Why Do the Rich Care About Downside Protection?

Hi, !

So, it’s finally happened! The Bank of Canada has lowered its lending rate by 0.25%! This reduction is based on a combination of slowing inflation and a decelerating economy.

The shift in monetary policy comes on the heels of GDP numbers that came in softer than expected, signalling an economic slowdown. There was also an article this past week from Business Insider (here) discussing warning signs that a stock market bubble could be on the horizon.

Now, whether you believe the next bubble is imminent or not, there is something that institutional investors and family offices always consider when building a portfolio: downside protection.

As you may well know, the ultra-rich and pension funds do not like to lose money. In fact, it is one of the key principles in how they invest their funds. That’s not to say that these institutional investors just sit on their millions and don’t expect significant returns. On the contrary, they often see returns of more than 10%.

So, what exactly is “downside protection”? Should you have it? How do you get it?

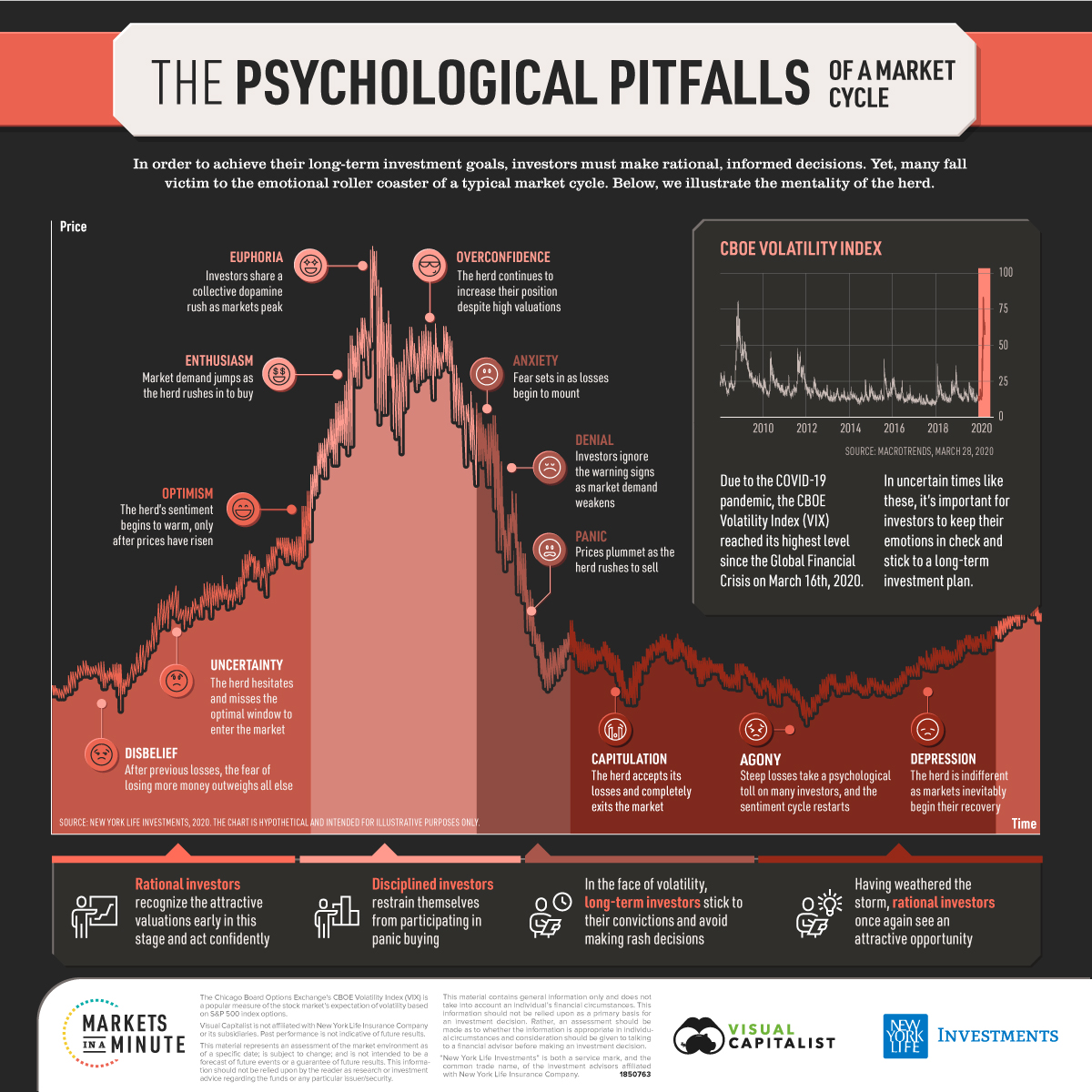

Essentially, downside protection is making sure you don’t lose your shirt when the markets go through a pullback or a bubble bursts. Sounds simple enough, doesn’t it? The problem is that most retail investors go through a cycle of greed when the markets are doing well and think it’ll stay this way forever, forgetting that we need to protect our assets.

