What the Budget Means for You

Happy Earth Day, !

“No one is very happy. Which means it’s a good compromise.”** - Tyrion Lannister.**

While this sentiment wasn’t originally coined by the Game of Thrones character, it aptly reflects the feelings surrounding last week’s federal budget release. As this isn’t a political newsletter, I will strive to remain impartial and provide you with the necessary information to make informed financial decisions. While researching this article I referenced several publications that typcially have opposing political leanings as well as contacting several of my resourses for insight. You can find links to a couple of the articles that I feel sum up the budget best at the end of the newsletter.

New Capital Gains Tax

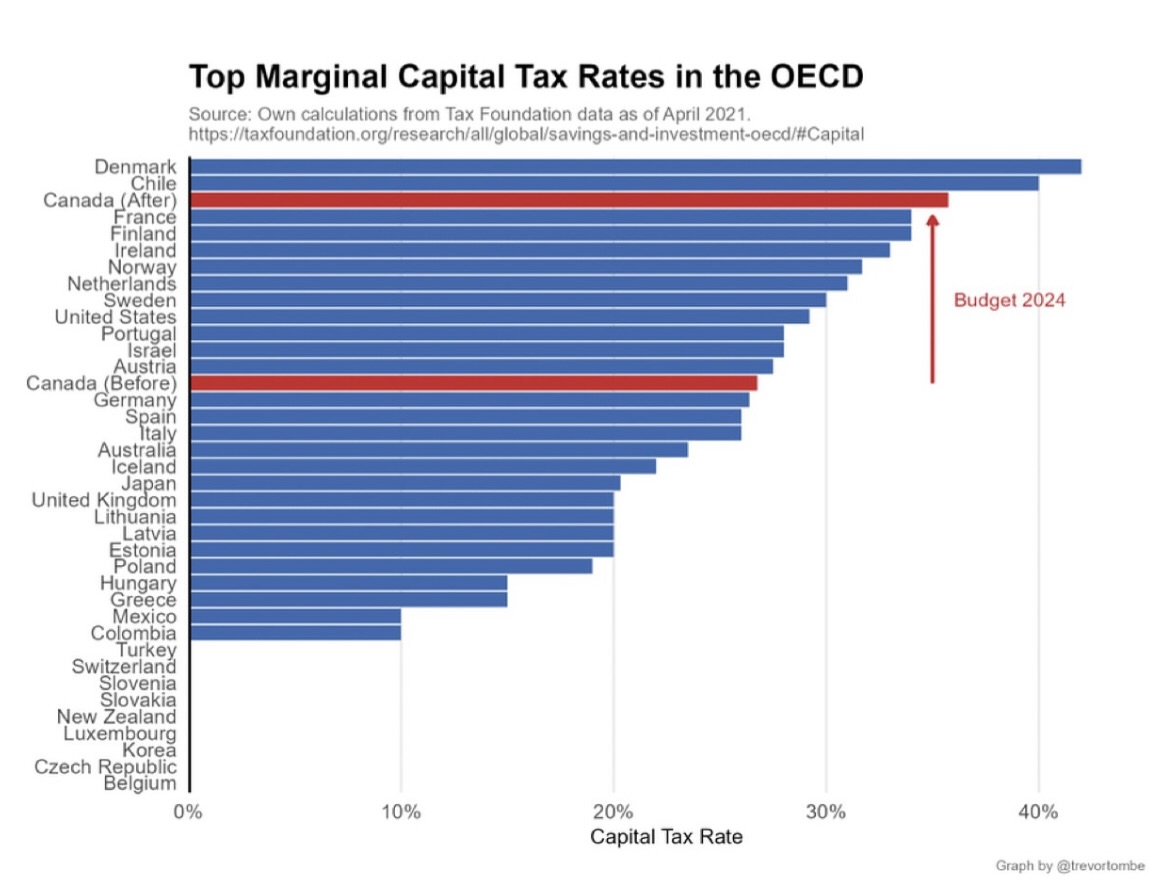

Most of the discussion seems to center around the increased capital gains tax, so let’s start there. Historically, capital gains have been taxed at a 50% inclusion rate as a measure to encourage innovation and growth as well as a reward for the additional risk associated with this type of investment.

