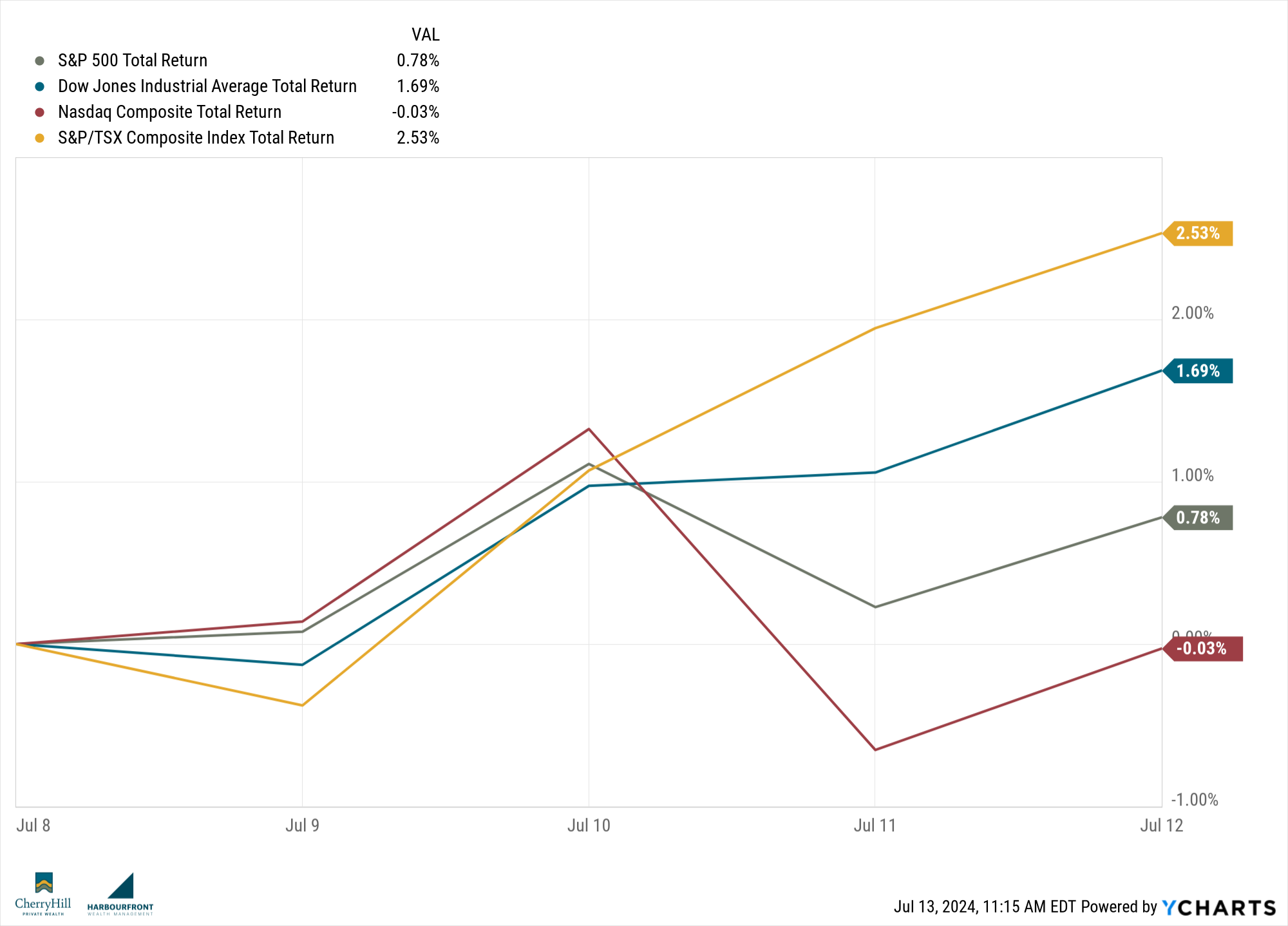

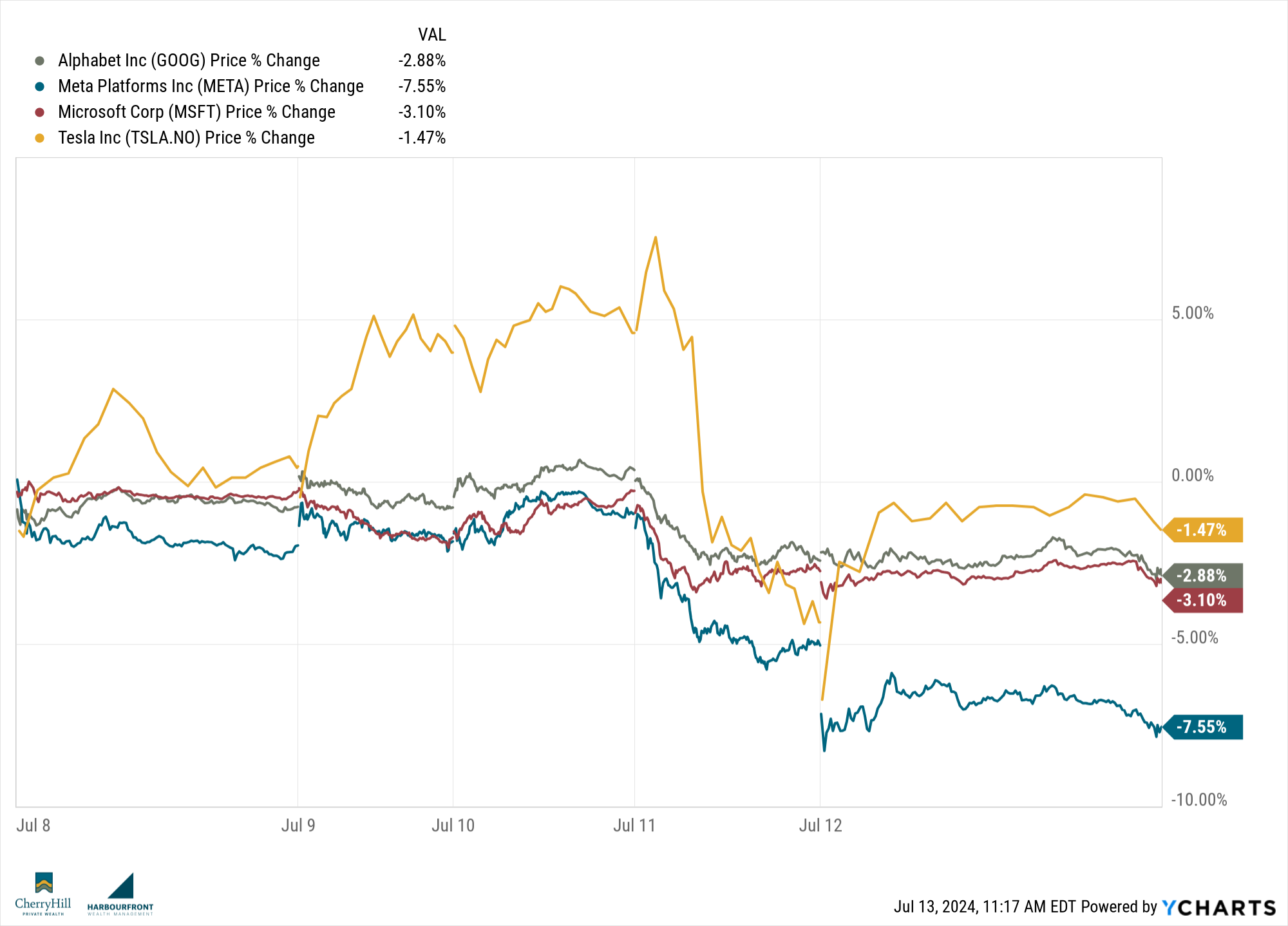

Last week turned out to once again be dominated by tech stocks. This week it was around some “disappointing” earnings.

In Canada we had a strong week, mostly due to a good performances in both the energy and financial sectors. Geopolitical tensions have caused oil prices to surge, which has been good for the Canadian exchange.

In the US we saw a week of significant volatility in both the S&P 500 and Nasdaq.

Interest rates continue to be a major factor both in Canada and South of the border. Canada has another rate decision coming on July 24, with most experts leaning towards a lowering of rates again. In the US, amidst continued inflation concerns, more rate hikes might still be on the table.

We saw significant volatility in the tech sector last week and the reactions to the earnings reports are very interesting.

Meta Platforms (Meta) had better-than-expected earnings and a 27% year-over-year increase, but the outlook for the second quarter fell short of expectations. Their forecasted revenue between $36.5 billion and $39 billion, was below the $38.24 billion estimates, which lead to a significant stock sell off.

Microsoft (MSFT) and Alphabet (GOOGL) both had seemingly positive results, but AI spending and other minor factors lead to uncertainty with investors.

Tesla (TSLA) had recently announced plans to accelerate the launch of more affordable vehicles, which had seen their stock price increase over the past several weeks. Their earnings report, however, was particularly disappointing with a 55% drop in profit and global deliveries falling well short of estimates.

Tech stocks continue to drive the US market and the volatility looks to continue to be a storyline for the foreseeable future.

The Lighter Side

Many of us think about leaving a legacy behind, which typically involves having a positive impact on our children and future generations. For the more ambitious it could involve having something named after you like a local park or creating a charitable foundation.