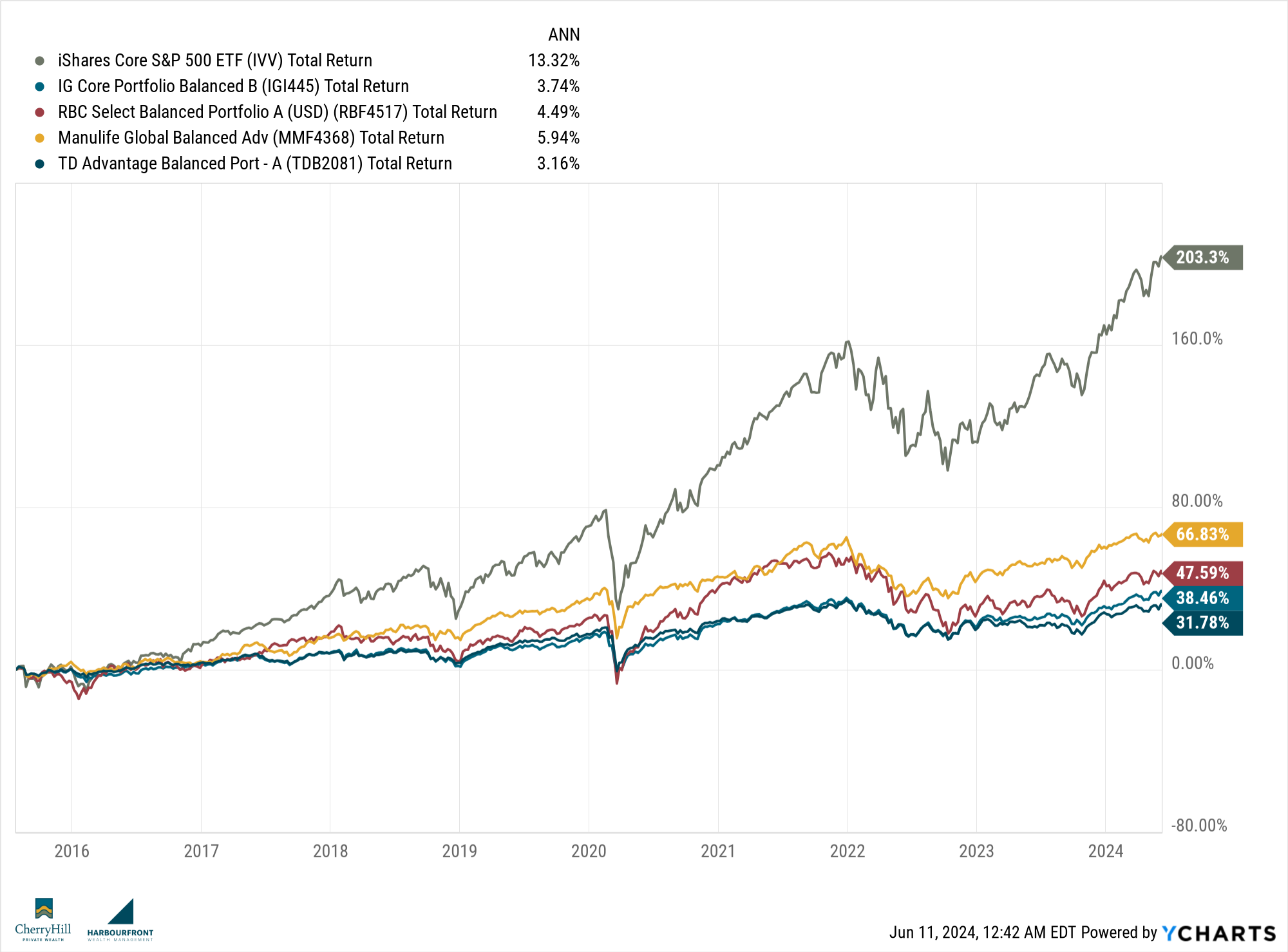

In a retail setting, such as with a bank or mutual fund company, downside protection is often provided through bonds or other fixed-income instruments. While these “safe investments” aim to preserve capital, their performance over the past decade has been modest, averaging around 2%. Even during the recent bond market uptrend with rising interest rates, returns have remained relatively low. Additionally, many fixed-income products can experience significant losses, such as -10% or greater like we saw in 2022. Although these investments can shield your portfolio from the full impact of market downturns, they often result in lower overall returns. For instance, balanced portfolios have historically returned about 5% on average, compared to the S&P 500’s 10.44% return since 1990.

The problem most of us have with investing strictly in something like the S&P 500 is that we need that money at some point. When we see our money drop by 29.65%, like we did in 2022, we have trouble staying invested or need to pull some of the funds, locking in our losses. This is why the wealthiest focus on downside protection.