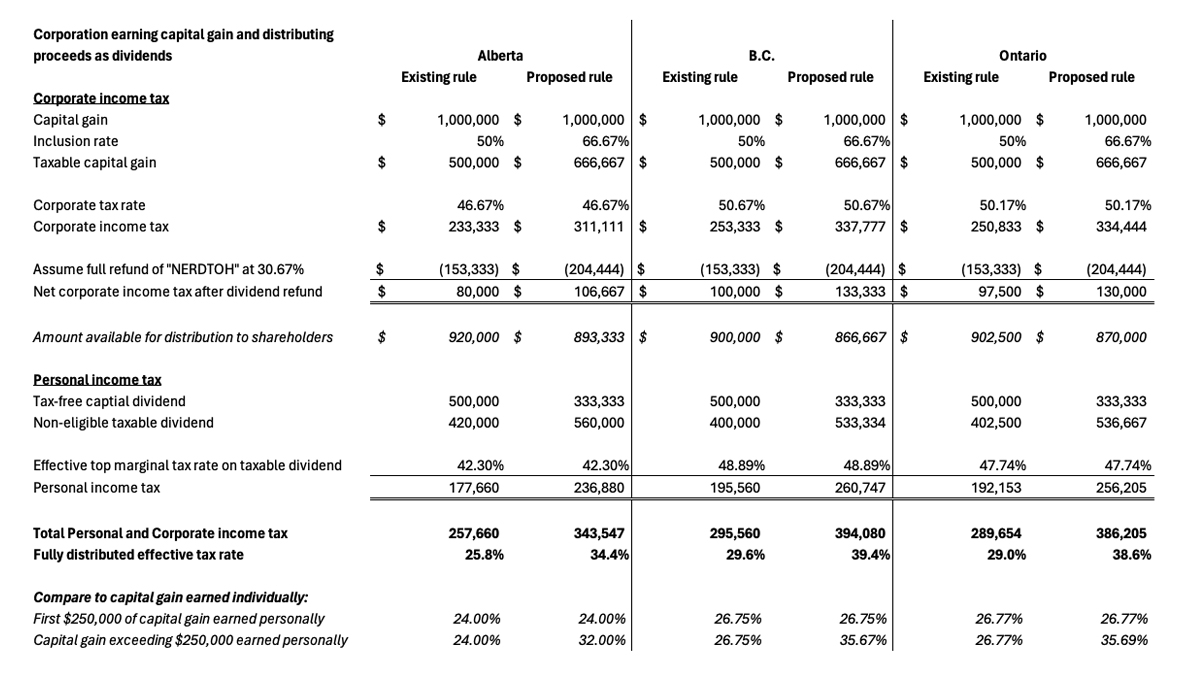

The new budget proposes increasing this inclusion to two-thirds for any capital gain over $250,000. This targets what the government describes as making “the rich pay their fair share.”

A story that caught my attention this week involved a retiree with a rental investment property, who planned on using the sale to fund their retirement. The additional taxes could tighten their retirement budget more than expected. The budget also introduces complexities for families and estate planning with regards to cottages, especially if they are looking to keep it in the family.

A seemingly overlooked consequence is the impact on our doctors. Many doctors save for retirement through their incorporated businesses, since they don’t have pensions. The increased taxes will affect corporations from the first dollar, which could drive many, especially general practitioners who are already in short supply, to relocate their practices outside Canada.

The projected $20 billion revenue from this tax increase underpins much of the proposed budget spending. However, if history is any indicator, these taxes will likely yield much less than forecasted. Several accountants working with high-net-worth individuals and businesses have mentioned exploring ways to circumvent this tax, including relocating corporations to tax-friendlier jurisdictions or simply not selling assets.