For Julius Caesar it was a month. When the new calendar was created, Caesar had the wonderful month of July named in his honour. It got me thinking, what month would I want named after me? I think I’d pick September as my “Trember” month. The weather is usually pretty ideal for getting out for enjoying nature, with cooler evenings around camp fires, and some final days on the water.

What month would you have named in your honour if you got to name a month after you? Send me a quick message with the month you’d choose and why you’d choose it!

The CHPW Team

Ashley is continuing to work basically around the clock bringing over clients and in our Friday morning chat she brought up something that I think surprised her. She was talking to the RBC wholesaler, who our team has got to know pretty well over the last couple years. What she realized during htis conversation was that she can continue to offer RBC funds, but now has even more options *within *RBC than she did while she was at RBC.

It’s amazing what opportunities are out there when you step outside your comfort zone!

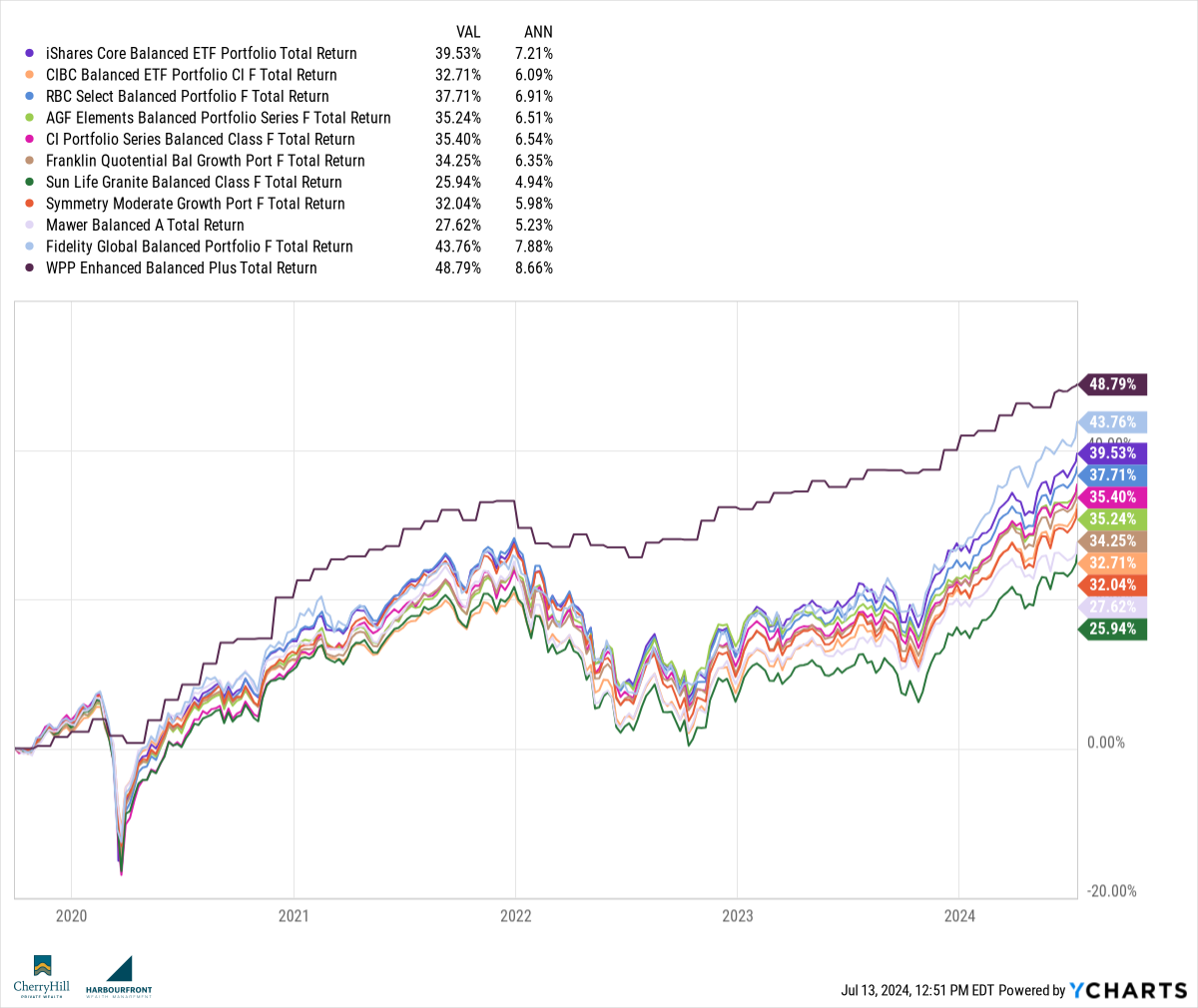

Our team also made some trades in the WPP portfolio that you can see here.

Until next week, happy investing!

Trevor