Don’t Miss Out on a 70% Boost in Your Investments

Hi, ! Let’s make the most of this cold weather and make you some money!

I must be getting old because I keep finding myself talking about the weather and how fast time is passing. Just like many of you, it felt like the calendar turned a page just yesterday, and yet here we are, approaching the end of January!

As January zooms by, there’s an important deadline quickly approaching - the RSP deadline. If you’re still contributing to RSPs, mark your calendars for February 29th this year (yes, it’s a leap year!). Despite the various retirement savings options available, the RSP remains a vital tool. For those of us feeling the pinch in our wallets and unable to make additional contributions to boost our retirement savings, there are still options worth exploring. I’m a fan of strategies that don’t impact my day-to-day finances but can significantly influence my retirement goals.

Let’s dive into the RSP Gross-Up strategy, a tactic that could potentially add several thousand dollars to your savings each year. But before we get into the nitty-gritty, let’s quickly recap what an RSP is all about. When you save within an RSP, the government essentially “loans” you the tax you paid on your contribution. We often refer to it as a refund, but remember, you’ll eventually need to repay it. Wealthy individuals are skilled at leveraging other people’s money to grow their wealth, and you can do the same. For instance, if you’re in a hypothetical 40% marginal tax bracket (yes, I’m rounding for simplicity), contributing $10,000 to your RSP means the government “loans” you $4,000. Most “regular” folks tend to spend their “refund” on something immediate.

Now, the RSP Gross-Up strategy is fantastic because it lets you use this “loan” to accelerate your investment goals without affecting your day-to-day cash flow. Here at Harbourfront, we have access to lending options that enable you to take out an RSP Loan and delay repayments for several months, usually until after you’ve received your refund. If you just use the loan to invest the extra $4,000 that you know you’ll be getting back, you will still have a refund. We want to fully utilize the RRSP “*Loan” *(refund).

Here’s the kicker: by taking this route, you can actually invest an additional $6,667, and your refund will cover your extra contribution. This represents a whopping 67% increase over the initial $10,000 contribution and the same increase over simply adding the $4,000. Imagine the positive impact this could have on your wealth if you repeat this process annually!

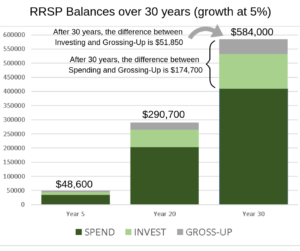

The below scenario is based on a 29.65% MTR and contributions of $6,000 per year.

The wealthy are constantly seeking strategies to make their money work for them, and this is a straightforward method that can potentially boost your investments by almost 70% each year! I’d love to hop on a quick call with you or someone you know who is open to leveraging other people’s money to enhance their wealth. I hate to sound like a clichéd infomercial, but “act now because time is running out”! We will need a couple of weeks before the RSP Deadline (February 29) to set up this strategy, so time is of the essence.

Until next week, Happy Investing!

Trevor