The Rest of It

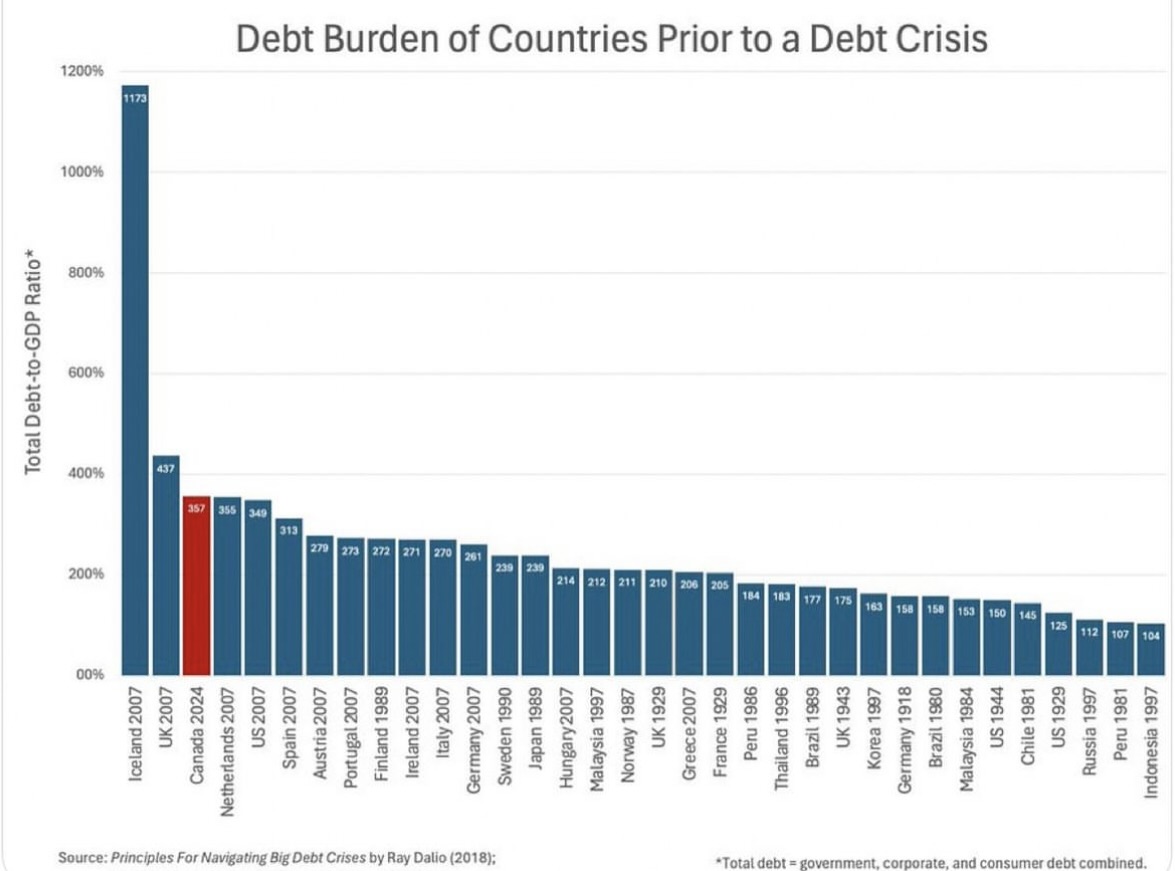

As federal spending increases by over $50 billion and debt servicing becomes a larger expense than health care, there must be some people that are excited by this?

It doesn’t seem so.

The budget primarily addresses the housing crisis, and with an anticipated 500,000 new immigrants annually for the next two years, it is definitely becoming a crisis. Despite the urgent need for housing solutions, other pressing issues like rising rental and mortgage costs and food affordability were largely overlooked.

There’s also a risk of aggravating inflation by injecting new spending. As former Bank of Canada Governor David Dodge noted, “Canada needs increased productivity and lower inflation, which generally come from reducing spending, regulation, and taxes.”

Without spending too much time on the federal debt, the government promises a budget for young Canadians, but this debt issue is becoming their problem. With increased taxes that don’t cover the additional spending, the high interest rates are creating a massive expense, which isn’t getting better. To hit their debt targets, which Canadian’s rely on to keep the AAA credit rating (if lost this would cost the government more to service debt, which would be passed on to banks, and then to us, the consumers) they need to keep it at a certain GDP-to-debt ratio. We are extremely close to this. If the increased tax falls short or their aggressive interest rate reduction projections miss, we could be offside of the ratio.

The Things I Liked

Unfortunately, this list isn’t long. While the budget allocates funds to several social issues, the early crisism is that the allocation will do little to move the needle.