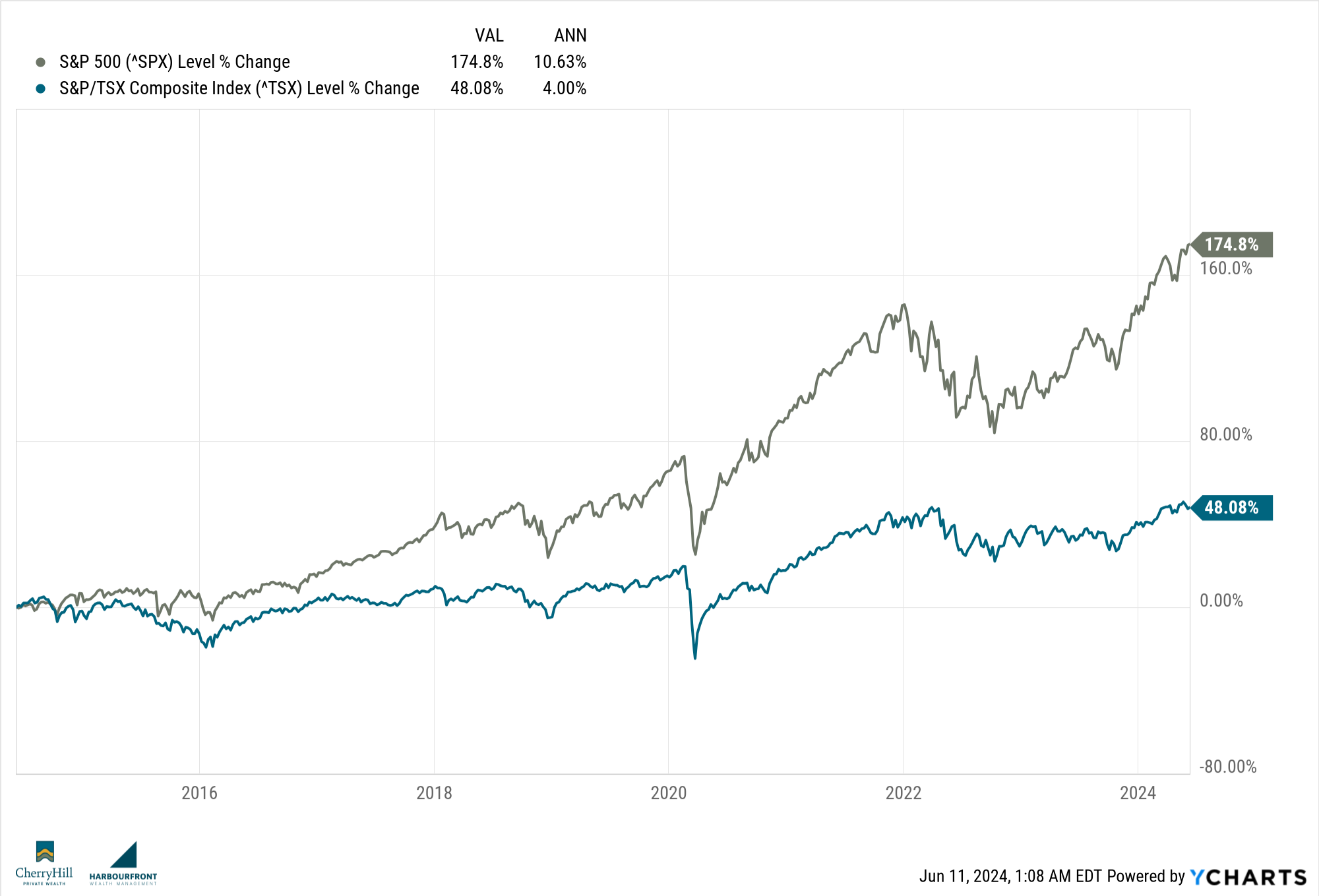

There are many strategies that can give above-average returns while protecting a portfolio from negative returns. Diversification is one that you will hear about a lot - “don’t put all your eggs in one basket”. This could be as simple as not investing everything into Nvidia, no matter how tempting it might be. This is a pretty basic starting point but one that we get wrong so often. In Canada, we tend to put more of our money into Canadian equities, but by doing so, we are giving up about 3% per year if we go back to 2000, and that number skyrockets to over 6.5% from 2014 to today.

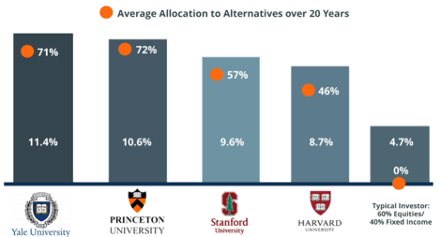

Many of the pension funds and super-rich diversify into other asset classes so that they’re not losing out on returns, but also keeping the investments positive in the worst years. These investors use products like hedges, shorts, and structured notes. They have also been increasingly relying on the stability and above-market returns of assets like private equity, private credit, and real estate.

With cracks starting to show in the financial markets, it’s a great time to revisit your portfolio and determine whether your advisor has taken downside protection into account. If they don’t know what this means or just talk about your fixed income holdings and “diversified portfolio,” then maybe it’s time to look for a second opinion.

Until next week, Happy Investing!

Trevor

In Lighter News:

On June 10, 1652, John Hull created the first mint in America, which was a bold step away from English colonial law. They produced, what was called the Pine Tree Shilling and was a crucial step in the economic development of the American colonies, laying the groundwork for future financial autonomy.

In The Markets:

Stock markets continued to be pushed by performance from Nvidia, which jumped more than 10% in the week. The Nasdaq Composite saw a weekly gain of nearly 2.4%, while the S&P 500 hit new all time highs.

In Canada we saw the BoC lower interest rates for the first time since March 2022 when they began tightening their monetary policy. South of the border, however, better-than-expected job numbers could influence the Feds decesion to hold rates for the time being.

Major banks in the US are set to release earnings this week, and key economic reports, including the Consumer Price Index (CPI) and Producer Price Index (PPI) will be closely watched by investors.