How Severe is the Mortgage Crisis?

Hi, !

I hope you enjoyed Mother’s Day weekend, spending quality time with loved ones and celebrating the amazing women in our lives who often don’t get thanked enough.

Each week, one topic continues to dominate household financial discussions: interest rates. Even without a Federal Reserve or Bank of Canada meeting, interest rates are consistently making headlines. Recently, there has been a surge of articles discussing the looming issues surrounding mortgage renewals.

With cash flow already tight for many Canadians, the question arises: what happens when mortgage costs increase too?

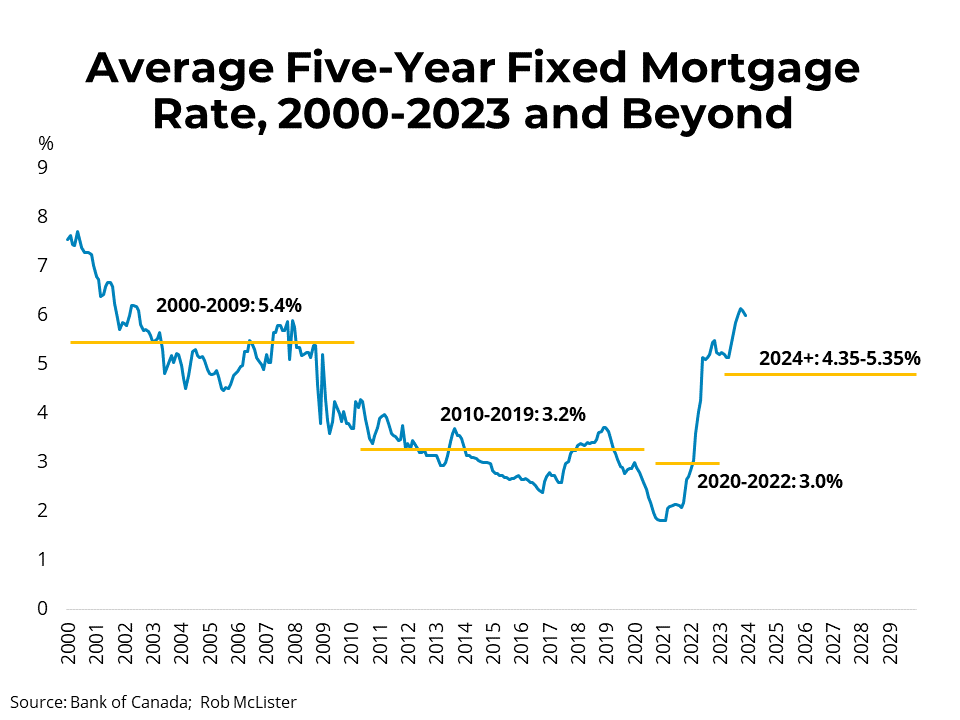

It feels like we’ve seen this coming for a while, yet many of us believed that interest rates would quickly return to their pre-2022 lows. Traditionally, Canadians opt for a 5-year mortgage, with more than half choosing the safer fixed-rate option. In 2022, there were 3 million mortgages in Canada, and 77% of those were fixed-rate. This has provided some cushion during the current rising interest rate environment, but that safety net is about to be cut loose. Borrowers with variable-rate mortgages have seen their payments rise nearly 70% since the start of the hikes.

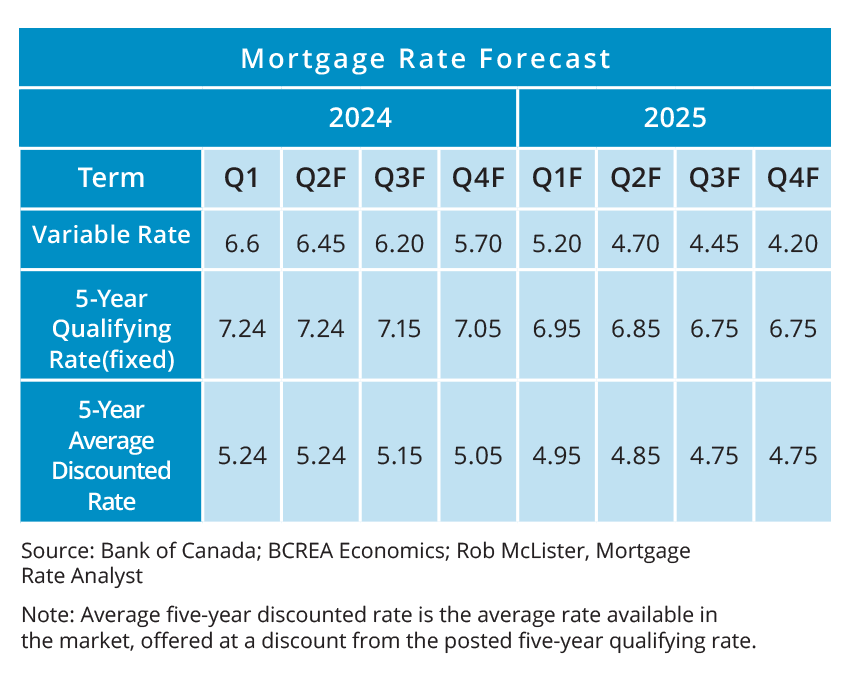

So why is this such an important topic today? Canadians currently have about $2 trillion in outstanding mortgage debt, and the CMHC predicts that 45% of all mortgages will come up for renewal over the next two years. During the pandemic years of 2020 and 2021, many people refinanced or had their mortgages renew organically, with rates around 1.39%. Today, those rates are closer to 4.79%.

Refinancing variable mortgages that had fixed payments will also present challenges, as many of these loans saw amortizations increase from 15-20 years to 50-60 years. To get back down to the allowed 30-year amortization, borrowers will need to make a lump sum payment, increase their monthly payments, or both.

Just as you wouldn’t wait until your retirement party to see if a few thousand dollars in a savings account will suffice, you shouldn’t wait until your mortgage renewal to start planning. There are several options available with enough time, including using investments from TFSAs or non-registered accounts, but there might still be better choices. We work closely with a mortgage broker who has many options at her disposal, and we are also happy to collaborate with your current lender to help you achieve your goals.

To put this into perspective, a pandemic-era mortgage of $500,000 would have mortgage payments around $1,973 based on a 25-year amortization. At today’s rate of 4.79%, that same payment would be about $2,849.

Many of our clients are now mortgage-free, so this might not directly affect you. However, if you know someone who might benefit from this information, please forward this newsletter to them or have them reach out. We’d love to have a conversation to help them avoid an uncomfortable situation over the next couple of years. Interest rates are likely to stay higher for longer, and even if there are a few rate reductions before their term comes up, they are still likely to face an interest rate shock.

Until next week, Happy Investing!

Trevor

In Lighter News:

Mother’s Day dates back to the early 20th century in the United States, founded by Anna Jarvis in 1908. It has become a widely celebrated day, with over 150 million Mother’s Day cards exchanged annually in the U.S. It’s also one of the busiest days for phone calls, with traffic increasing by up to 37%.