**RESPs: **Programs like RESPs and RDSPs, which are underutilized yet offer “free” money to beneficiaries, are set for improvement. The new budget mandates automatically opening an RESP for children by age four, with outstanding bonds added to their account if one has not been established.

**Financial Literacy: **Many Canadians lack access to reliable financial advice, often encountering predatory practices. The budget strengthens Prosper Canada, a national financial literacy charity, ensuring more Canadians can access free advice and financial programs.

Final Thoughts

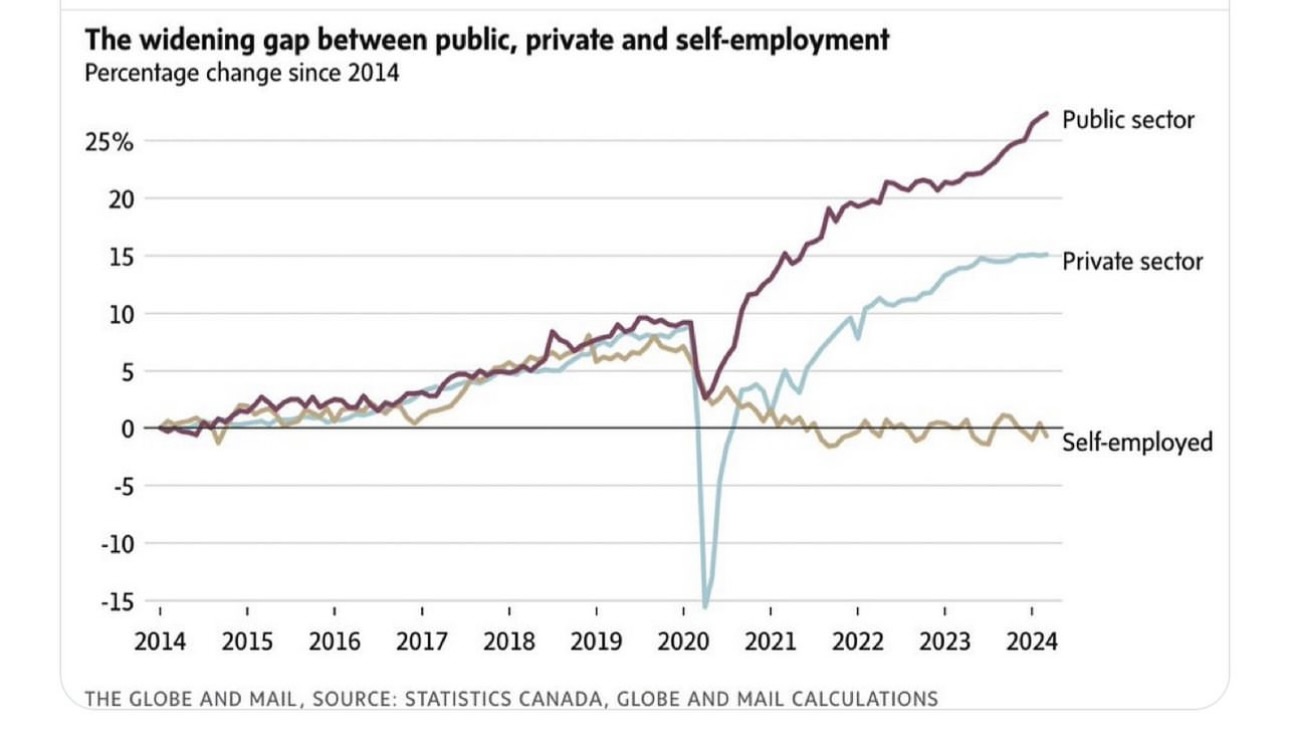

We seem overly fixated on enabling our youth to purchase homes, often to the detriment of other issues. Reducing red tape to foster growth could benefit young Canadians, but it’s moot if they’re leaving Canada for better opportunities. Policies that hinder economic growth and neglect infrastructure development that could create meaningful employment are missing the mark. Coupled with a 2.5% decline in GDP over recent years—excluding population growth—and a reduction in entrepreneurial and public employment opportunities, it’s clear we need to rethink our approach.

Until next week, Happy Investing!

Trevor

Further Reading:

Unaffordability Budget (Financial Post)

Worst Canadian Budget Since 1982 (National Post)

Here’s What a Fairness for Every Generation… (The Globe & Mail)