TFSA vs. RRSP: The Epic Showdown

Hi, !

Happy Family Day to you and your family!

Family Day has been around since 1990 in Alberta, but it took until 2008 for Ontario to adopt the holiday and get us a long weekend between New Year’s and Good Friday. I hope that you are able to spend time with family today and I’d love to hear how you’re spending the holiday Monday!

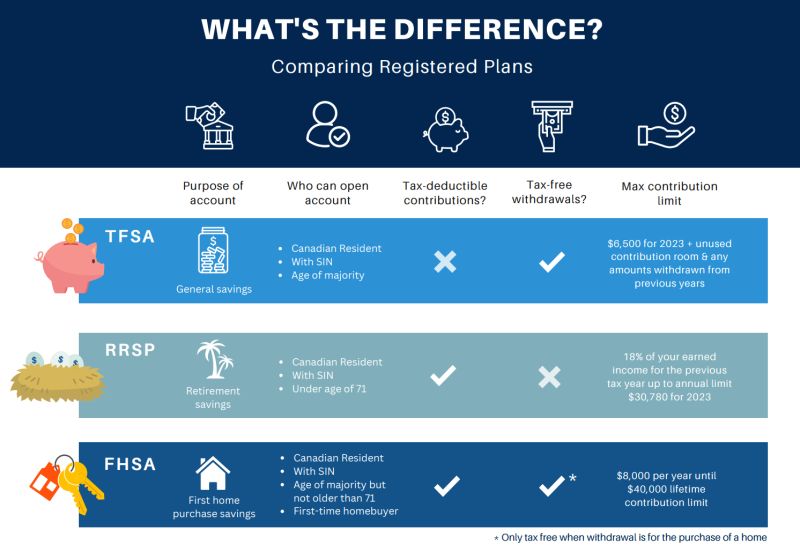

Many Canadians find themselves unable to fully contribute to both the Registered Retirement Savings Plan (RRSP) and the Tax-Free Savings Account (TFSA). As a result, the question of how to best allocate long-term savings is crucial. Unsurprisingly, this is one of the most common questions I hear from my clients who are still in the wealth accumulation phase. If you’ve already built your wealth, feel free to pass this on to someone you care about who is still on the journey towards financial freedom.

The TFSA has grown in popularity in recent years, attracting more investments than its RRSP counterpart, even though this year’s limit is $7,000 for the TFSA and as much as $31,560 for the RRSP.

So, why is this the case?

Several factors contribute to this trend, including the “no strings attached” nature of the TFSA and many misconceptions about the RRSP and the taxes that will eventually be paid. Determining whether to invest in a TFSA or RRSP involves many factors, more than this newsletter can cover. However, I will break down a few misconceptions and hopefully provide an idea or two that could be useful.

Investing in a TFSA doesn’t necessarily mean you’ll pay less tax than with an RRSP, as you’re contributing with after-tax dollars initially. Many critics of RRSPs argue that many Canadians will be at a higher or similar marginal tax rate (MTR) in retirement as they were when they contributed. The goal of investing and working with a wealth management firm is definitely not to have less spending power in retirement. So, are the critics right?

Often missed in the conversation is how we spend the tax refund. If we change our mindset about the refund we get from investing in an RRSP, we can turbo charge our investment strategy. As amazing as it is to get that refund and go on a family vacation, it’s unlikely that it’s the most efficient way to reach your retirement goals - even if sometimes it’s more important at the time. If we look at the refund as an investment loan, this could be the boost to have the RRSP the long-term winner. The refund can be invested back inside the RRSP, creating another refund next year, but it can also help fund an RESP, or TFSA. It can also pay down high interest debt, freeing up cash flow.

Even with a similar MTR in retirement, the tax shelter of the RRSP can aid in long-term growth. Understanding what you paid in taxes last year and what this year looks like can help make a more informed decision. TFSAs are usually more beneficial for young people, as they contribute with lightly taxed money, which wouldn’t yield a large refund in an RRSP anyway. TFSAs are also more flexible with withdrawals and can double as an emergency fund, but this flexibility can be a double-edged sword.

There are several factors to consider when determining the best investment vehicle for the long term, and we’re happy to discuss how you can best utilize your resources.

Until next week, Happy Investing!

Trevor

PS: There are more than 1 million Ontarians with expired plates. If you’ve forgotten to renew since it became free, you could still face a $1,000 fine. Visit ontario.ca/page/renew-your-licence-plate to update your plate and avoid a potential fine!