RRSPs aren’t bad, but…

Hi, !

Recently, there have been intriguing articles in the Globe and Mail highlighting individuals who have amassed remarkable balances in their Tax-Free Savings Accounts (TFSAs). For instance, one retired military member has built an impressive $883,500 TFSA. Considering the maximum total original contribution room for one person is $95,000 in 2024, this achievement is undeniably noteworthy.

While these articles caution about the risks associated with generating such substantial returns and acknowledge the role of luck, I’d like to delve into how we can strategically position risk across entire portfolios and various account types.

When making investments, we often focus on potential or likely returns rather than the associated risks. However, portfolio management theory often frames investments as purchases of risk. You can choose to purchase more or less risk, expecting higher returns for higher levels of risk. Thus, risk isn’t inherently negative; it’s an attribute that should be managed within one’s comfort zone over time.

In Canada, we have a range of account types for investing, each with different rules, tax implications, limits, and purposes. Despite these differences, many investors utilize the same portfolio across all their accounts.

Being intentional about how you spread your portfolio across different accounts can yield several benefits.

1. RRSPs: A Compounding Deferred Tax Liability

In my view, an RRSP represents a compounding, deferred tax liability:

- Compounding: Whether positive or negative, the results are exponential.

- Deferred: While deferring taxes can be advantageous, it merely postpones the issue.

- Tax Liability: Withdrawals from an RRSP are taxed as income without preferential treatment for capital gains or dividends.

Given these characteristics, it’s prudent to allocate lower-risk fixed-income assets to RRSPs to slow the compounding process. Since all redemptions from RRSPs are treated as income, it makes sense to hold income-producing assets here.

2. TFSAs: Tax-Free Growth and Withdrawals

In contrast, all returns in a TFSA are tax-free, as are withdrawals. However, it’s crucial to note that losses in a TFSA cannot be deducted, and contribution room cannot be regained.

For “reliably aggressive” investments—diversified assets with high equity content—TFSAs are ideal. Since there are no tax implications, aggressive investments with high compounding potential suit this account, but be aware of the accompanying volatility.

3. Non-Registered Accounts: Tax Efficiency and Speculative Ventures

Non-registered accounts entail various tax implications:

- Income Tax: All income is fully taxed, but dividends receive preferential treatment, and capital gains can be triggered, or deferred indefinitely.

- Capital Gains/Losses: Capital losses can be offset against capital gains.

For speculative ventures or dividend-paying investments, a non-registered account is preferable. Speculative investments, particularly those involving individual stocks or bets (gambles) using options, benefit from the ability to offset capital losses against gains. Dividend-paying investments are also tax-preferred in non-registered accounts, and compounding isn’t an issue if dividends are spent rather than reinvested.

Balancing Act: Seeking Professional Guidance

Efficiently allocating investments across accounts depends on various factors, including account balances and risk tolerance. Consulting with a financial advisor is crucial to managing both risk and long-term tax consequences effectively.

In conclusion, thoughtful allocation of investments across different account types can optimize returns while managing risk and tax implications. If you’d like to explore this topic further, don’t hesitate to reach out.

Until next week, Happy Investing!

Adrian

In The Markets:

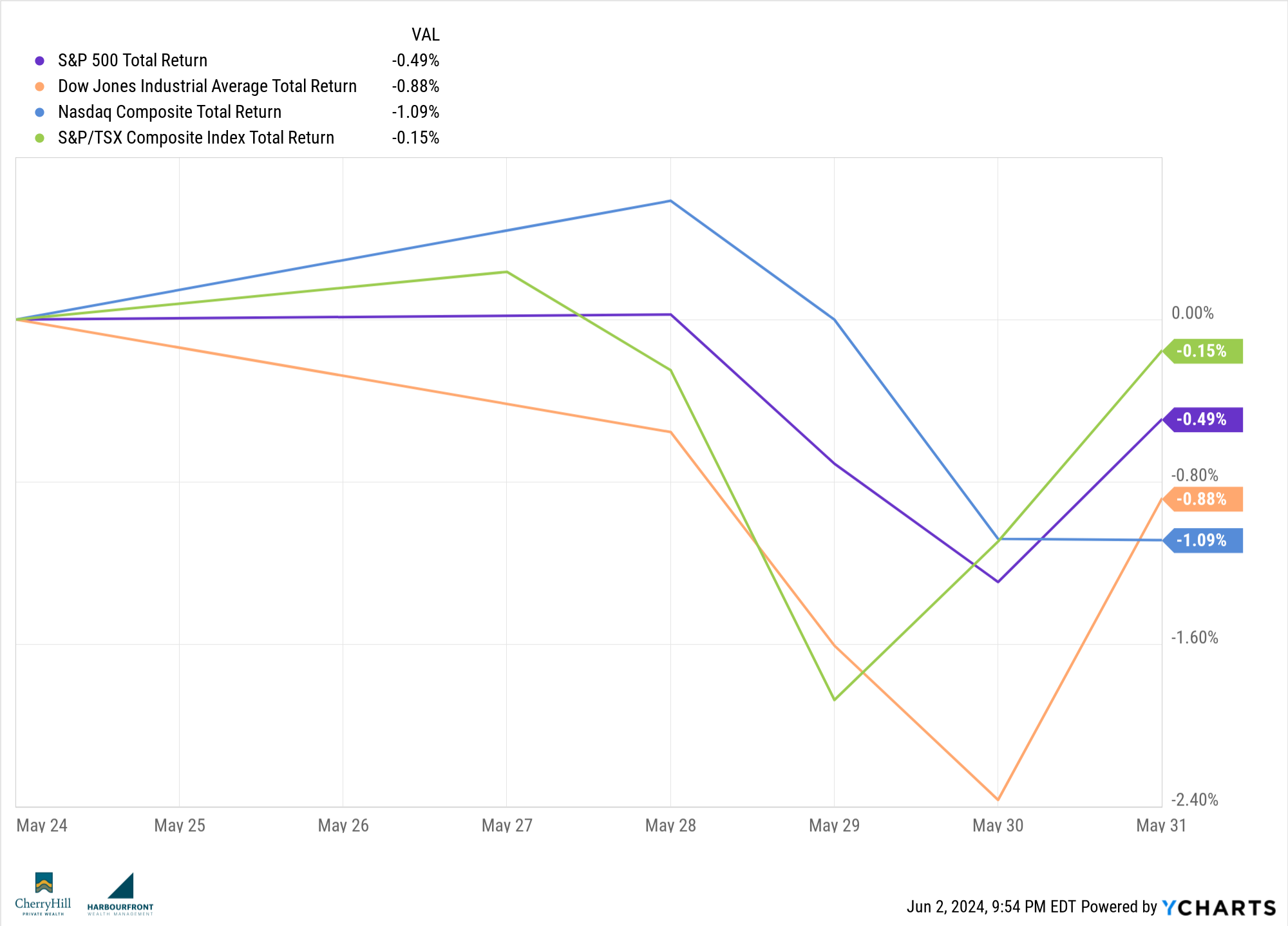

Last week, major investment markets experienced some significant movements. U.S. stocks ended their multi-week rally, highlighted by a sharp drop on Thursday, the worst single-day decline since March 2023. This was primarily due to investor concerns that stronger-than-expected economic data might lead to prolonged high-interest rates. The Dow Jones Industrial Average fell by nearly 600 points, while the S&P 500 and NASDAQ also saw declines.

In specific sectors, technology stocks like Nvidia reported strong earnings and announced a 10-for-1 stock split, providing some positive news amidst the overall market downturn. However, technology stocks, despite their impressive earnings growth, have recently been outperformed by utilities, reflecting a broader base of market gains beyond just the tech sector.

Bond yields saw modest increases, and oil prices continued their decline from earlier highs. WTI crude oil prices, for example, dropped to around $78 per barrel from peaks above $87 per barrel in early April.